Without subscription growth it’s difficult for mature market operators to report service revenue growth.

Some operators – anxious to still show growth – have thus begun to regularly highlight their fixed-mobile convergence base in quarterly results presentations. It’s most often a smoke screen. Here are seven examples – of which six aren’t growth stories.

These examples are designed to look like growth, but it’s most often not. It’s simply migration from one plan to another.

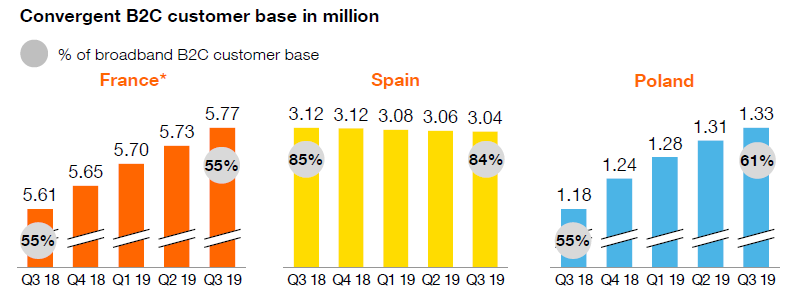

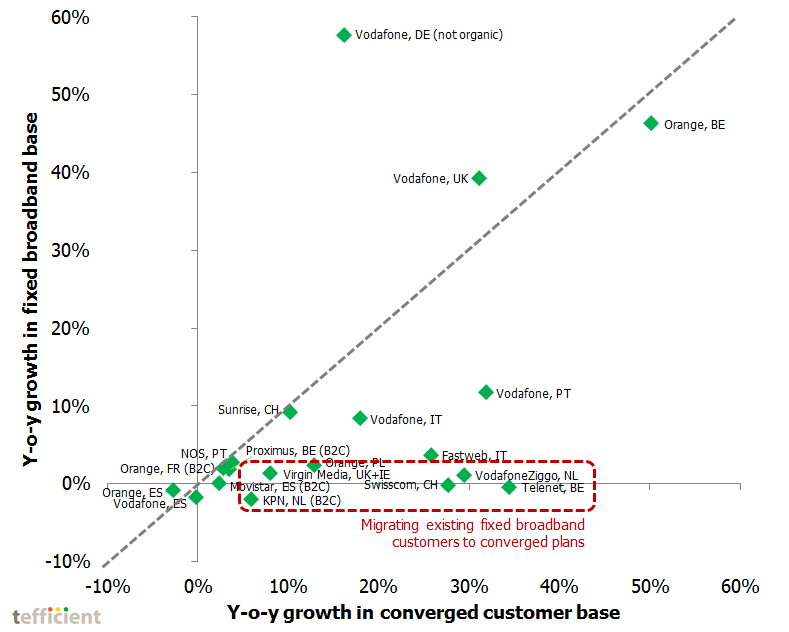

Take a look at our graph below. It compares the y-o-y growth in the converged customer base to the y-o-y growth in the fixed broadband base.

With few exceptions, the growth in the converged customer base is much faster than the growth in the fixed broadband base. The only operators in our European sample that could be seen to use convergence to grow its fixed broadband base, taking market share, are Orange in Belgium, Vodafone in the UK and Sunrise in Switzerland. (The position of Vodafone in Germany is heavily affected by the acquisition of Liberty Global’s Unitymedia in Q3 2019.)

The operators in the box highlighted in red are essentially just migrating existing fixed broadband customers to converged plans. There is no growth in the fixed broadband base and these operators are thus not taking any market share – even if the snippets from the investor presentations above speak about the growth in convergence base.

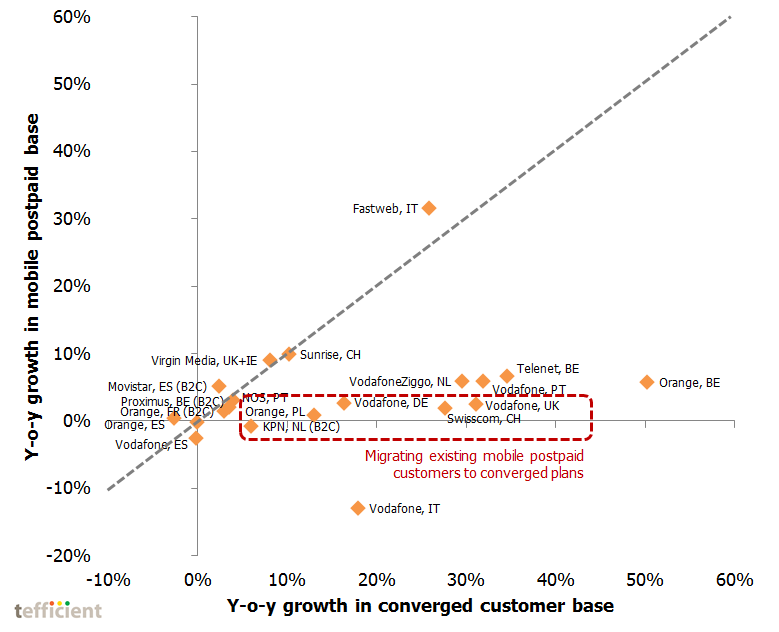

If we instead plot the y-o-y growth in mobile postpaid base vs. the y-o-y growth in converged base, it looks a bit better.

One reason to this is that there’s an underlying prepaid to postpaid migration trend in all markets; it elevates the dots a bit from the zero line. That trend has little to do with convergence.

In reality there are few operators that can turn their growth in converged customer base into any significant growth in mobile postpaid base. Virgin Media, Sunrise and Fastweb are the exceptions. Note that Virgin Media and Fastweb both are MVNOs – and that Sunrise is again identified as a positive exception.

In an industry looking for a growth formula, fixed-mobile convergence has, as shown, become a general way to try to demonstrate growth. This seems particularly true for incumbents such as Telefónica, Orange, KPN, Proximus and Swisscom. But a reported growth in FMC base is seldom relevant.

The proof for a successful FMC proposition is instead found in how the total revenue, EBITDA and churn develop.

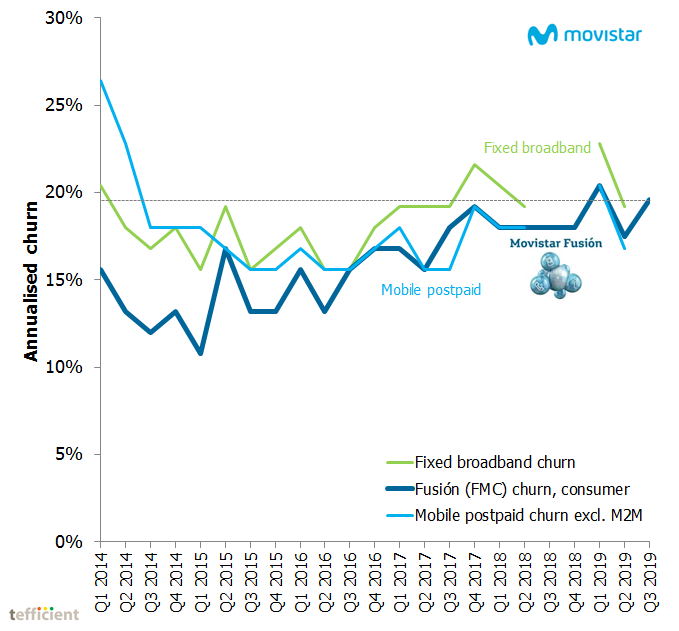

Please don’t regard FMC as a universal solution for customer churn either. The graph below shows how Movistar Spain’s churn developed between 2014 and today.

When the FMC plan Fusión was new, customers on Fusión had a significantly lower churn than what the overall fixed broadband and mobile postpaid churn were.

Little by little as Fusión penetration grew, the difference shrunk. Today there’s no churn benefit of FMC vs. the overall churn levels for fixed broadband and mobile postpaid. When 89% of Movistar’s fixed broadband consumer customers are Fusión customers and 85% of Movistar’s mobile postpaid consumer customers are Fusión customers, there’s simply no reason why there should be a churn differential any longer. And there isn’t. FMC customers churn as often as any customer. But the FMC churn grew a lot from its lowest point in Q1 2015. From a churn point of view, Telefónica is back to where it started.

So when an operator reports lower churn for FMC customers while still expanding the FMC base: Don’t be fooled. It will not last for long when operators strive to push the FMC penetration level upwards. The reason is simple: Customers are loyal if they are satisfied. Only satisfied customers would consider buying more from the same operator. In the beginning, the FMC base will consequently consist of the most satisfied and loyal customers. No wonder churn goes down – it’s a club for happy, loyal and likely price indifferent customers; often on binding contracts.

The rest of the population don’t have those characteristics. The only way to get really high FMC penetration is then to say no to a significant part of the market. That’s also why FMC-embracing incumbents, as shown, have such a difficulty to grow total base. One size does not fit all.

But for challengers FMC seems to work as long as penetration levels are moderate.

If you are a customer to Tefficient, ask us for the scatter chart also for revenue.