45 million SIMs: The combined EplusO2 will be the largest mobile operator in Germany and in the European Union. A mobile giant was in practice born today with EU’s approval of Telefónica’s acquisition of E-plus.

But during the more than 11 months of approval, the competitive playground changed:

- Vodafone acquired Kabel Deutschland and is about to integrate it in order to offer quad-play

- Telekom developed a new strategy, bringing quad-play to Germany during 2014

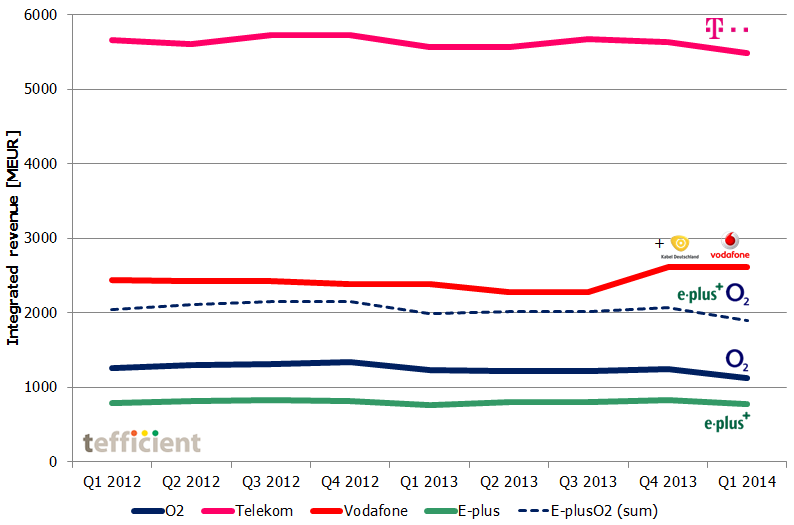

Realising that the future battlefield won’t be mobile-only, we should understand how EplusO2 would rank when it comes to integrated revenue. See the graph above.

When we sum up O2 and E-plus (dotted line), we are no longer looking at market leader. EplusO2 will be number 3.

E-plus is (and has always been) mobile-only. O2 has a fixed arm in Germany, but its share of integrated revenue is just about 25% (and much of it relates to wholesale). What’s worse from a quad-play perspective is that O2 discontinued its TV product by the end of 2013. It never gained more than 90 000 customers – nothing in a country with a population of 82 million.

Telefónica might have something up their sleeve, but the question still has to be asked: Has the mobile-only scale logic behind the merger of O2 and E-plus passed best before date?

We look at what happened to the MVNO businesses when Orange, SFR and Bouygues launched their sub-brands Sosh, Red and B&YOU during second half of 2011 in preparation for the announced launch of Free mobile.

We look at what happened to the MVNO businesses when Orange, SFR and Bouygues launched their sub-brands Sosh, Red and B&YOU during second half of 2011 in preparation for the announced launch of Free mobile.