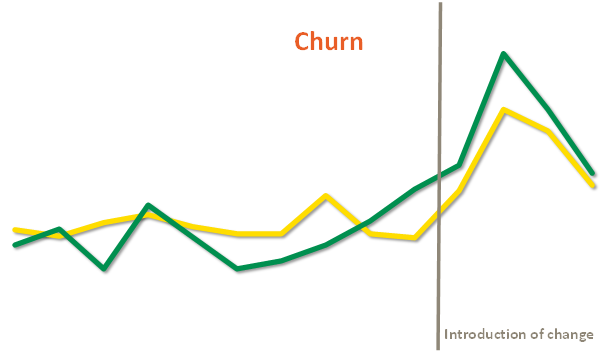

Austria, with a population of 8.5 million, used to have five mobile network operators, making it one of the most competitive mobile markets in Europe. Now there are three left.

When Hutchison-Whampoa, the owner of ‘3’, made a bid on Orange, the European Union needed 11 months to approve it. EU appears to have changed their thinking since. It’s roaming that is under scrutiny now: If operators would agree to abolish roaming fees within EU, maybe EU could be more forgiving to national M&A?

Consequently, European operator executives are publicly advocating the need to cut the number of mobile operators to three per country. If Telefónica’s bid for E-plus in Germany is approved by KPN’s shareholders and by the EU, it will be the ultimate starting signal for Europe’s march towards national consolidation: If it can be done in EU’s largest country, why not elsewhere?

But since Austria serves as the 4-to-3 precedent of Europe, let’s check what the first six months with three mobile operators did to the business results.

Download analysis: tefficient public industry analysis 10 2013 From 4 to 3 Austria

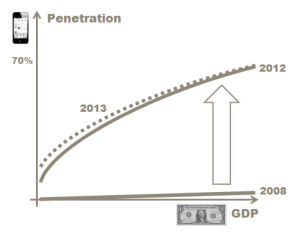

An amazing growth story comes to an end: Smartphone penetration isn’t really growing any longer in mature markets. Smartphones are still sold in high volumes, but the difference is that they’re now primarily sold – subsidised or not – to existing smartphone owners, who upgrades.

An amazing growth story comes to an end: Smartphone penetration isn’t really growing any longer in mature markets. Smartphones are still sold in high volumes, but the difference is that they’re now primarily sold – subsidised or not – to existing smartphone owners, who upgrades.