Analysis & Consulting, 2014

Independently identifying and presenting customer-specific initiatives to increase efficiency to a key customer operator of a global services provider.

Analysis & Consulting, 2014

Independently identifying and presenting customer-specific initiatives to increase efficiency to a key customer operator of a global services provider.

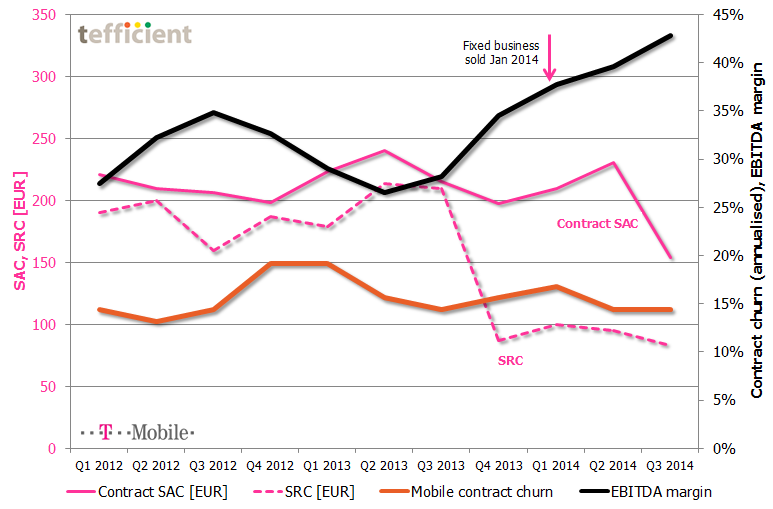

T-Mobile in the Netherlands continues its rally towards higher EBITDA margin: One year ago, it was 28%. Now it’s 43%. T-Mobile’s reported figures shows just how sensitive sales costs are to the mobile business margin.

In Q4 2013, T-Mobile cut its subscriber retention cost (SRC) from a level above 200 EUR to less than half. It has stayed at the new, lower, level since. Even though done during fourth quarter – where margin normally is weak due to seasonal sales – T-Mobile’s EBITDA margin took a leap upwards quarter-to-quarter. Another leap came in Q1 2014 when T-Mobile sold its fixed business (traded under the “Online” brand).

In the just-reported third quarter, T-Mobile’s EBITDA margin took yet a leap: This time due to a significant reduction in contract SAC (subscriber acquisition cost).

The text book says that such dramatic reductions in SAC/SRC would immediately penalise T-Mobile who would experience a shrinking base and market share since existing customers would churn out and new customers would’t join. The interesting thing is that existing customers haven’t left: The orange curve shows a stabilising contract churn of about 15%. T-Mobile has, however, still experienced a decline in their total base, but this has mainly been within prepaid. [The reported reduction in Q3 was almost exclusively to the disposal of the Simpel brand].

According to T-Mobile, the answer to how this has been possible comes in two parts:

In a market where T-Mobile’s two current MNO competitors KPN and Vodafone both go in the converged multi-play direction, it will be interesting to follow if T-Mobile can stay on this route – especially as Tele2 is about to enter the Dutch market as MNO within short.

Analysis & Go-to-market, 2014

Analysis & Go-to-market, 2014

How have operators introduced mobile-fixed convergent quad-play in Europe’s most advanced markets France, Spain, Portugal – and in emerging quad markets like Belgium, the Netherlands, the UK and Germany? How has competition reacted?

Using facts: How have these quad introductions affected market share, churn, acquisition & retention cost, demand for mobile, fibre-speed broadband and TV – and revenue and margin? Which defensive actions can non-convergent operators take?

Which factors can be attributed to effective take-up of quad play? Market share, fibre deployment and homepass, TV offers, exclusive content – or is it just about bundling discounts? What discount levels are we talking about?

Based on international facts and best practice, what would tefficient recommend? Taking local conditions, operator strategy and market position into account.

Commissioned by two operators.

There are two major changes to this benchmark compared to 2013 and 2014:

In total, 16 operators (see above) will be invited to participate. As previous years, the identities of the actual participants will be confidential.

An operator can, depending on business scope, focus or budget, participate in one, two or three of the benchmarks: Mobile, fixed/cable and/or the integrated benchmark.

Integrated operators: Since the mobile-fixed mix is different from one integrated operator to another, integrated operators aren’t just compared “as is”. With tefficient‘s methodology, an operator’s actual mobile-fixed mix will be taken into account on a per-KPI basis making the integrated peer group totally relevant for this specific operator’s mobile-fixed mix.Other modifications to the benchmark are: Improved comparability for equipment sales via subsidy and instalment models; M2M split-out; Improved comparability between telesales in incoming and outgoing calls; Improved comparability between “make or buy” in Networks OPEX & CAPEX; More detailed network quality KPIs.

Mobile benchmark: 603 KPIs derived from a maximum of 376 input data points

Fixed/cable benchmark: 549 KPIs derived from a maximum of 471 input data points

Integrated benchmark: 555 KPIs derived from a maximum of 594 input data points (stand-alone) or just 99 additional input data points (if mobile and fixed benchmarks done)

All three benchmarks cover revenue, OPEX, CAPEX, headcount productivity, performance, traffic & load, quality and innovation & growth for 33 functions.

Deadline to participate is 23 January 2015. Input data (FY 2014) frozen 20 March 2015. Results available 24 April 2015. If you’re among the 16 operators, please contact tefficient for an introduction.

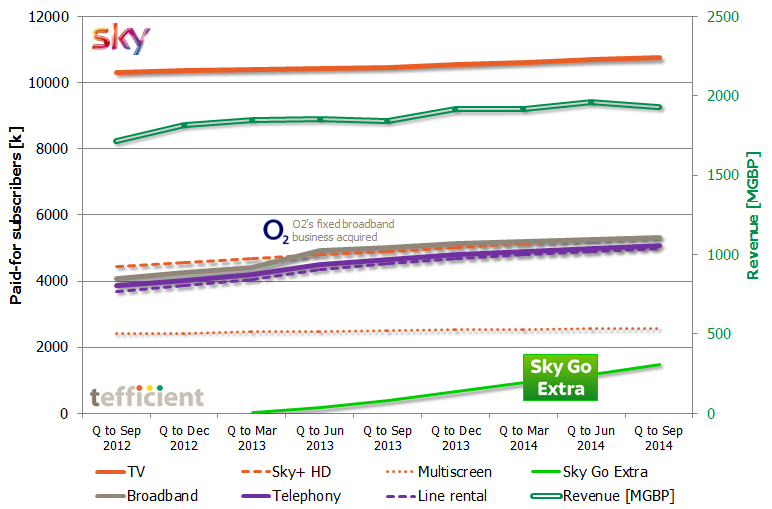

You have to admire the way Sky continues to grow customer base and revenue in the UK and Ireland. Most of us thought that satellite TV belonged in the past century, but Sky has through constant development of their products and offerings, by e.g. integrating broadband, multi-screen and streaming, revitalised and modernised the customer experience.

Have in mind that Sky in this period was challenged by BT who in August 2013 launched BT Sport – their own sports channel with exclusive rights to football games which previously were exclusive to Sky. A channel which BT provides for free to their broadband customers.

Sky is of course at the same time challenged by Netflix and other streaming services. On this part, it’s interesting to note how successful Sky Go Extra is. The “Extra” allows customers to download content to portable devices like tablets and bring it with them – to watch offline. This is a premium service (5 GBP extra per month) whereas the streaming-only variant (Sky Go) is without any extra charge.

This is an indication that people now are ready to pay not to stream. Access to Wi-Fi is unpredictable. Mobile data allowances are typically low in the UK and 4G network coverage is not yet universal. Are we getting tired of streaming?

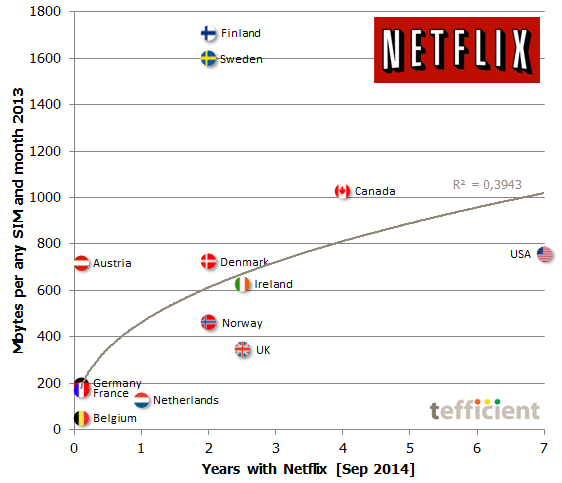

This is a correlation graph that simply had to be done 🙂 We know that Netflix is the single biggest driver of fixed Internet bandwidth in its original market, USA, with up to 40% of downstream traffic at peak hours.

In just two years, Netflix built as large subscription bases as the largest pay-TV providers in some of the European markets launched, so it’s likely that Netflix has a major impact on fixed Internet traffic also in Europe.

One of the benefits with Netflix is portability: It runs on almost any device you might have. Many of these devices – smartphones and tablets e.g. – are often connected over mobile networks. Have the Netflix viewing habits gone mobile beyond Wi-Fi? Can we observe a Netflix effect on the mobile data usage?

The graph correlates the average mobile data usage per any SIM with the number of years Netflix has been in service per country. It’s not perfect, but let’s not dismiss it as just trivia.

Netflix has competitors. The entry of Netflix into new country markets has often paved the way for others (like HBO) when consumers have come to adopt a video streaming habit. Plus that Netflix in most markets have forced incumbent cablecos and satellite providers like Sky to launch portable streaming platforms to complement the traditional viewing experience at home.

This month, Netflix launches in four additional European markets: Germany, France, Austria and Belgium. Austria has high mobile data usage already, but let’s see if the other three laggard markets are elevated.

The equipment instalment plan has proven capable of substituting the subsidy model in mobile – even in traditional subsidy markets like the USA and the UK.

The equipment instalment plan has proven capable of substituting the subsidy model in mobile – even in traditional subsidy markets like the USA and the UK.

While the EIP opens for more competitive service pricing, it also opens for flexibility when it comes to equipment upgrades: Pay remaining instalments – and upgrade. Some operators go further, though:

Realising that customers aren’t particularly interested in obtaining the ownership of (aged) equipment, pioneering operators introduced a variant of the EIP – based on an early return of equipment: The early upgrade plan.

It’s a recurring upgrade promise – often without any additional fee. Take-up has been great, but it’s only now the pioneering operators need to start delivering on this promise.

Download analysis: tefficient industry analysis 5 2014 early upgrade plans 19 Sep

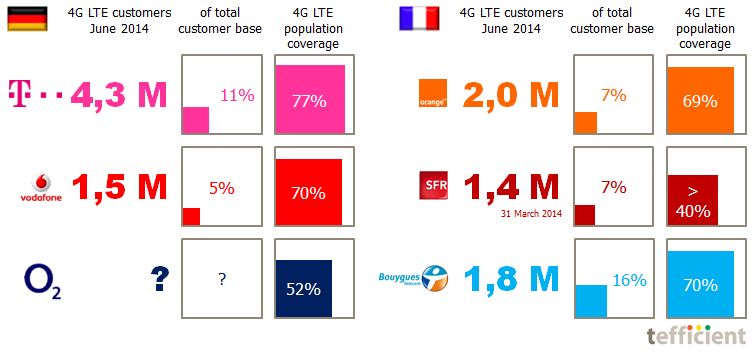

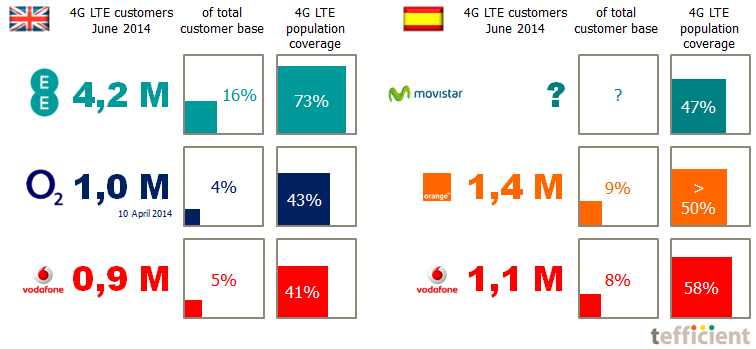

In four of the largest European markets – Germany, France, UK and Spain – we see three out of four mobile operators reporting their 4G LTE rollout status. Most of them also report (or indicate) their 4G LTE customer base.

After much hesitation, the 4G LTE rollout eventually started also in Europe. And you know what? Customers are coming. If they are covered, that is.

The country pictures show the overall market leader at the top. Telekom has the largest 4G LTE network in Germany and had 11% of its customer base on 4G LTE by the end of June.

In France, Bouygues Telecom shows how a small No 3 operator through aggressive focus on 4G LTE rollout can challenge the 2.5x larger Orange on the total 4G LTE customer base. 16% adoption is among the highest in Europe.

SFR – in the process of being acquired by Numericable – didn’t report their 4G LTE figures in Q2. Arcep, the French telecom regulator, however critisised SFR in June for their 4G LTE coverage claims, saying their population coverage was just 30%. [Bouygues and Orange claims were OK whereas also Free was critisised. Their population coverage was said to be 24%].

UK is behind on 4G LTE rollout, partly because of late licensing. Market leader EE was given a head start when it was allowed to refarm 1800 MHz spectrum and use it for 4G LTE.

In Spain, market leader Movistar is behind Vodafone and Orange on 4G LTE rollout. Telefónica doesn’t report the number of 4G LTE customers in Movistar which might be an indication of that it’s low.

Neither E-plus, Free, ‘3’ nor Yoigo report figures on 4G LTE. We see this an indication of them being behind on rollout and adoption. E-plus is now in the process of merging with O2.

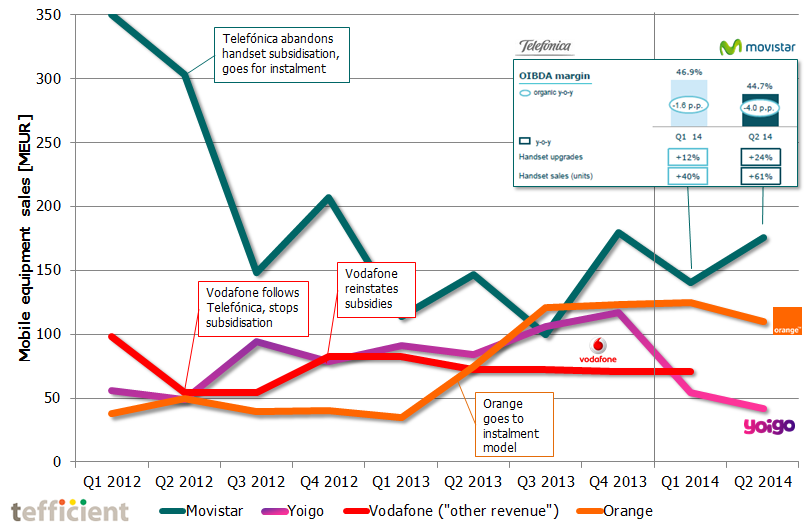

The economic crisis put significant pressure on the Spanish telcos. Telefónica (Movistar) and Vodafone each lost around 4 millions SIMs in the past two and a half years. Orange and Yoigo have fared much better. Yoigo, with its no-frills low cost profile, grew subscriber base from 3 to 4 million at the same time. But suddenly – in Q1 2014 – Yoigo’s total revenue fell 26% quarter-on-quarter.

In TeliaSonera’s new reporting format – implemented Q2 2014 – we could see why total revenue fell: Equipment revenue declined 53% quarter-to-quarter. We could also see that in Q4 2013, 40% of Yoigo’s total revenue stemmed from equipment sales. By any standard, that is high.

Why was it so high? In March 2012, Telefónica decided to abandon handset subsidisation altogether. It had an immediate negative impact on Telefónica’s equipment revenue: From Q2 to Q3 2012, equipment revenue fell from 300 to 150 MEUR (see graph). When Telefónica didn’t any longer discount customer equipment, customers bought it elsewhere. Vodafone followed the market leader and stopped subsidisation as well. Orange did not – and had a few easy quarters during which it churned over customers from Telefónica and Vodafone. Yoigo’s differentiation was instead its low service prices. Many cost-aware mobile users went to Yoigo for this reason, even if it meant that they had to pay the full price of a handset. Yoigo’s service revenue was low, but it was compensated by an increasing revenue from equipment sales…

…until Telefónica decided that they saved enough. The inserted frame in the graph shows that Telefónica grew handset sales 40% in Q1 2014 and 61% in Q2. At the same time, Telefónica’s margin fell. Equipment revenue expanded, but not in line with the number of handsets sold. All this together signal handset subsidisation. Telefónica: back in the game. Yoigo: equipment sales halfed.

TeliaSonera was for a long time open about their interest in selling Yoigo. With the improved results 2012 and 2013, that message changed. But after the Q1 2014 surprise, TeliaSonera put Yoigo back on the transfer list. All of Yoigo’s revenue expansion 2012-2013 was based on hardware sales. A weak foundation when the market leader changes direction.

It’s been more than two years since the June 2012 launch of Verizon’s shared data plan which took out all other Verizon postpaid plans at one go. From this point on, new Verizon customers (or prolonging customers) had to take the Share Everything plan (later renamed More Everything). The initiative was Verizon’s final attempt to get rid of unlimited data and make usage-based data monetisation a reality.

It’s been more than two years since the June 2012 launch of Verizon’s shared data plan which took out all other Verizon postpaid plans at one go. From this point on, new Verizon customers (or prolonging customers) had to take the Share Everything plan (later renamed More Everything). The initiative was Verizon’s final attempt to get rid of unlimited data and make usage-based data monetisation a reality.

Since the standard US postpaid contract is running for 24 months, we should after two years consequently see a 100% adoption of Share/More Everything within Verizon’s postpaid accounts? No, it is 55%.

![]() Verizon’s primary competitor, AT&T, launched their shared data plan, Mobile Share, in August 2012. Unlike Verizon, they kept other postpaid plans available to begin with. More than one year later, in October 2013, Mobile Share was eventually made the only plan. AT&T reports that 56% of their postpaid SIMs are on Mobile Share. Still not 100%.

Verizon’s primary competitor, AT&T, launched their shared data plan, Mobile Share, in August 2012. Unlike Verizon, they kept other postpaid plans available to begin with. More than one year later, in October 2013, Mobile Share was eventually made the only plan. AT&T reports that 56% of their postpaid SIMs are on Mobile Share. Still not 100%.

In its Q2 reporting of yesterday, AT&T says that 80% of postpaid smartphone subscribers are on usage-based data plans. Leaving 20% of smartphone subscribers (plus a bunch of data-only subscribers – no reporting for that segment) that still are unlimited.

Verizon and AT&T’s principal method to convince customers to let go of their unlimited plans has been equipment subsidy: You wouldn’t get any unless you go for the new plans.

But T-Mobile’s disruption of the subsidy model – later embraced by AT&T and (somewhat reluctantly) implemented by Verizon – has led to US customers shifting away from subsidy, instead going for installment plans or BYOD. And with these models, customers can easier hold onto their grandfathered unlimited data plans.