The Q3 results just reported by Telia Company, Telenor, Tele2, 3 Scandinavia and Elisa show that it’s quite difficult not to be successful as a Nordic telco today.

Revenue and ARPU is growing. OPEX grows too, but slower than the revenue, so the EBITDA margins are increasing. Churn is decreasing. CAPEX is in decline. More cash is being generated.

We have identified seven signs that competition in cooling down in Nordic telco.

Sign 1. Mobile ARPU grows

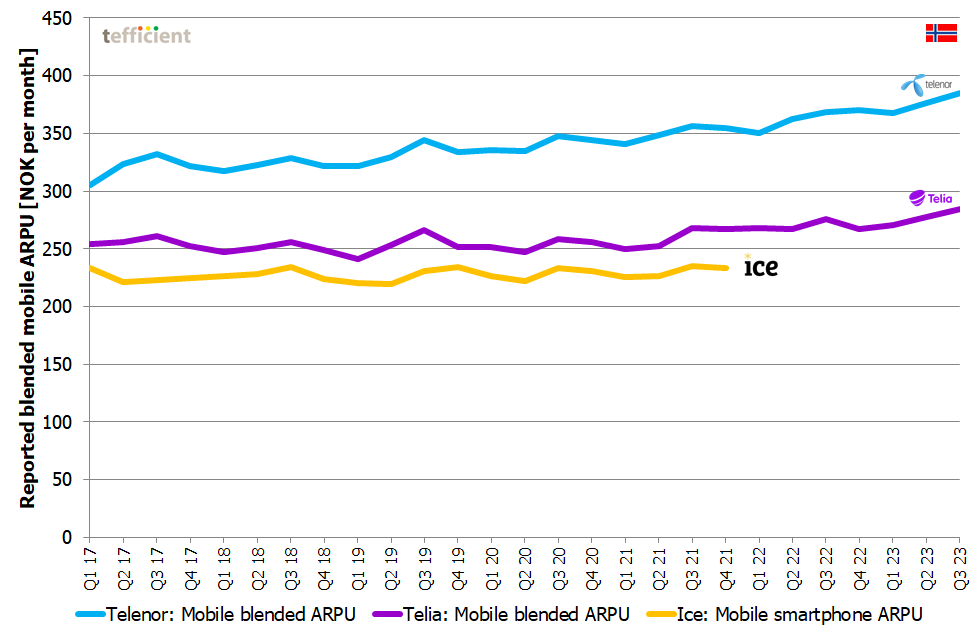

Let’s start with Norway. The reported blended mobile ARPU has quite steadily increased for the two MNOs that still report it. For Telenor it grew 4% year-on-year to Q3 2023. For Telia it grew 3%.

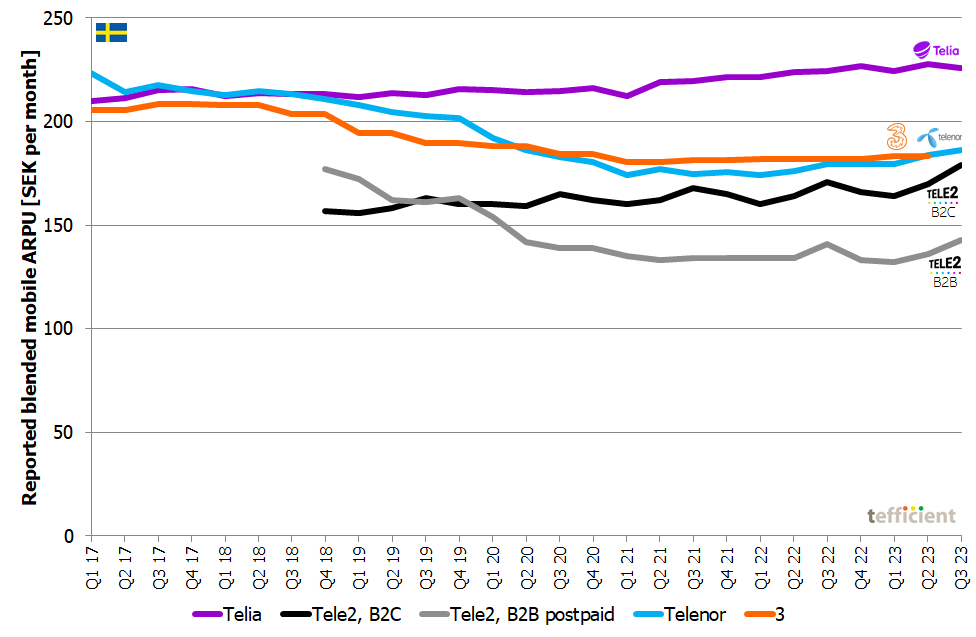

In Sweden, the ARPU development has been a bit more dramatic than in Norway. Three players, first 3, then Telenor and the B2B side of Tele2, witnessed their ARPUs going down from 2018 to the first half of 2021. A corona effect, you might say. Not really; it started before corona started (Q1 2020) and compare with Telia who could keep their ARPU steady or even increase it when 3, Telenor and Tele2 B2B seemingly fought a battle on price.

If we look at the past year trends, Tele2 B2C grew 5%, Telenor 4% year – while all of Tele2 B2B, 3 and Telia grew 1%. For 3, reporting ARPU only every half year, that trend is from the first half of 2022 to the first half of 2023.

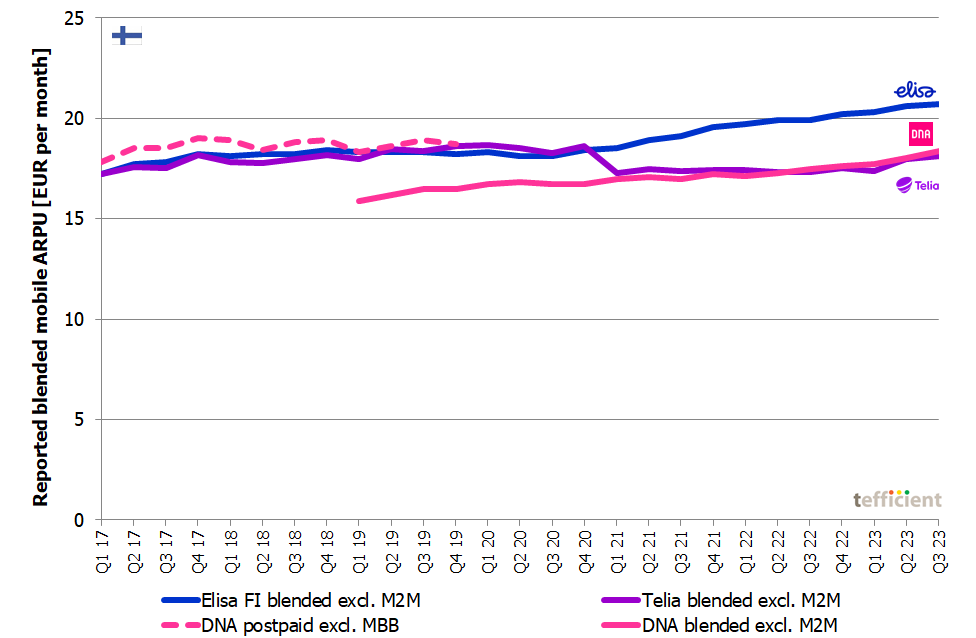

Finland is no exception to our mobile ARPU-increasing trend. Telia has reclassified its ARPU from Q1 2021, but otherwise we see how nicely ARPUs increased in Finland.

The past year trends are that DNA grew 5% while Telia and Elisa both grew 4%.

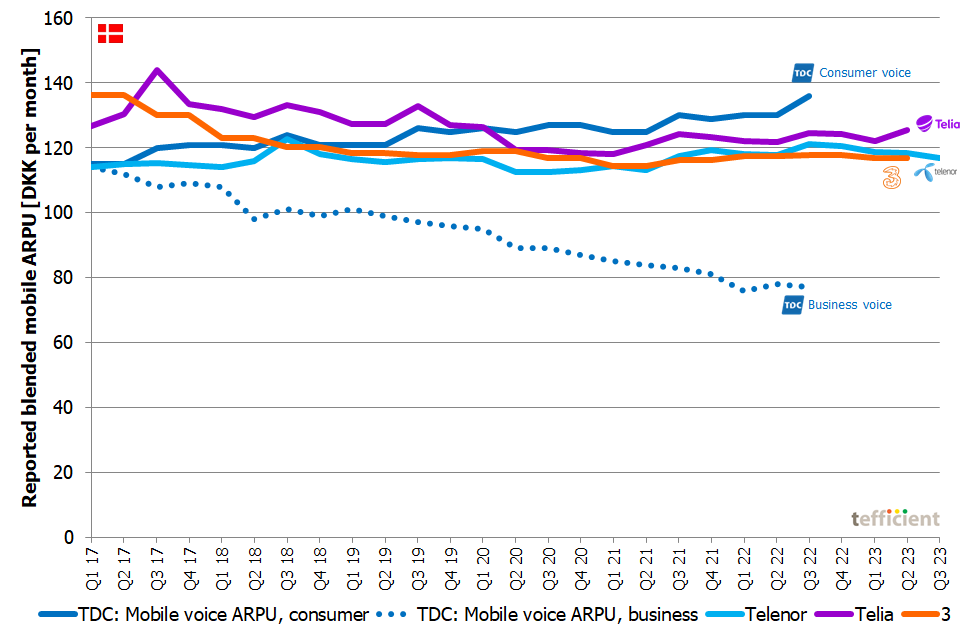

Finally, let’s look at Denmark. The inherited view is that it’s an overly-price-centric market destroyed by competition. But it’s not really the case any longer. As shown below mobile ARPUs have been quite stable. Denmark’s approximate 120 DKK of mobile ARPU translates to 189 SEK – very similar to the Swedish ARPU. Denmark’s ARPU corresponds to 16 EUR – a couple of Euros below the Finnish average. It’s only versus Norway that Denmark’s ARPU stands out as low: 120 DKK is 190 NOK – which is much below the Norwegian ARPU.

Ever since the largest mobile operator, TDC split up into Nuuday and TDC NET, Nuuday is not reporting ARPU, regretfully. And as Telia Denmark is about to be sold to Norlys, Telia Company from Q3 2023 only reports some few, basic, financial stats. But Telenor is still reporting; if we calculate its past year trend, its ARPU fell 3%. Telia’s year-on-year trend to Q2 2023 was up 3%, though. 3‘s was down 1%.

With the exception of Denmark, we see strong growth in mobile ARPU in the Nordics. When ARPU increases, it’s explained by two things:

- Customers using or buying more

- Price hikes – on new subscriptions (front book prices) and old subscriptions (back book prices)

For decades it was a well-known fact that telco prices always go down and never up. The return of inflation in the beginning of 2022 turned this around. For the first time all telco players – at the same time – thought it was a good idea to raise mobile prices. Not just front book prices, but also back book prices. This obviously has a positive impact on ARPU. But it is not a sign of increasing competition.

Sign 2. Fixed broadband ARPU grows

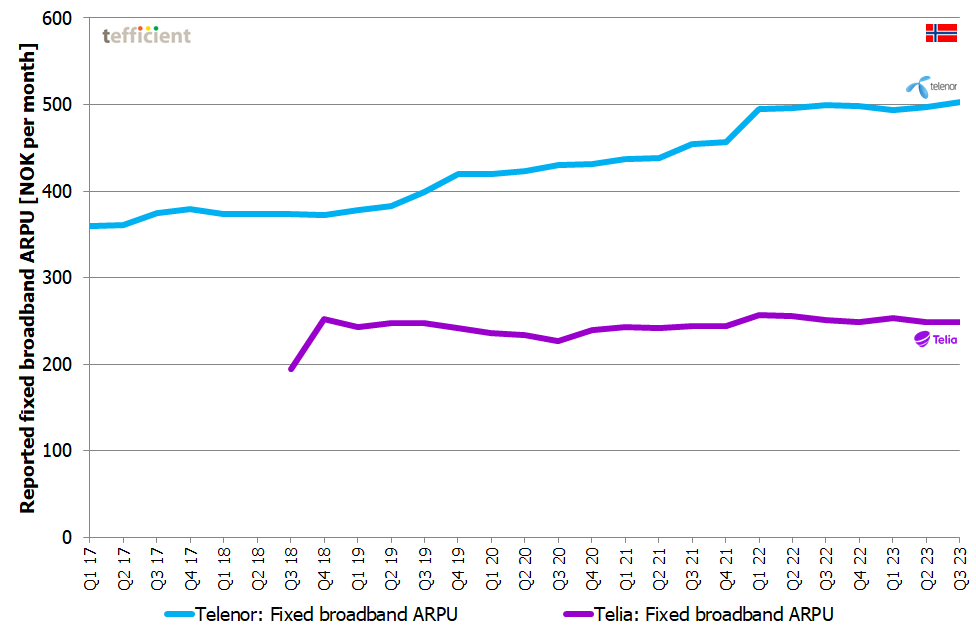

Let’s now see if the fixed broadband ARPU development is different than mobile. In Norway, Telenor has experienced a quickly growing ARPU whereas Telia has been flat. ARPU is regretfully not reported by Lyse or some of the other larger providers in the Altibox family.

In the past year, Telenor‘s fixed broadband ARPU grew 1% while Telia‘s was flat (-0.5%). This is slower ARPU growth than in mobile.

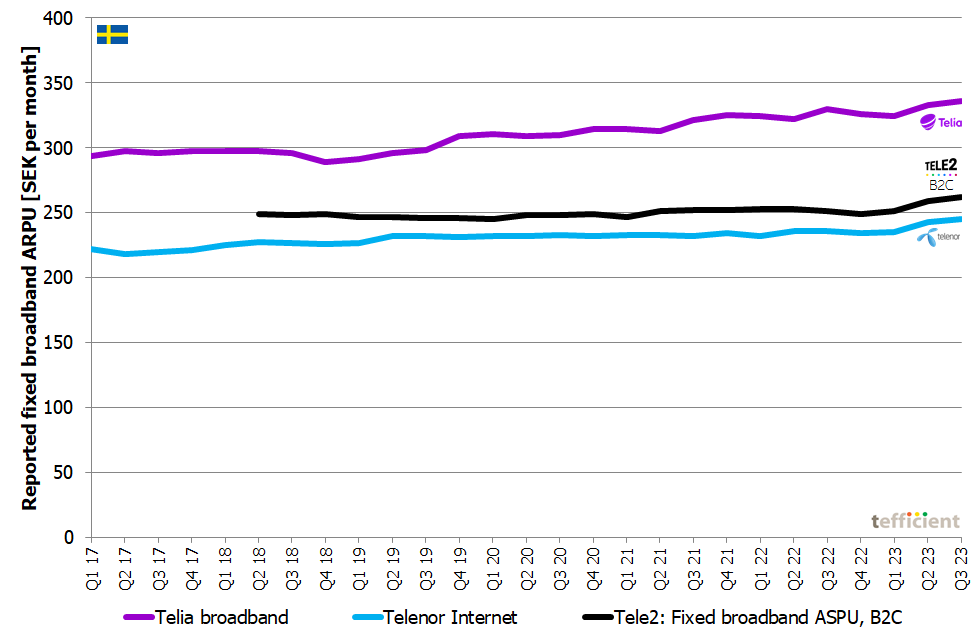

In Sweden, Telia’s fixed broadband ARPU has had a better development than that of Tele2 B2C and Telenor.

In the past year, Tele2‘s fixed broadband ARPU among B2C customers grew 4%. Telenor‘s ARPU also grew 4% while Telia‘s grew 2%. This is in line with the mobile ARPU trends in Sweden.

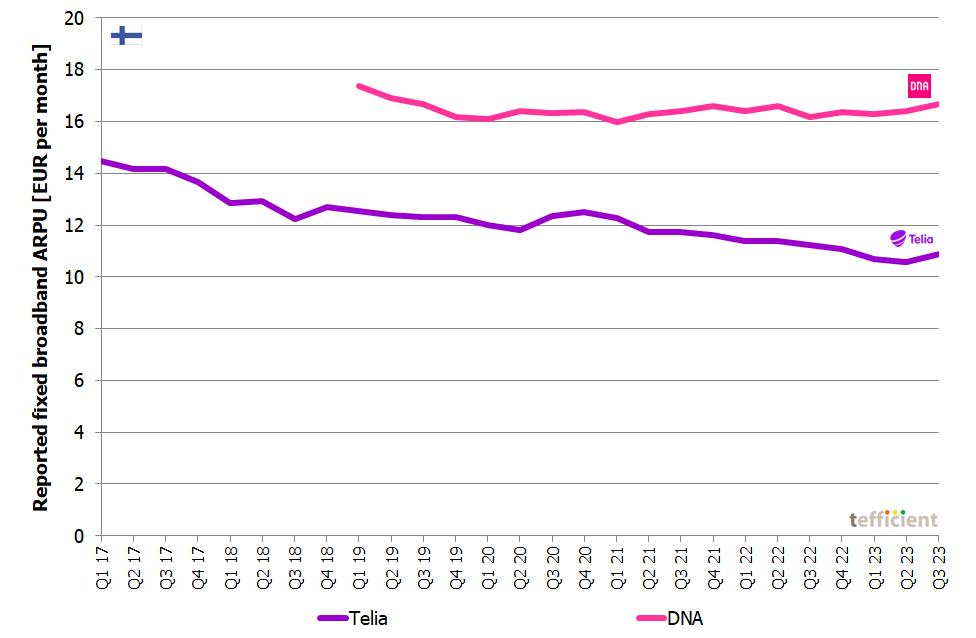

In Finland, fixed broadband has not really been in demand; about 40% of households simply rely on an unlimited mobile data subscription with a router standing on a window sill. The fixed broadband ARPU for the two reporting operators (Elisa does not report) is quite low.

In the past year, DNA‘s fixed broadband ARPU grew 3%. Telia‘s fell 3%. This is slower ARPU growth than in mobile.

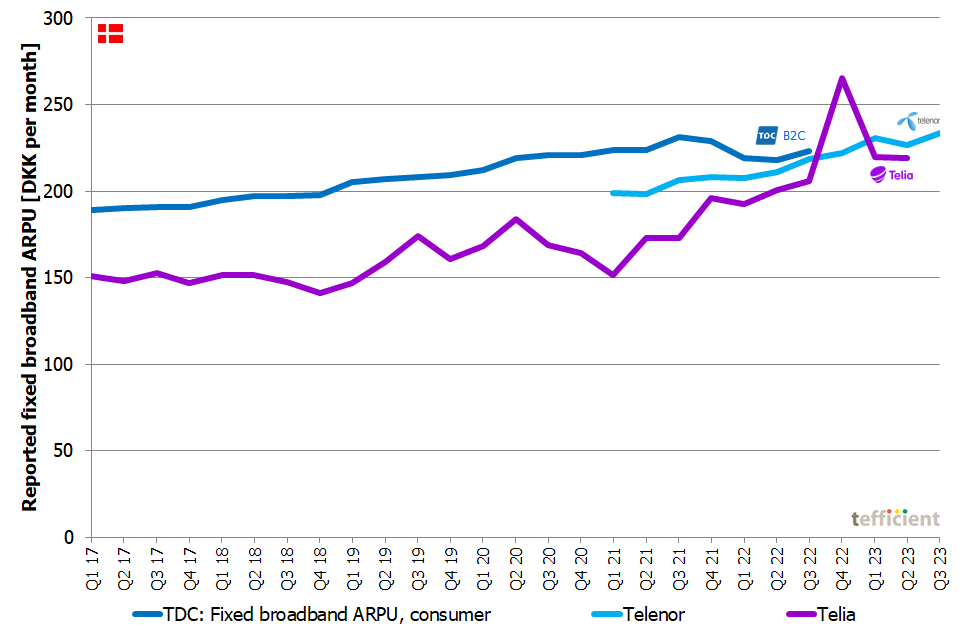

Finally Denmark where the fixed broadband ARPU of the reporting operators generally is increasing. As in mobile, Nuuday (ex-TDC) is no longer reporting and Telia stopped reporting in Q3 2023. Telia’s ARPU peak in Q4 2022 looks strange but is as reported. Telenor started to report fixed broadband ARPU lately retrospectively back to 2021.

In the past year, Telenor‘s fixed broadband ARPU grew 7%. Telia‘s grew 9% from Q2 2022 to Q2 2023. This is much faster than the mobile ARPU.

To conclude, we see strong growth in fixed broadband ARPU in Denmark and Sweden – but not in Norway and Finland. Technology migration from older technologies, like DSL, to better performing technology like fibre could have contributed, but there have also been regular price increases.

Increased prices had a very positive impact on ARPU in Denmark and Sweden. But it is not a sign of increasing competition.

Sign 3. Mobile churn is falling

Sign 1 showed an increasing mobile ARPU in Norway, Sweden and Finland. It would be logical to think that this in itself could lead to an increased mobile churn. If prices increase, some mobile customers would seek cheaper alternatives.

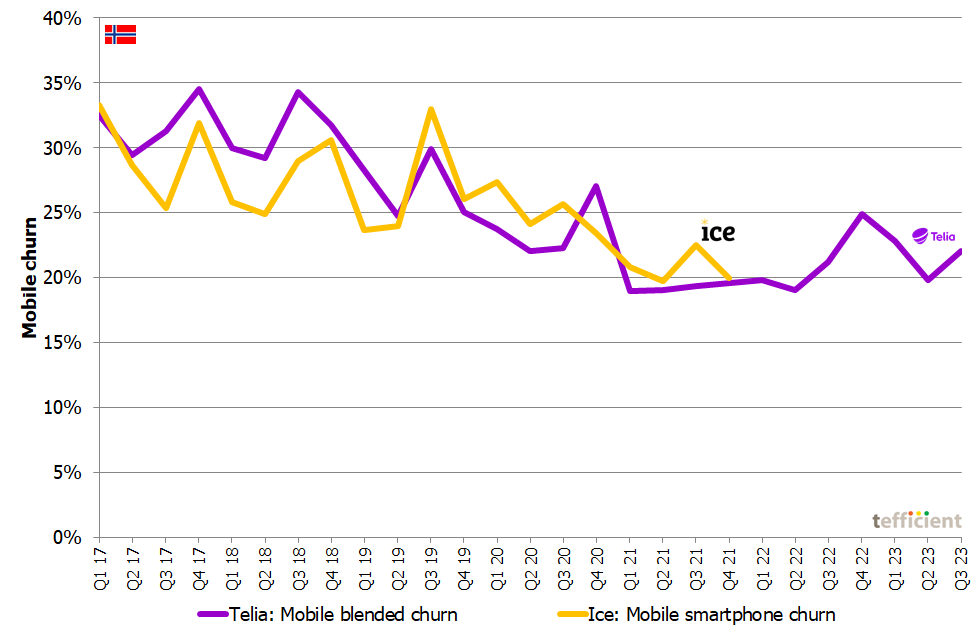

In Norway, the reported mobile churn (Telenor does not report) has decreased since 2019. In our graphs we show annualised churn, i.e. how large portion of the mobile subscriber base that would churn during a year.

For the only remaining operator reporting mobile churn, Telia, the year-on-year trend Q3 2022 to Q3 2023 is however slightly negative: Telia’s blended churn increased 0.8 percentage points.

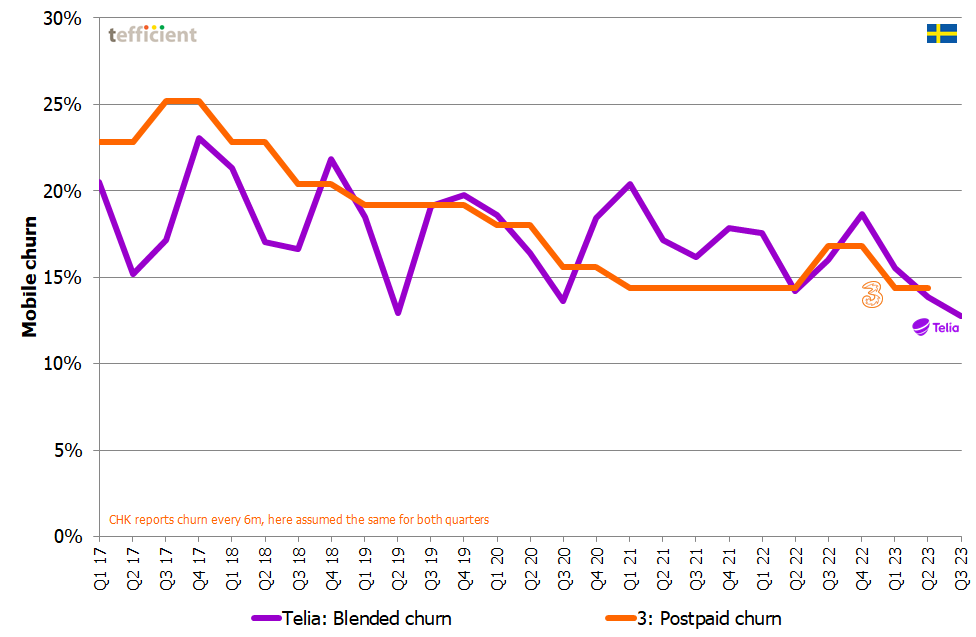

In Sweden, we see that the mobile churn declined for the two operators reporting it (Tele2 and Telenor do not).

Telia‘s blended churn decreased 3.3 percentage points in the past year – to its lowest-ever level. This happened although Telia, as shown in Figure 2, has the highest ARPU and has had the best long-term ARPU development in Sweden. 3‘s postpaid churn (in the 3 brand only) was unchanged from the first half of 2022 to the first half of 2023.

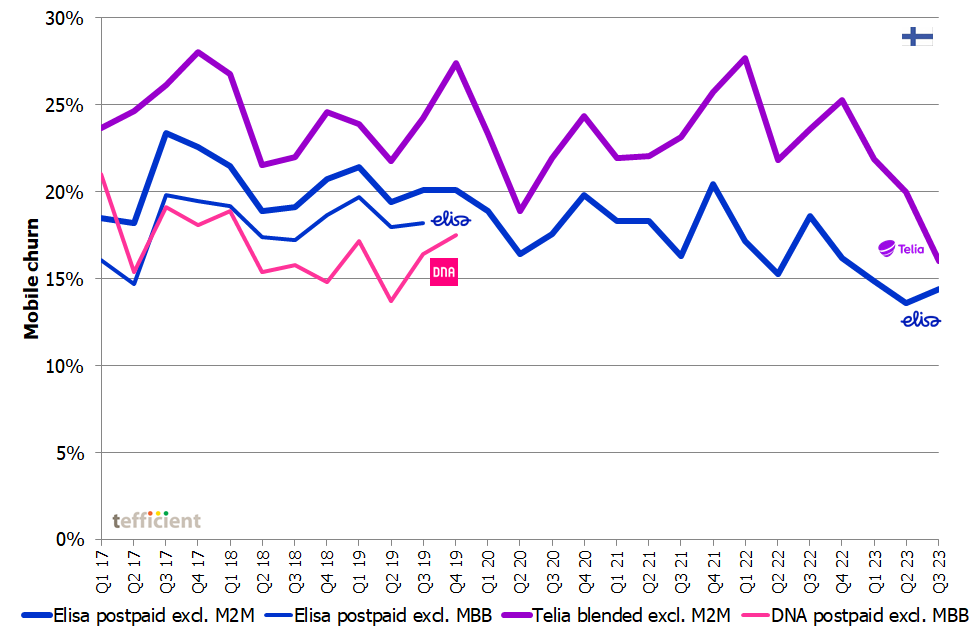

Also Finland has had a good development in mobile churn.

Of the operators still reporting mobile churn (DNA is no longer), Telia‘s blended churn decreased 7.6 percentage points in the past year – to its lowest-ever level – although we in Figure 3 noticed a strong 4% growth in mobile ARPU. Elisa‘s postpaid churn decreased 4.2 percentage points year-on-year in spite of 4% mobile ARPU growth also here.

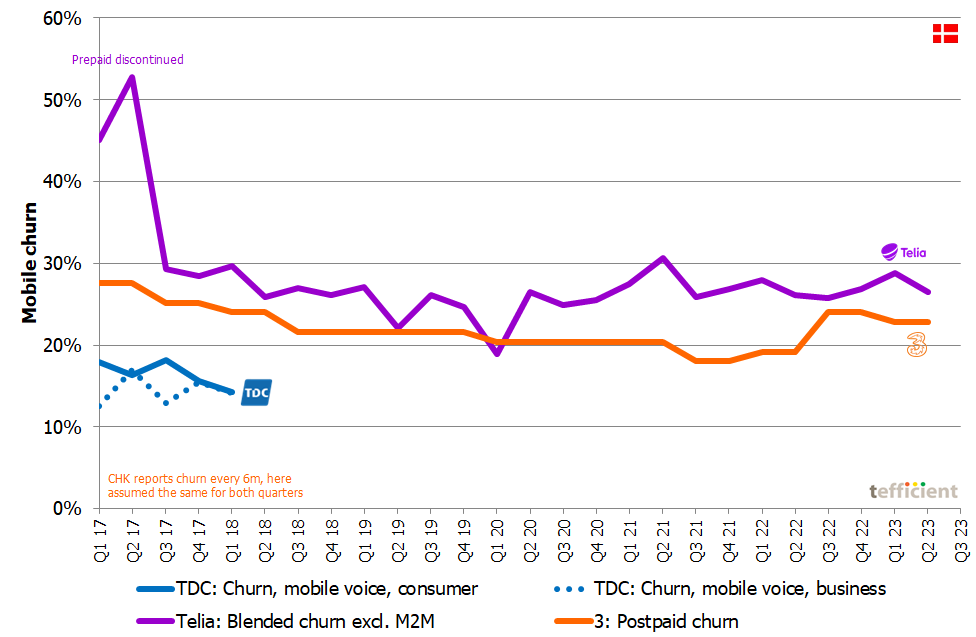

In Denmark, mobile churn seems relatively flat ever since Telia shut down its prepaid business in 2017.

Now that Telia Denmark is reported as discontinued, we will no longer get mobile churn reported for Telia in Denmark. In the year from Q2 2022 to Q2 2023, it increased 0.3 percentage points. In the same year, 3‘s postpaid churn (in the 3 brand only) increased 3.6 percentage points. Note that this happens although Denmark was the only Nordic market where we couldn’t see clear mobile ARPU growth (see Figure 4).

The Nordics is upside down: In markets with strong mobile ARPU growth, most operators enjoy declining mobile churn. In two cases even the lowest ever. Denmark doesn’t have mobile ARPU growth but seems to have increasing mobile churn. Logically, it should have been the other way around. It is not a sign of increasing competition when mobile ARPU grows at the same time as mobile churn declines.

Sign 4. Mobile net adds are stable in spite of lower churn

We just concluded that mobile churn levels have decreased – at least in Sweden and Finland. That’s good news for the sales departments of operators because their efforts will now be visible as net additions, i.e. a growth in the mobile customer base. If the customer bucket isn’t leaking much due to low customer churn, the new customers that are acquired will fill the bucket. It’s easier to report great net add numbers when churn is low.

But are operators having record mobile net adds?

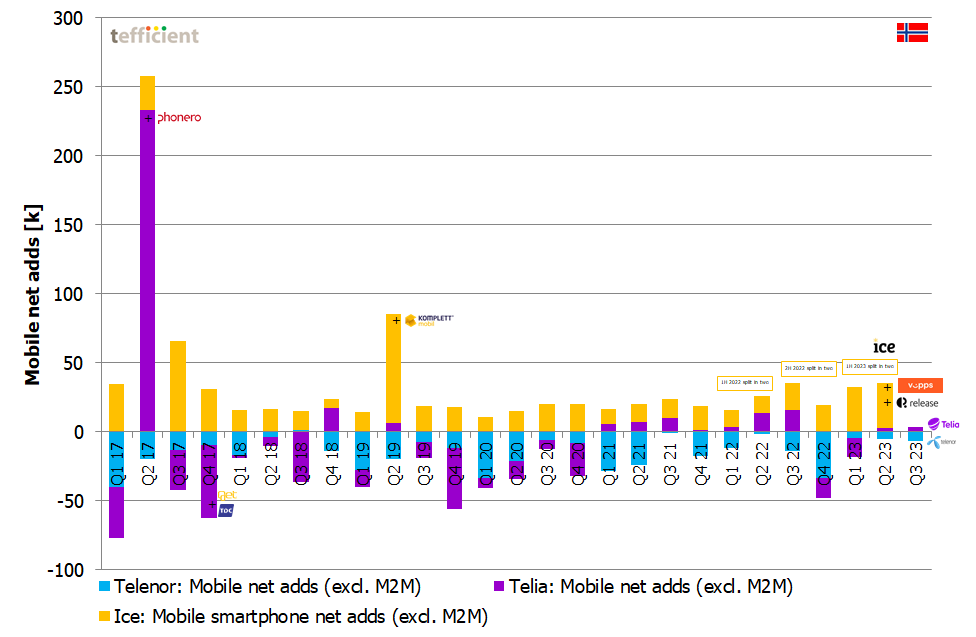

The net add graph for Norway suffers from non-organic growth based on MVNO acquisitions done. The impact is very visible when Telia acquired Phonero and when Ice acquired Komplett Mobil. But Lyse/Ice acquired two smaller MVNOs in the first half of 2023: Vipps Mobil and Release. In total they should have added 29k of the 65k mobile smartphone net adds Lyse reported for Ice in the first half of 2023 (Lyse reports only half-yearly).

Removing these from the Q1 and Q2 2023 bars for Ice would give a picture that has been more or less unchanged in the past four years: Ice’s net adds more or less equal the sum of Telenor and Telia. There’s no sign of any acceleration in the mobile net adds.

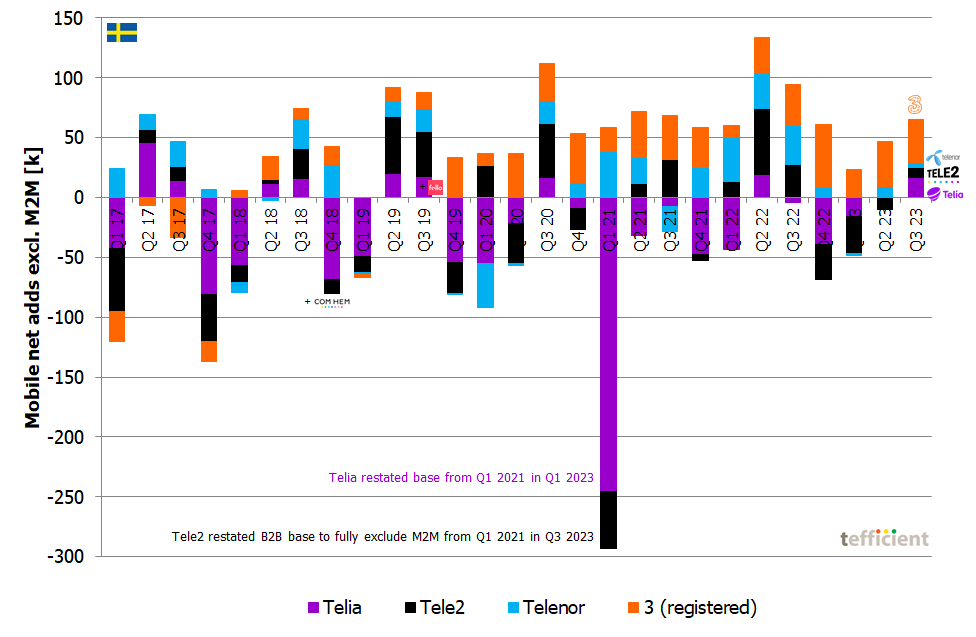

What about Sweden then? Where the largest mobile operator, Telia, had record low churn in Q3 (see Figure 10). Q3 2023 was indeed the first quarter since Q2 2022 that Telia was able to report positive mobile net adds. All other three operators could also report positive mobile net adds, though.

So although Telia seems to have got its net add act together in Q3, its not exactly a Swedish turn-around in net adds. It could suggest that Swedish operators are dropping their sales focus a bit now that the mobile market churn is going down. Not having to sell saves operators lots of money but operators will only do it when the market allows it.

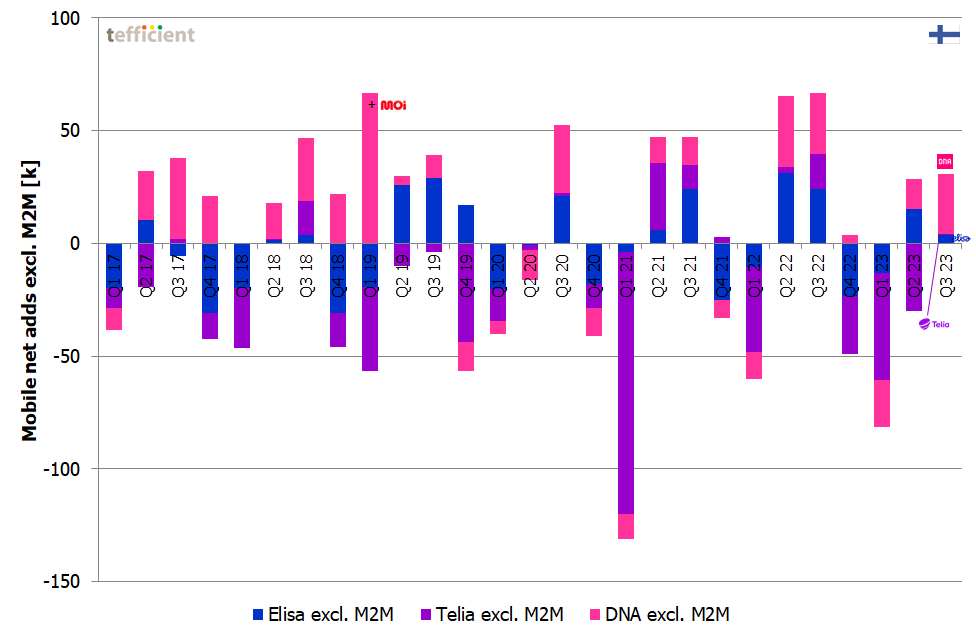

Like in Sweden, we had low or even record-low mobile churn in Finland. Has this led to an explosion in mobile net adds?

Telia, who reported record-low churn in Q3, managed to break even in mobile net adds in Q3. Elisa, who reported its second-lowest churn in Q3, did only grow with 4k mobile subscriptions in Q3. It’s hardly suggesting that Telia or Elisa pushed their sales in Q3. DNA, who doesn’t report churn any longer, had a good net add quarter, but not better than many quarters in the past.

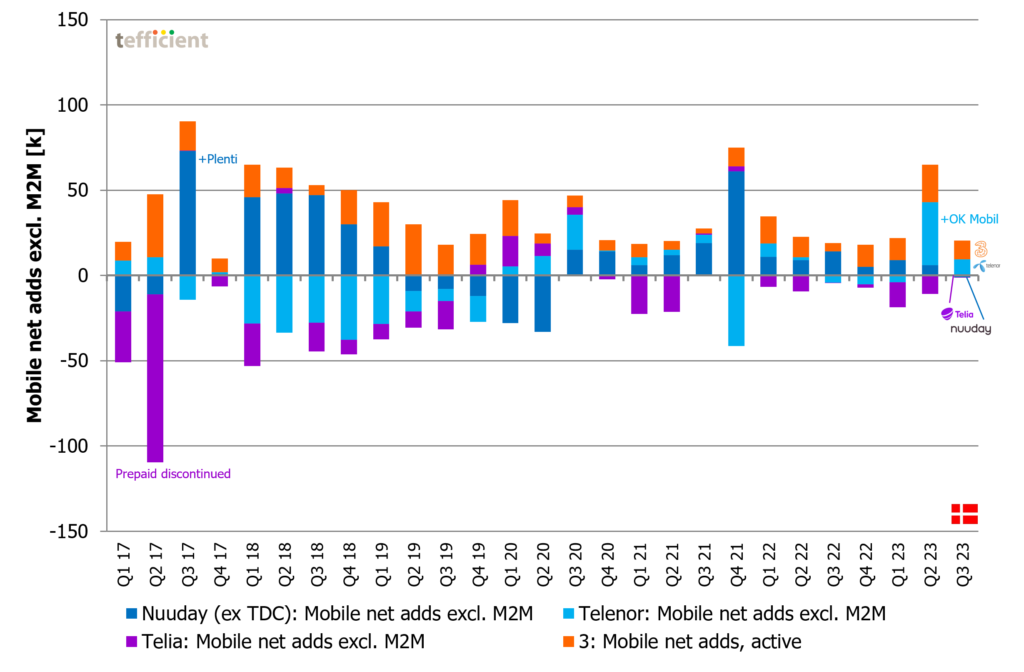

Finally Denmark, where we observed that churn not seems to fall. In its Danish press release, Telia reported its mobile base although Telia Company no longer reports it. Excluding M2M, it was flat versus Q2. 3 and Telenor had some net adds in Q3 while Nuuday had a slight loss of 1k. But the quarter seems to be quite normal quarter. Note that Telenor in Q2 2023 included an acquired MVNO, OK Mobil.

In spite of lowered mobile churn in Sweden and Finland, operators have not been rewarded with an uptick in mobile net adds. This suggests that operators save on their sales efforts now that the market churn allows it. It is not a sign of increasing competition.

Sign 5. Smaller mobile competitors are being acquired and the MVNO market share is low

As already shown in the various net add graphs, Nordic MNOs have acquired several independent MVNOs to either continue using them as sub-brands or to, simply, migrate their customers onto an existing MNO brand.

A few recent examples of this are:

Norway

Ice‘s acquisition of Vipps Mobil with about 19k customers and the MVNO part of Release with about 10k customers. Both brands are today discontinued and Ice have integrated the customers into Ice.

Telia‘s acquisition of 39% of Norway’s largest MVNO, Fjordkraft with about 137k customers, in an agreement where Fjordkraft also changed to Telia as host network. Fjordkraft continues as a mobile brand.

Sweden

It’s not very recent, but an example is Telia‘s acquisition of Fello with 45k customers in 2019. Fello was using Telia as host network. Fello has continued as a Telia sub-brand.

Finland

Finland has never had many MVNOs, but in 2019 DNA acquired Moi with an unknown number of customers. Moi was using DNA as host network. Moi has continued as a DNA sub-brand.

Denmark

If going back in time, we could have given an almost unlimited number of MNO-buys-MVNO examples for Denmark. It was almost as if it was a national sport in Denmark to setup price-focussed MVNOs, quickly acquire a customer base and then sell them to an MNO – most often TDC.

The most recent example is OK Mobil that Telenor acquired in 2023. The number of customers is unknown, but perhaps around 30k. The brand is today discontinued and OK Mobil’s customers were moved into Telenor’s sub-brand CBB (which, by the way, was one of those historically acquired MVNOs). OK Mobil was using Telenor as host network.

What have these and previous acquisitions done to the market share of MVNOs in our four countries?

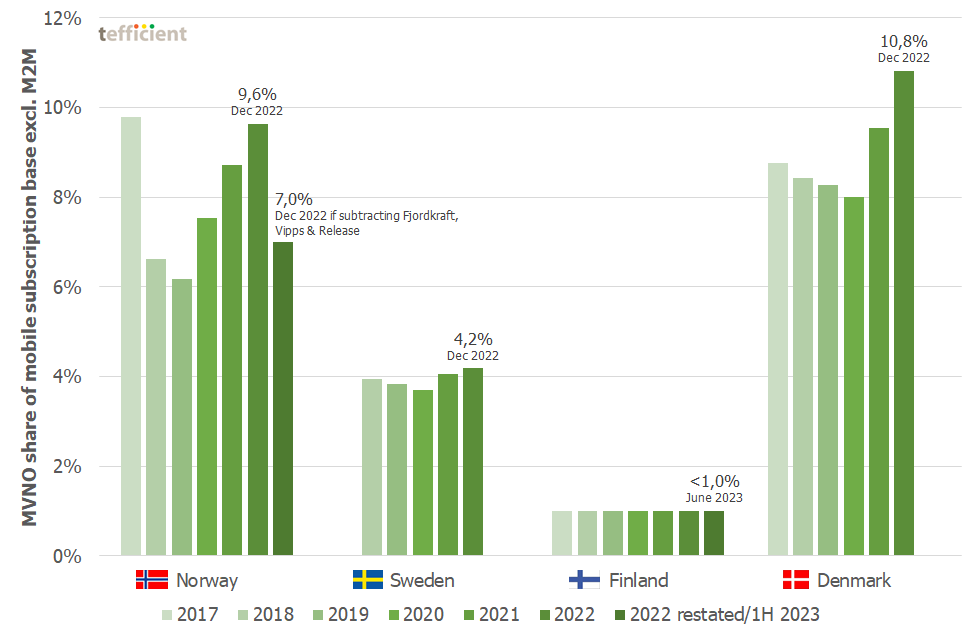

Figure 18 shows that it is far more common with MVNOs in Norway and Denmark than in Sweden and Finland.

Prior to the acquisitions of Fjordkraft, Vipps and Release, Norway had 9.6% of its mobile subscriber base with independent MVNOs. In the last bar for Norway, we recalculated that 2022 result without Fjordkraft, Vipps and Release and got to 7.0%. One could argue that Fjordkraft still should be regarded as an independent MVNO – Telia owns just 39% – but if we do regard it as a Telia sub-brand, the share becomes 7.0%. The largest fully independent MVNO in Norway is Chilimobil with 86k subscriptions in December 2022.

Sweden had 4.2% of its mobile subscription base with MVNOs in December 2022. The largest independent MVNO is Lycamobile with 150k subscriptions in December 2022.

Finland had less than 1% of its mobile subscription base with MVNOs in June 2023. Based on regulator’s Traficom data, we can’t say which MVNO is the largest.

Denmark leads in the Nordic with 10.8% of mobile subscribers with MVNOs in December 2022. After Telenor’s acquisition of OK Mobil, that percentage should have decreased somewhat but the base of OK Mobil is not reported by SDFI.

The MVNO share of mobile subscriber base is generally low in the Nordics – and particularly low in Finland and Sweden. Recent MVNO acquisitions in Norway and Denmark will reduce the independent MVNO share of base. Few MVNOs reduce the customer choice and low MVNO adoption isn’t a sign of increasing competition.

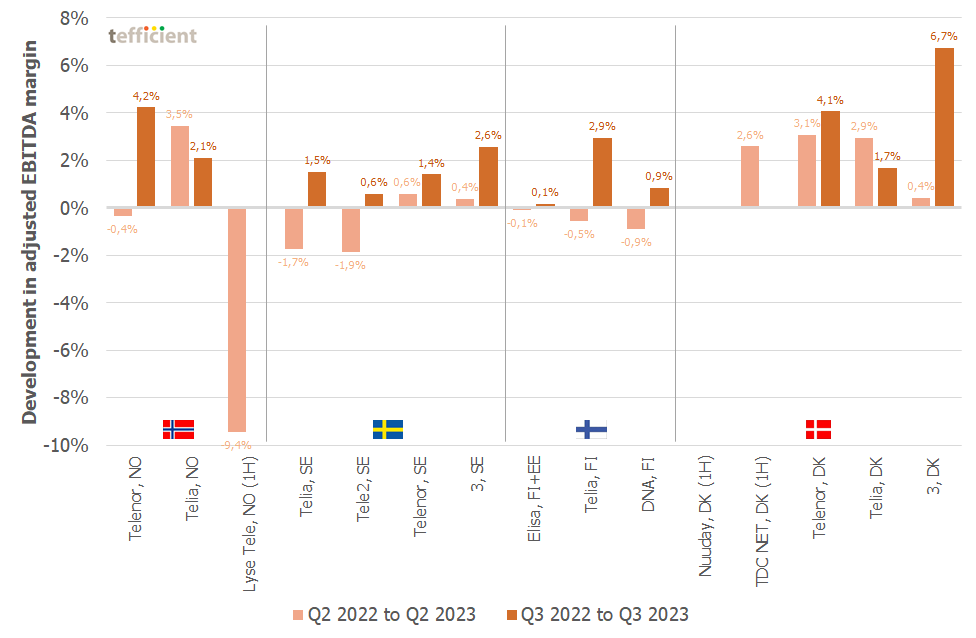

Sign 6. EBITDA margins are going up

We previously suggested that operators can use this period of generally weaker competitive activity and lowered churn to relax their sales aggressiveness a bit. Since customer acquisition and retention is one of the most significant OPEX items for an operator, we should then be able to see this in the EBITDA margins of operators.

And if we can see it, the savings are so large that it actually compensates for much of the inflation-driven OPEX increases in e.g. salaries and rents. What works in the different direction is energy prices that, at least one the spot market, were reduced from 2022 to 2023. It’s however hard to say how much the energy OPEX of operators is affected as most of them rely heavily on hedging.

Half of the operators were able to improve their reported adjusted EBITDA margin in Q2 2023 – but in Q2 2023 all of the operators improved their reported EBITDA margin. And in some cases, like 3 Denmark, the increase was significant (6.7 percentage points in their case).

As always, there are a few fine print comments that need to be made when comparing operator reported financial data:

Lyse‘s dramatic decrease in reported EBITDA margin from, in their case, 1H 2022 to 1H 2023 originates from Lyse’s acquisition of Ice which happened 30 March 2022, i.e. their Q1 2022 is without Ice. Since Ice prior to the Lyse acqusition had a much lower EBITDA margin than Lyse’s telecom business, the reduction in Lyse’s telecom EBITDA is likely solely attributable to the acquisition of Ice. There’s no pro forma available.

For Elisa, due to their reporting, the numbers include also Estonia.

Nuuday, the ServCo part of the old TDC, has now reported its Q3 2023. Although some numbers were reported, the total revenue has been reported for any quarter in 2023. Hence the underlying EBITDA margin can’t be calculated.

The NetCo part of the old TDC, TDC NET will from now on report only half-yearly it seems. It’s EBITDA margin was a whooping 71.5% in the first half of 2023. Given that, TDC NET’s increase of 2.6 percentage points is not as significant as it seems. The increase is likely driven by energy prices as TDC NET does not have retail customers.

The EBITDA margins of Nordic operators are at very healthy levels and have increased further in 2023 in spite of the general inflation. Price increases have contributed positively – and so has the decrease in spot market energy prices. Another contributor is the much lower churn observed in some of the Nordic markets which has allowed operators to achieve the same net adds albeit using less in sales cost. It suggests that competition at present isn’t as tough as in the past.

Sign 7. Price hikes start in the low end

Under Sign 1, we noticed that mobile ARPU increased for most operators in the Nordics, with the exception of Denmark.

When mobile providers raise prices, they seem to want to avoid making their more premium plans less attractive – as that could limit their ability to upsell. Instead, the price increases seem to be done in the low end and then particularly in the price fighting brands that historically provided the mobile subscriptions with the lowest monthly rates.

This tactic, to adjust the lowest price points upwards, has been key to the gradual improvement of the business results in Denmark and Finland. That journey started long before the inflation comeback in 2022.

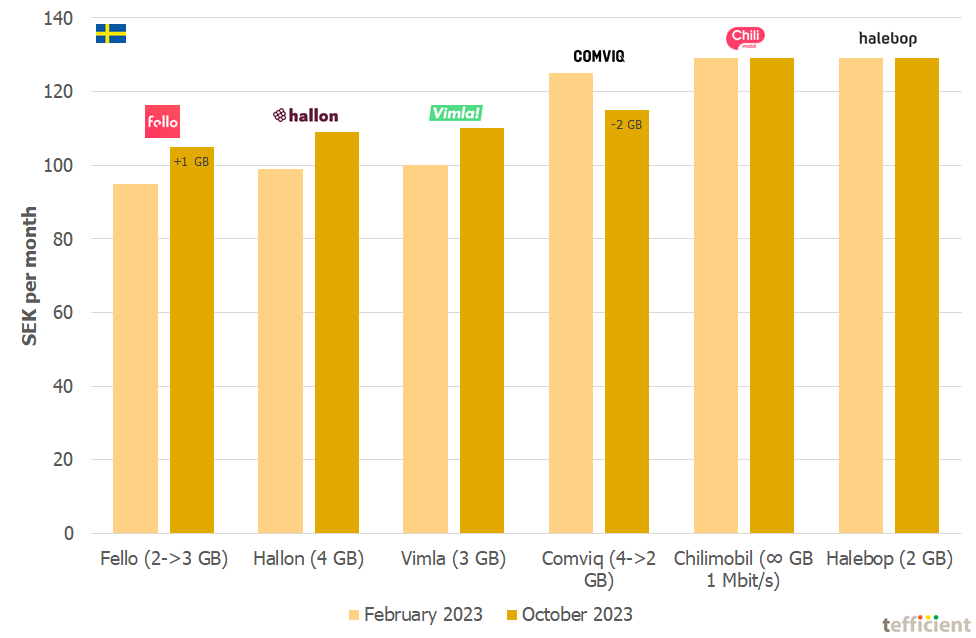

In Sweden, the cheapest mobile subscriptions were sold for just below 100 SEK until March 2023 when Telenor’s sub-brand Vimla decided to raise the prices on all of its plans and then triggered most other sub-brands to consider adjusting their prices too. Vimla’s cheapest plan was raised from 100 to 110 SEK, i.e. 10%.

The graph below shows the cheapest offered mobile subscription by the consumer sub-brands of the four MNOs and by the MVNO Chilimobil.

A month after Vimla, 3’s sub-brand Hallon announced that it would increased all of its prices too. Also for existing customers. To make it simple with 10 SEK regardless of subscription. Hallon’s cheapest plan then went from 99 to 109 SEK, i.e. 10% up.

At about the same time, Telia’s acquired sub-brand Fello announced that it had revised its pricing. The cheapest Fello subscription increased 10 SEK too, from 95 to 105 SEK, but Fello increased the inclusive data volume from 2 GB to 3 GB.

Whereas Telia’s original sub-brand, Halebop, and Chilimobil haven’t changed their prices during these months, Tele2’s Comviq actually lowered its lowest price point by quitely introducing a new 2 GB subscription for 115 SEK. The previous entry plan was 4 GB for 125 SEK – that plan is now 145 SEK but with 5 GB.

Although we have exemplified this only with Swedish price data, mobile operators seem to follow each other and favour to raise prices in the low end. This has a positive impact on ARPU, especially when applied also to back end prices. Increased prices is not a sign of increasing competition.

All in all

The four Nordic markets studied here are not all behaving in the same way, but in this long post we note that the following trends apply to most of the markets:

- Mobile ARPU grows

- Fixed broadband ARPU grows

- Mobile churn is falling

- Mobile net adds are stable in spite of lower churn

- Smaller mobile competitors are being acquired and the MVNO market share is low

- EBITDA margins are going up

- Price hikes start in the low end

Although most of these trends are positive to the industry, they are also signs of that competition has cooled down in the Nordic markets.

The style of communication from particularly Telia Company and Telenor on their Q3 2023 results was this time quite bullish.

Our question is to what extent those good results were rather driven by more relaxed competition?

What’s cooking when it comes to regulation and competition?

The Norwegian telecom regulator, Nkom, has recently communicated that it sees a ‘competitive’ national third mobile network, i.e. Ice, as an important competitive factor. Ice has recently been acquired by Lyse and a new ambitious rollout plan which will more than double the number of sites is now being implemented. If this would allow Ice to also become a host alternative for MVNOs, it could make it more attractive for MVNOs to establish themselves and grow in Norway.

Sweden, Finland and Denmark all have three national networks since long already, so that competition issue doesn’t exist there. But, as shown, the MVNO market is apparently not very dynamic or attractive in Sweden and Finland. What prevents MVNOs to be as successful in Sweden and Finland as in e.g. Denmark?

In the Norwegian fixed broadband market, Nkom wants to move from national regulation to regional regulation. Nkom proposes that broadband providers in 12 of the 22 regions should open their fibre networks to competition. Open fibre networks are already the norm in Sweden and Denmark and exist also in Finland.

In spite of this, the Swedish regulator, PTS, proposes to regulate the single-family home fibre access market. PTS assesses that the competition is working in multi-family homes and hence doesn’t propose any regulation in that part of the market.

In Denmark, the competition regulator Erhvervsstyrelsen divided the country into 21 areas and assessed that 14 operators had significant market power (SMP) in 17 of those 21 areas. Some of these operators made regulatory commitments and were removed from the SMP list. Erhvervsstyrelsen imposed regulatory remedies on the remaining operators. The EU Commission however open an investigation regarding the market review in five of the 21 areas. Erhvervsstyrelsen then withdrew its SMP designation for four of the five markets investigated by the Commission. Only one provider, AURA, remained to be regulated and the Commission accepted this.

So, while that process didn’t result in any real change of the competitive situation in Denmark, the acquisition of Telia Denmark by Norlys might. In spite of having been in the market for decades and in spite of acquiring competition like Orange, Telia never managed to become a strong contender in Denmark. The regional energy company Norlys built Denmark’s largest fibre network reaching about 800k households. That network is open for other ISPs. In its retail business, Norlys has about 500k fixed broadband retail customers. Telia Denmark never had any fixed network and only had very few fixed and TV customers. The combination of Norlys and Telia could lead to a competitor capable of challenging Nuuday (former TDC) in the fixed-mobile converged (FMC) space.

Recommendation

So, some change might come. Until then, there are signs that the competition in the Nordics is cosier than what it has been in a long time. Seven signs.

We therefore recommend Nordic telcos celebrating their business success to stop it. The risk is that your organisations think that the job is done (hint: it never is) and thus stop chasing customer satisfaction, cost and productivity improvements. We welcome all that want to improve further to take part in our Nordic operator benchmark of 2024.