Our nine predictions for 2016 were designed to be measurable. The outcome wasn’t bad. Consequently, inspired by Apple’s self-proclaimed ‘courage’ to remove the headphone jack on the then-new iPhone 7, we upped our game when publishing our eight (courageous) predictions for 2017.

We didn’t think it would play out as well as it did. We predicted that Verizon would dump bucket plans and go all-in on unlimited. It happened. Verizon doesn’t call its unlimited plan “Kick the bucket”, but still. We predicted that the “control & zero-rate content” bundle would fail in the light of unlimited and the clouds have never been darker for AT&T with regards to its thirteen-months-have-elapsed-but-yet-to-be-approved attempt to take control over Time Warner. We also predicted that BT and Deutsche Telekom would eat crow and admit that their copper-embracing access strategy wasn’t future-proof just to realise that they now need to speed up to meet the demand for FTTH – or be run over by competition.

We weren’t right on everything – Vodafone didn’t pause 5G plans to focus on unlicensed spectrum; the company just asked the industry to sober up – but we are nevertheless so encouraged that we for 2018 present seven undaunted predictions:

- We’re all Netflix!

- Zero-rated offers are pulled back – due to video, not regulation

- Unlicensed to the rescue – when cost per GB is about to rise

- Copper squeezed out by the fibre/wireless ecosystem

- No humans – just robots – in the NOC

- The unlimited plan extends beyond the humans in the home

- Churn is dead

Prediction 1: We’re all Netflix!

Every telco will start original content production in 2018

Not discouraged by Netflix’s cash burn, telecom operators are in 2018 betting on that one card will trump all other loyalty cards in the deck – original content.

Not discouraged by Netflix’s cash burn, telecom operators are in 2018 betting on that one card will trump all other loyalty cards in the deck – original content.

If not already launched or in progress, every modern telco will have started production of original drama series in 2018. The hopes are high: End-users love video, it consumes data and customers who can consume the data they want without annoyances are more satisfied and loyal than those that were given the impression that mobile data is as expensive as saffron and should be consumed with caution.

Has our industry finally found the grain of gold? Possibly. The business models are many and the ultimate question is yet to be answered: Does it pay off? Just like Netflix, there might not be time to wait for someone else to figure it out for you. Burn the cash and hope for the best. But before starting to subsidise the video consumption of your customers you’d better stop subsidising their devices – because this will grow and so will your costs.

Has our industry finally found the grain of gold? Possibly. The business models are many and the ultimate question is yet to be answered: Does it pay off? Just like Netflix, there might not be time to wait for someone else to figure it out for you. Burn the cash and hope for the best. But before starting to subsidise the video consumption of your customers you’d better stop subsidising their devices – because this will grow and so will your costs.

![]() Wild card: AT&T isn’t discouraged by the U.S. government’s blocking of the acquisition of Time Warner and is in the second half of 2018 instead making an attempt to acquire Netflix to be able to fulfill its vision of video-broadband convergence.

Wild card: AT&T isn’t discouraged by the U.S. government’s blocking of the acquisition of Time Warner and is in the second half of 2018 instead making an attempt to acquire Netflix to be able to fulfill its vision of video-broadband convergence.

Prediction 2: Zero-rated offers are pulled back – due to video, not regulation

The commercial risk of ‘zero-rating an unknown’ makes operators favour the safety of neutral plans

Since zero-rating offers currently spread like wildfire across the European continent – driven by Deutsche Telekom‘s and Vodafone‘s more-for-more upsell ambitions – this is indeed an undaunted prediction.

But here’s the problem: The services that operators are kind enough to exempt from the gigabyte meter are from global internet service giants like Facebook, Google, Twitter, Netflix and Amazon. And – as the links show – it’s in their plans to massively expand in video.

These internet giants couldn’t be happier when operators subsidise mobile users’ consumption of their services. But mobile operators that thought that zero-rating Twitter meant covering the cost for a few tweets a day or zero-rating Facebook meant covering the cost for a few posts a day will wake up. Their propositions will instead zero-rate hours of video – where a significant part is advertising. Advertising that telcos subsidise.

The clarification that zero-rating can’t just be national but need to be EU-wide is another negative surprise for zero-raters.

![]() Facing the spiraling cost of this, mobile operators will not try to communicate incomprehensible limitations in their zero-rating offers like “YouTube is included, but not the ads”. They will instead find their way back to a neutral gigabyte-based and/or premium unlimited offer. Rather paid unlimited than ‘zero-rating an unknown’.

Facing the spiraling cost of this, mobile operators will not try to communicate incomprehensible limitations in their zero-rating offers like “YouTube is included, but not the ads”. They will instead find their way back to a neutral gigabyte-based and/or premium unlimited offer. Rather paid unlimited than ‘zero-rating an unknown’.

Wild card: Amazon acquires Sprint and provides free unlimited mobile services for customers who never leave amazon.com while shopping. To support it, Amazon trials Softbank-manufactured Sprint-connected shopping robots (see Prediction 6) that move around your home in search for anything that can be ordered and open the door for deliveries or services.

Wild card: Amazon acquires Sprint and provides free unlimited mobile services for customers who never leave amazon.com while shopping. To support it, Amazon trials Softbank-manufactured Sprint-connected shopping robots (see Prediction 6) that move around your home in search for anything that can be ordered and open the door for deliveries or services.

Prediction 3: Unlicensed to the rescue – when cost per GB is about to rise

4G slows, 5G isn’t here yet – but the ‘Toyota Corolla of connectivity’ comes to the rescue as data demand grows

Thanks to the excellent characteristics of 4G, it’s so far been cheap to produce another gigabyte of data – something which hasn’t been reflected in the pricing structure of many mobile operators: They instead penalised customers who wanted to use more data by charging more for an additional gigabyte than the average price of those gigabytes already consumed. It led to one thing: Data anxiety.

Luckily, as predicted last year, plans with unlimited data volumes have come to the rescue. It has been good for base growth, for loyalty and good for the financials. And customers are happier.

Luckily, as predicted last year, plans with unlimited data volumes have come to the rescue. It has been good for base growth, for loyalty and good for the financials. And customers are happier.

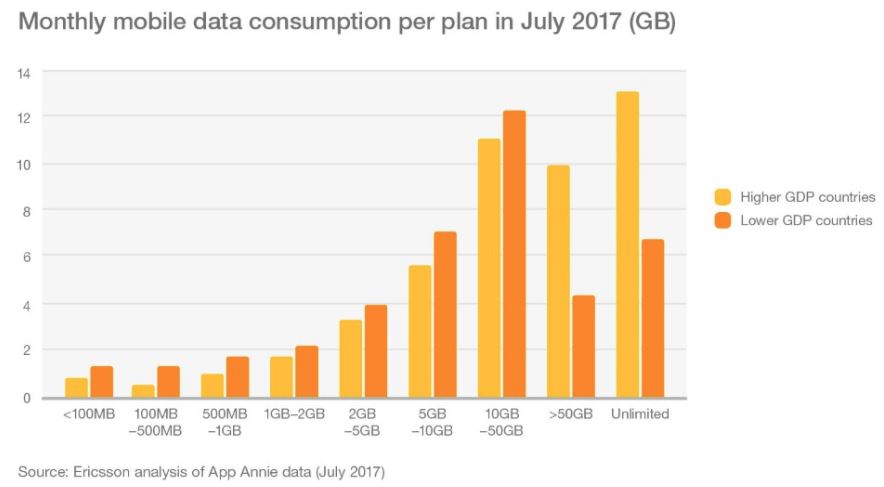

But it also drives data traffic. Not as much as you might think – see the stats from Ericsson‘s latest Mobility Report in the graph below: In higher GDP countries, unlimited customers are only using a few GBs more than customers on 10-50 GB plans (and in lower GDP countries even less than customers on 10-50 GB plans).

But the usage growth will continue, driven particularly by all that video (see Prediction 1 and 2). This starts to strain the 4G networks – average speed is no longer increasing in the top-performing countries. Since unlimited plans aren’t bringing any additional revenue for that extra gigabyte consumed, the cost per gigabyte becomes an issue (again) as the cost to expand capacity in a fully loaded 4G network is something quite different than the cost to handle an additional gigabyte in an half-empty network.

5G is coming, but not fast enough. The 5G network might be there fairly soon, but as usual the issue will be about the penetration of capable terminals. For operators with a high share of fixed-substituting home routers such as the Finnish or the Austrian operators, this is a smaller issue as it’s ‘just’ about replacing these routers and make sure they are within the 5G coverage area. These routers stand for about 20% of the total subscription base but carry 50-60% of the data traffic. But for most operators, 5G will not offer much load relief until the 5G smartphone penetration is substantial.

The mid-term rescue comes from unlicensed spectrum. The newest smartphones support what is called LAA – Licensed Assisted Access. It adds unlicensed spectrum LTE in the 5 GHz band to the regular, licensed, LTE and aggregates the two so that high (like 1.1 Gbit/s) data rates can be achieved in a situation where licensed spectrum is heavily utilised.

But unlicensed doesn’t need to be complicated. There is a technology which is being supported in 100% of the smartphones: The ‘Toyota Corolla of connectivity’ – Wi-Fi. With unlimited mobile data, the offload relay baton moves from the end-user to the operator. And operators will step up to the challenge because it makes sense from a cost point of view. If you want the full Corolla story, watch this video.

But unlicensed doesn’t need to be complicated. There is a technology which is being supported in 100% of the smartphones: The ‘Toyota Corolla of connectivity’ – Wi-Fi. With unlimited mobile data, the offload relay baton moves from the end-user to the operator. And operators will step up to the challenge because it makes sense from a cost point of view. If you want the full Corolla story, watch this video.

Wild card: By combining automatic Wi-Fi offload with large-scale Wi-Fi networks, cable operators show that they can produce a gigabyte of smartphone data averagely as cheap as cellular-only MNOs even though cablecos still buy many of the gigabytes from their host MNOs.

Prediction 4: Copper squeezed out by the fibre/wireless ecosystem

FTTH grows the total market and paves way for wireless

Last year we predicted that even BT and DT would have to realise that the copper era in the access network is over. Operators like DT, A1, KPN and Swisscom will still try to delay the shift to fibre by pushing hybrid 4G/DSL. Adding DSL to 4G is like adding a coal cart to an electrical locomotive hoping for a hyperloop.

Last year we predicted that even BT and DT would have to realise that the copper era in the access network is over. Operators like DT, A1, KPN and Swisscom will still try to delay the shift to fibre by pushing hybrid 4G/DSL. Adding DSL to 4G is like adding a coal cart to an electrical locomotive hoping for a hyperloop.

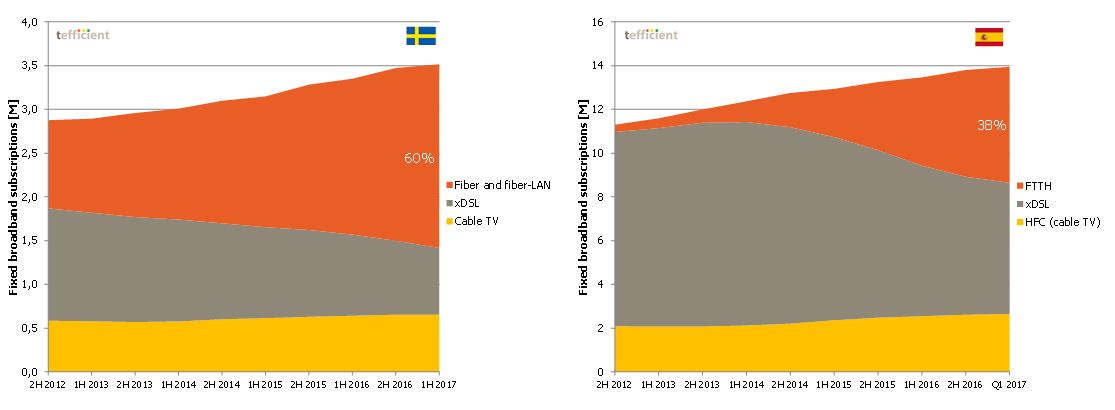

Already during the transition from 2G/3G to 4G, mobile operators realised that they by default need fibre to the base station for capacity reasons. Without a widespread fibre infrastructure in place, the cost to get fibre to the base station sites is high. In countries such as Spain, Sweden, Portugal, Norway, Latvia and Lithuania where fibre (FTTH and FTTB) has become a de facto solution for fixed broadband to the homes, the likelihood of finding a fibre connection point (or canalisation) nearby is much higher for mobile operators.

Vice versa, mobile network’s need for fibre will take fibre to locations that otherwise perhaps would not have been built. There will be ripple effects: Options for better connectivity will be opened for nearby businesses and homes. In e.g. Sweden and Spain, fibre technologies (orange) drive good growth into the total fixed broadband market:

In the homes, a majority of the traffic is already over Wi-Fi and its share will continue to grow. The Wi-Fi mesh market will flourish – fuelled by operators (such as Ziggo below) that have realised that it’s not enough to get the speed and capacity into the house; it needs to be distributed in the house as well.

5G-based fixed wireless services will surface as a cost-effective alternative to FTTH in less densely populated areas but will also require a well distributed fibre infrastructure.

Simply put: The data traffic growth has created a wireless/fibre ecosystem where there’s no room for copper. Wireless needs fibre and fibre needs wireless.

![]() Wild card: After being publicly shamed by a Swedish minister visiting Germany in November 2017, the new German government had it and decides to distance itself from Telekom. It sells its shares in DT for 20 BEUR and uses it to create a fund for German municipalities so that they can build open FTTH networks connecting their inhabitants and businesses.

Wild card: After being publicly shamed by a Swedish minister visiting Germany in November 2017, the new German government had it and decides to distance itself from Telekom. It sells its shares in DT for 20 BEUR and uses it to create a fund for German municipalities so that they can build open FTTH networks connecting their inhabitants and businesses.

Prediction 5: No humans – just robots – in the NOC

With AI, network uptime has never been higher than in 2018

Several progressive operators are in 2018 putting software at work in the former network operations centers. The ‘robots’ will monitor all aspects of the network, solve routine issues and only alert operations staff when hands-on action need to be taken in the field. 24/7 manning is no longer needed and the high capacity of the ‘robots’ allow immediate error detection, quick analysis and fast action taking. The business case is driven by higher network uptime and higher network quality, not cost savings.

![]() Wild card: After having tried call center outsourcing, insourcing, offshoring and onshoring, the British MNO EE decides to give robosourcing a go. In the end of 2018, 15% of EE’s incoming call volume is handled by conversational robots. It surprises the operator that in the IVR self-serve tree, the option “speak to a robot” is more popular than the option “speak to an agent” until the company realises that it’s not humans that are calling; it’s the robots belonging to their customers (see Prediction 6).

Wild card: After having tried call center outsourcing, insourcing, offshoring and onshoring, the British MNO EE decides to give robosourcing a go. In the end of 2018, 15% of EE’s incoming call volume is handled by conversational robots. It surprises the operator that in the IVR self-serve tree, the option “speak to a robot” is more popular than the option “speak to an agent” until the company realises that it’s not humans that are calling; it’s the robots belonging to their customers (see Prediction 6).

Prediction 6: The unlimited plan extends beyond the humans in the home

Services charged based on the value they bring, not the gigabytes they consume

The operators that have transitioned to an unlimited mobile data portfolio will in 2018 move on and think beyond humans. It has begun already; the global ‘non-human’ leader AT&T had 36 million connected devices in September.

The operators that have transitioned to an unlimited mobile data portfolio will in 2018 move on and think beyond humans. It has begun already; the global ‘non-human’ leader AT&T had 36 million connected devices in September.

Many of these are connected cars where AT&T has been a pioneer in offering plans that include unlimited data. In the same way as a human now pays for the service of being connected – without anybody counting gigabytes – the connected car is a service that, yes, connects a car.

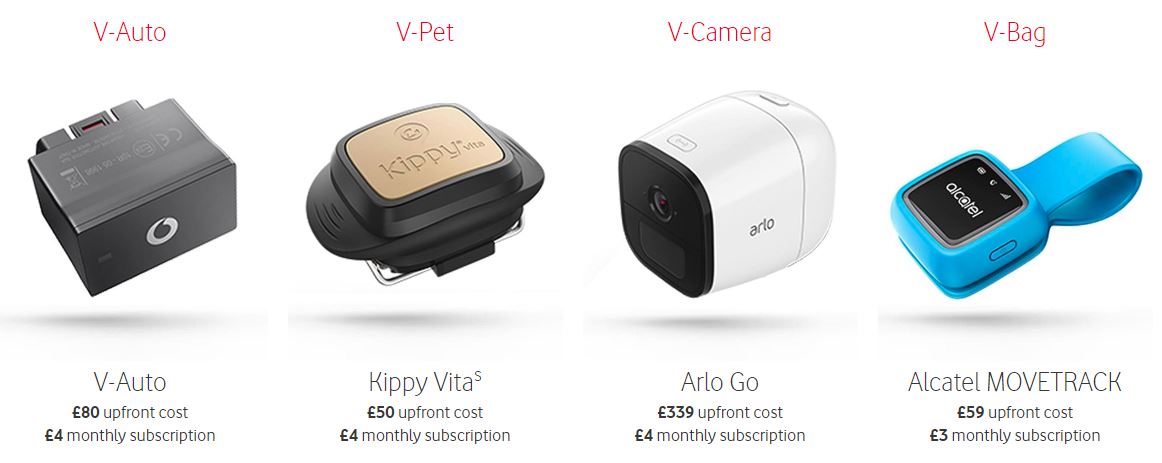

Also the home should be connected and become a smart home. The IoT devices in it would have different functionalities – window/door sensors, motion sensors, video surveillance cameras, flooding sensors, smart sockets, thermostats – the list is endless – and some of them would connect over Wi-Fi, some over cellular and some over both. It actually doesn’t matter since the value of what these devices do has nothing to do with how many gigabyte they consume. Just as with the human or the car, operators will charge for the service based on the value it brings, not for the usage. V by Vodafone is a step in the right direction – one use case, one fixed price.

And then you have those speakers with virtual assistants such as Amazon Echo, Google Home and Apple Home Pod. They are great, but they don’t have legs.

So in 2018, a Japanese or Korean operator will launch the first plan that integrates also the home robot in a package that satisfies all the connectivity needs in a household – for humans, cars, appliances and robots – not to forget pets. You pay for the service components, regardless of which technology they connect over or how many gigabytes they use.

So in 2018, a Japanese or Korean operator will launch the first plan that integrates also the home robot in a package that satisfies all the connectivity needs in a household – for humans, cars, appliances and robots – not to forget pets. You pay for the service components, regardless of which technology they connect over or how many gigabytes they use.

![]() Wild card: The home robot becomes the ultimate status symbol in 2018 and Google, Amazon and Apple race to launch their variants. Apple’s version is called Sari, Amazon’s Alexi and Google’s Alpha Beth. LG integrates a vacuum cleaner and a lawnmower in its robot.

Wild card: The home robot becomes the ultimate status symbol in 2018 and Google, Amazon and Apple race to launch their variants. Apple’s version is called Sari, Amazon’s Alexi and Google’s Alpha Beth. LG integrates a vacuum cleaner and a lawnmower in its robot.

Prediction 7: Churn is dead

Telecoms becomes the most loved industry of all in 2018

Based on excellent implementations of customer-centric transformation plans combined with state-of-the-art utilisation of big data in marketing and sales, customer service and networks, telcos in 2018 find themselves in a position where they are in total synch with customer preference at all times.

Based on excellent implementations of customer-centric transformation plans combined with state-of-the-art utilisation of big data in marketing and sales, customer service and networks, telcos in 2018 find themselves in a position where they are in total synch with customer preference at all times.

There is no longer any need have lock-in contracts; customers stay because they love their telco. The right individual match between actual usage and price on a real-time basis gives customers a never-before-seen level of peace of mind, a Nonstop Retention Index of 100 and an NPS score of 100. Not a single customer churns in the fourth quarter of 2018.

Wild card: Come on. That prediction was undaunted enough.

Those were our seven predictions for 2018. A year from now, we’ll measure the outcome. We hope we are right, but suspect that one might not come true.