Which are the equipment sales models in mobile and how have they developed over time? Can best practices be spotted when comparing equipment sales and profitability for a large number of mature market operators globally?

Using facts: What outputs are different equipment sales models such as subsidy, instalment, leasing, rental and BYOD generating – and how is an early upgrade promise affecting?

In this project we identified and documented a few operator best practices across different models in different markets.

Nowhere else in the world will you find as many 5G users as in South Korea. Nowhere else will you find as many 5G base stations up and running. If there ever was a race to 5G, the Korean government and industry won it.

Seeing is believing: After having dug up, read and compiled all reporting and data on Korea’s mobile business there was no other way forward than to seeing it for ourselves and interview people involved in creating Korea’s ‘5G wonder’.

We spent eight busy days (11-18 July) in Seoul to finish a comprehensive 106-page analysis – full of graphs and photos – with recommendations for European operators.

Quantitative and qualitative exploration and analysis project starting with a Nonstop Retention® benchmark for a specific country market.

Analysing a wide area of propositions and tactics from several different markets:

Multi-user and multi-device plans

Fixed-mobile convergent plans

Premium value plans and options

Flexible plans and sub-brands

Early upgrade plans for handsets

Loyalty programmes

Identifying best practice with regards to impact on revenue, take-up and customer loyalty. Applying it to the local market competitive context, resulting in a recommendation presented during interactive workshops.

Mobile operators are abandoning the previously predominant model to subsidize handsets and to, in return, lock customers in on long contracts with elevated service fees.

The death of the model should be mourned by no one since end-users have been given choice and flexibility through a multitude of non-binding, cheaper and flexible service options with generous – or even unlimited – allowances. Operators have seen customer churn decrease as end-users hold onto their handsets longer. As a direct consequence, EBITDA margins have increased.

It’s here. I’ve been salivating after the latest Apple Watch 3, with all the bells and whistles. Slick, beautiful, cool and I’ll only need a watch to make/receive calls and text, stream music, etc. This should be easy, I’ll just pre-order the GPS & Cellular version. I’m a UK consumer and have a passion for all things mobile & telco, both home and abroad. Therefore, I decided to find out how Apple Watch 3 offers compare in the UK, USA and Australia. Continue reading Apple Watch 3 Cellular, how much data does it eat?→

The four largest wireless carriers in the US – Verizon, AT&T, T-Mobile and Sprint – all claim that they have (essentially) abandoned the two-year-binding-contract-with-subsidized-phone model.

At least in the consumer market; the model is still around in the business market.

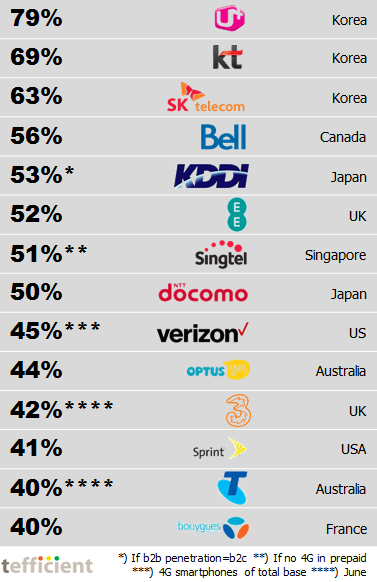

We all know that a significant share of mobile operator revenue is equipment, not service, related. Even though equipment subsidisation and lock-in contracts rapidly become less popular, the reality is that if it wasn’t for subsidisation, reported equipment revenues would be even higher.

When Canning Fok, the co-managing director of

When Canning Fok, the co-managing director of