Fiberalliancen is a trade association representing companies that own, operate, and use fibre networks in Denmark. It is part of Green Power Denmark.

For the fifth time, following previous reports in 2021, 2022,2023, and 2024, Tefficient has conducted an extensive fibre broadband pricing benchmark across nine European markets: Denmark, Sweden, Norway, Finland, Germany, the Netherlands, Belgium, the UK, and France.

“While prices are low, access to fiber networks in Denmark is among the highest in Europe.”

In a press release, Fiberalliancen introduces Tefficient’s latest analysis and makes it publicly available for download in the right hand column under “Links”. If you do not read Danish, don’t worry; the report is in English.

Fiberalliancen is a trade association representing companies that own, operate, and use fibre networks in Denmark. It is part of Green Power Denmark.

For the fourth time, following previous reports in 2021, 2022, and 2023, Tefficient has conducted an extensive fibre broadband pricing benchmark across nine European markets: Denmark, Sweden, Norway, Finland, Germany, the Netherlands, Belgium, the UK, and France.

“Germany and the Netherlands have also experienced falling fiber prices, but Denmark has seen the biggest overall price drop over the four years.”

In a press release, Fiberalliancen introduces Tefficient’s latest analysis and makes it publicly available for download at the bottom of the page under ‘Læs hele analysen fra Tefficient‘. If you do not read Danish, don’t worry; the report is in English.

Fiberalliancen is a trade association for companies that own, operate and use fibre networks in Denmark. It is a part of Green Power Denmark.

For the third time (previously done in 2021 and in 2022), Tefficient has performed a comprehensive fibre broadband pricing benchmark covering nine European markets: Denmark, Sweden, Norway, Finland, Germany, the Netherlands, Belgium, the UK and France.

In a press release, Fiberalliancen introduces Tefficient’s analysis and makes it publicly available. Download it from the right ‘Dokumenter’ column. It’s in English.

The release concludes that:

Denmark has some of the lowest consumer prices for both new and existing fibre connections.

Danish consumer prices – both for new and existing connections – have overall fallen from 2022 to 2023. This is only seen in Denmark and the Netherlands.

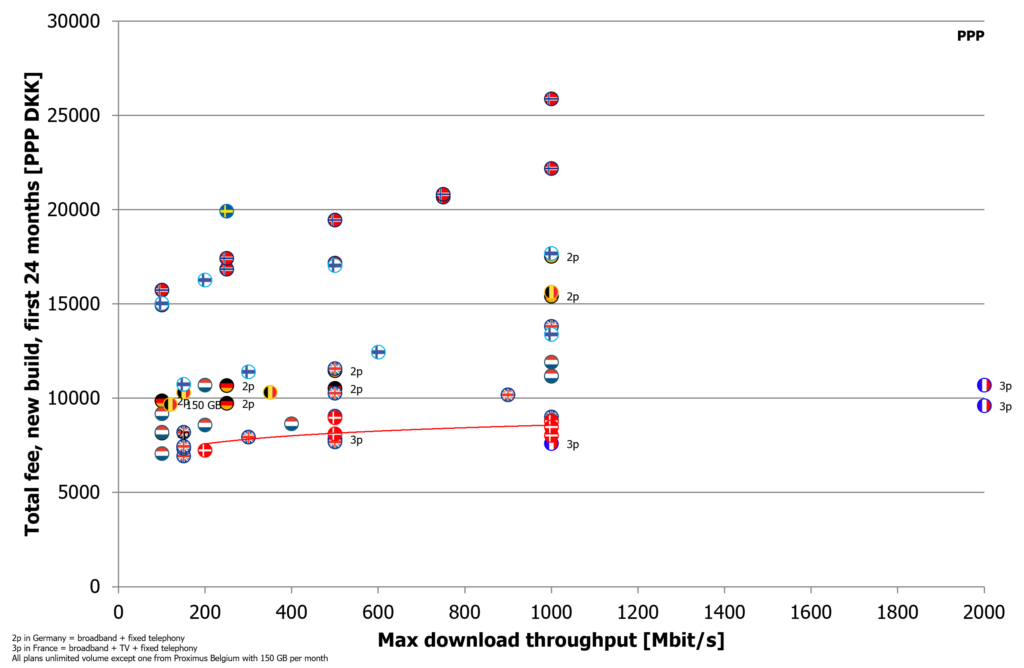

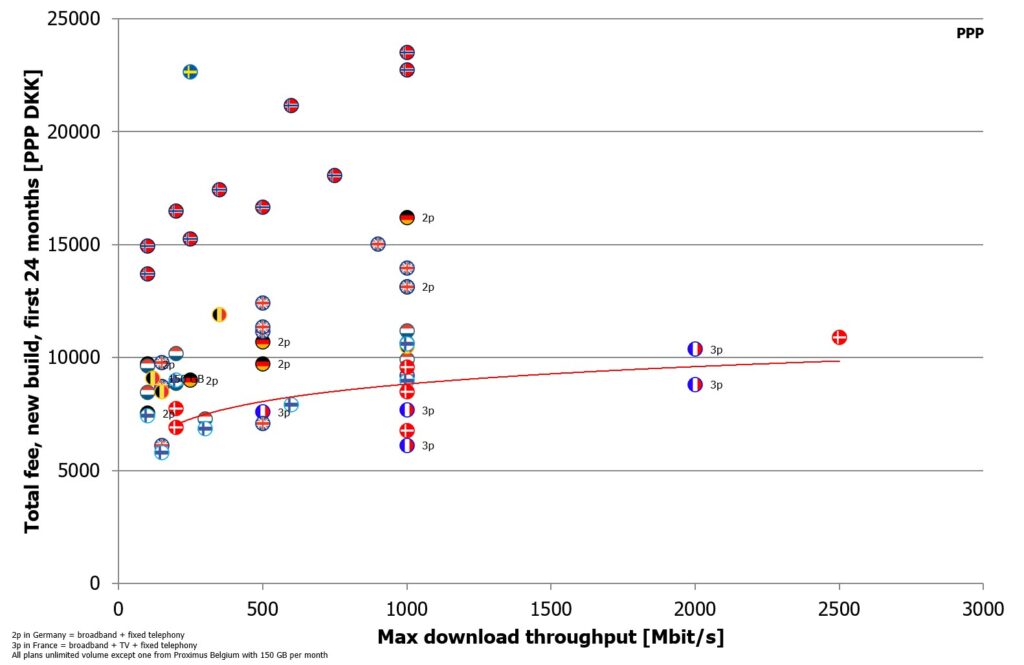

Tefficient’s approach has been thorough and the results are presented in a set of graphs like below.

Example graph from the analysis showing the total 2-year fee for the new build fibre case. The red trend line highlights Denmark’s position.

Fiberalliancen is a trade association for companies that own, operate and use fibre networks in Denmark. It is a part of Green Power Denmark.

For the second time (the first analysis was done in 2021), Tefficient has performed a comprehensive fibre broadband pricing benchmark covering nine European markets: Denmark, Sweden, Norway, Finland (new since 2021), Germany, the Netherlands, Belgium, the UK and France.

As part of a press release, Fiberalliancen makes Tefficient’s analysis publicly available. Download it from the right ‘Links’ column. It’s in English.

The release concludes that:

Denmark has some of the lowest consumer prices for both new and existing fibre connections. Only French consumers generally get a better deal than Danish consumers.

Danish consumer prices – both for new and existing connections – have overall fallen from 2021 to 2022. This is only seen in Denmark and the UK.

According to Ookla, Denmark has the fastest median broadband download speeds among the countries included in the comparison.

Tefficient’s approach has been thorough and the results are presented in a set of graphs like below.

Dansk Energi (Danish Energy) is a business and interest organisation for energy companies in Denmark. These companies spearheaded the rollout of fibre networks in Denmark.

In a press release, Dansk Energi concludes that Denmark has among the lowest prices on fibre broadband in Europe. That conclusion is based on a comprehensive price benchmark performed by Tefficient – a benchmark which Dansk Energi has made public. Open the press release and download the benchmark in the “Dokumenter” area highlighted below.

Which are the equipment sales models in mobile and how have they developed over time? Can best practices be spotted when comparing equipment sales and profitability for a large number of mature market operators globally?

Using facts: What outputs are different equipment sales models such as subsidy, instalment, leasing, rental and BYOD generating – and how is an early upgrade promise affecting?

In this project we identified and documented a few operator best practices across different models in different markets.

How have operators introduced fixed-mobile convergent plans in Europe’s most advanced markets France, Spain, Portugal, Belgium, Switzerland, the Netherlands – and in emerging FMC markets like the UK and Sweden? How – and how quickly – did competition react?

Using facts: What is the take-up of these FMC plans? How have the FMC introductions affected mobile and fixed market share, customer churn, acquisition & retention cost, demand for fibre and TV – and revenue and margin?

How do you avoid making FMC a discount-centric thing? How have the best FMC propositions been put together and how have they been marketed? Is there a way to leverage content and exclusivity?

The past three months have been a testing time for the UK mobile and broadband service providers, as many of them have battled with outages, vandalised phone masts amid lurid 5G conspiracy theories, extreme demand peaks. Store closures have placed added pressure on field, customer service and call centre staff who have been largely working from home. We all know the drill. All of us just want to get on with ‘getting back to normal’, safely past Covid-19, to life as we used to know it. But we don’t know how long it will take, or even if we will have the same breadth of services on the high street as before. Today, 15th of June, the shops are gradually and carefully opening their doors on UK high streets.

Two years ago, telcos were still proudly reporting their progress in utilisation of their own public Wi-Fi hotspots for cost efficient offloading of mobile data. Public Wi-Fi was also positioned as an investment in a better customer experience – especially in public indoor environments. Telcos that were late with 4G – such as in Taiwan and Belgium – could utilise their public Wi-Fi to bridge the transition from 3G to 4G.

It’s here. I’ve been salivating after the latest Apple Watch 3, with all the bells and whistles. Slick, beautiful, cool and I’ll only need a watch to make/receive calls and text, stream music, etc. This should be easy, I’ll just pre-order the GPS & Cellular version. I’m a UK consumer and have a passion for all things mobile & telco, both home and abroad. Therefore, I decided to find out how Apple Watch 3 offers compare in the UK, USA and Australia. Continue reading Apple Watch 3 Cellular, how much data does it eat?→

Measure, compare and improve competitiveness in telecoms

Two years ago, telcos were still proudly reporting their progress in utilisation of their own public Wi-Fi hotspots for cost efficient offloading of mobile data. Public Wi-Fi was also positioned as an investment in a better customer experience – especially in public indoor environments. Telcos that were late with 4G – such as in Taiwan and Belgium – could utilise their public Wi-Fi to bridge the transition from 3G to 4G.

Two years ago, telcos were still proudly reporting their progress in utilisation of their own public Wi-Fi hotspots for cost efficient offloading of mobile data. Public Wi-Fi was also positioned as an investment in a better customer experience – especially in public indoor environments. Telcos that were late with 4G – such as in Taiwan and Belgium – could utilise their public Wi-Fi to bridge the transition from 3G to 4G.