Mobile data usage and revenue for 36 countries

This is tefficient’s 19th public analysis of the development and drivers of mobile data.

Mobile data usage is still growing in all of the countries covered by this analysis. But the growth rates are very different and so are the usage levels. Unlimited moves the needle. Finland tops the charts in usage – but it’s India that leads the growth league.

Data-only is a very important driver of usage. Austria is now the clear world leader in fixed-line substitution.

In Korea, the share of data traffic on 4G has now effectively reached 100% with a 4G penetration of 80%. The country is ready for 5G.

A prerequisite for continued data usage growth is that the total revenue per gigabyte is low. This is not the case in Greece, Canada and Belgium. The total revenue per gigabyte there is roughly 20 times higher than in Finland and more than 35 times higher than in India.

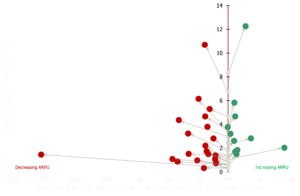

In this analysis we again use the Christmas tree visualisation to identify the countries where the more-for-more initiatives of operators buck the general more-for-less trend.

In this analysis we again use the Christmas tree visualisation to identify the countries where the more-for-more initiatives of operators buck the general more-for-less trend.

Download analysis: Unlimited moves the needle – but it’s when mobile addresses slow fixed internet that something happens Continue reading Unlimited moves the needle – but it’s when mobile addresses slow fixed internet that something happens