Reference: Analysis, 2025

Norway’s Ministry of Digitalisation and Public Governance published an analysis on 6 March 2026 commissioned from Tefficient in 2025.

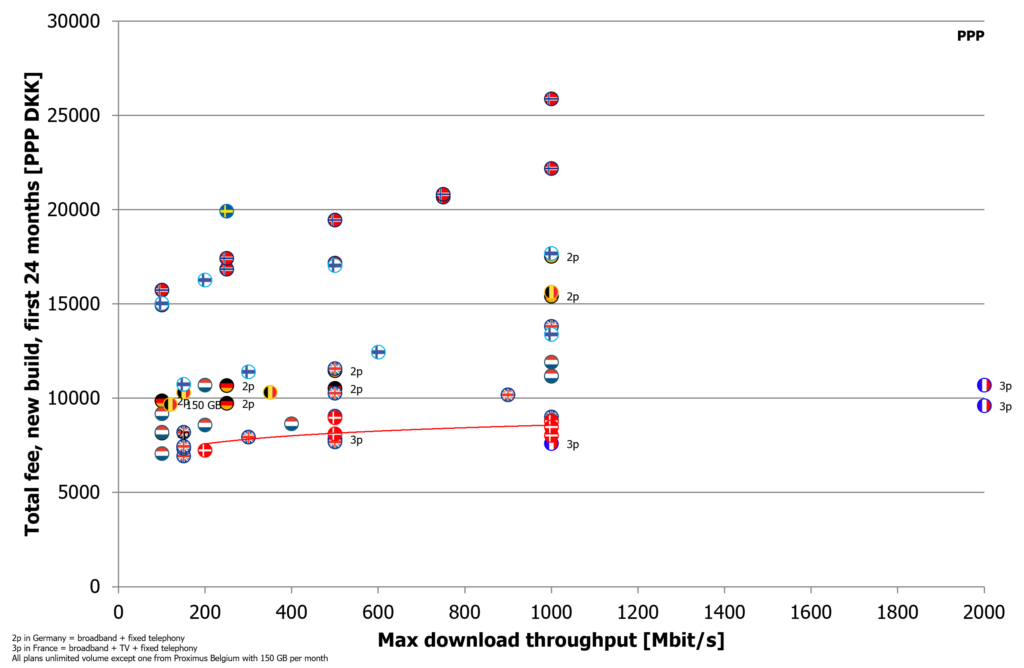

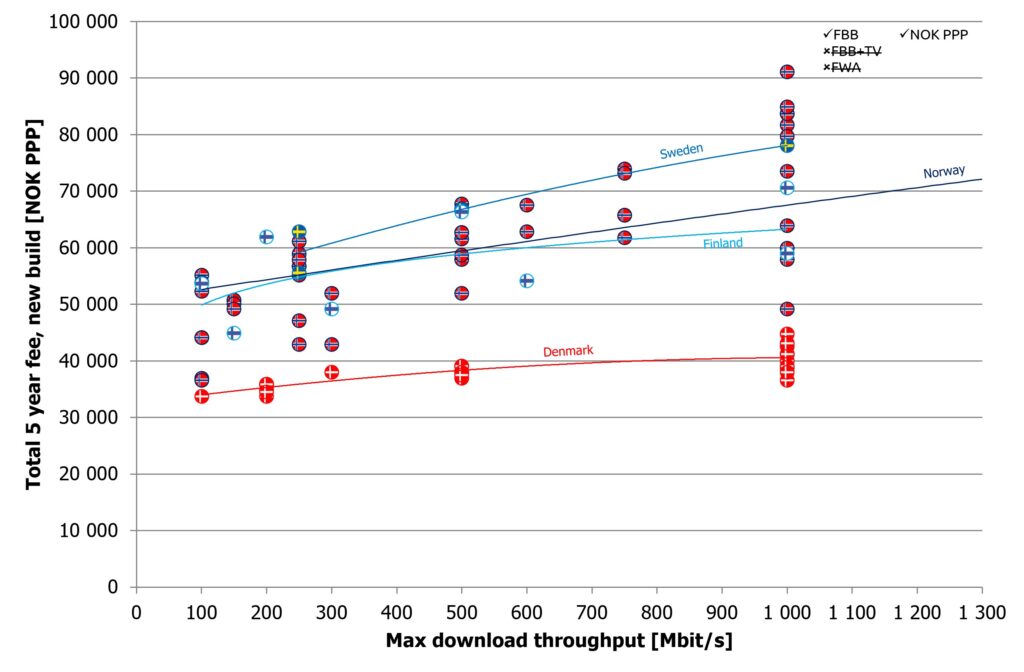

This analysis builds on two previous standalone analyses for mobile and fixed broadband that have been issued four times since 2021, although with less detailed analysis. It focuses on comparing revenues derived from subscribers and assessing selected value-for-money metrics across the four Nordic markets – Norway, Denmark, Sweden, and Finland – for the period up to June 2025.

In addition, the analysis compares market concentration and reviews the financial results of the main mobile and fixed broadband providers.

The analysis can be downloaded from the Norwegian government’s homepage and is written in English.

Commissioned by Norway’s Ministry of Digitalisation and Public Governance.