Tefficient’s 27th public analysis of the development and drivers of mobile data compares 44 countries from all regions of the world. We say hello to the new additions Chile, New Zealand and Qatar.

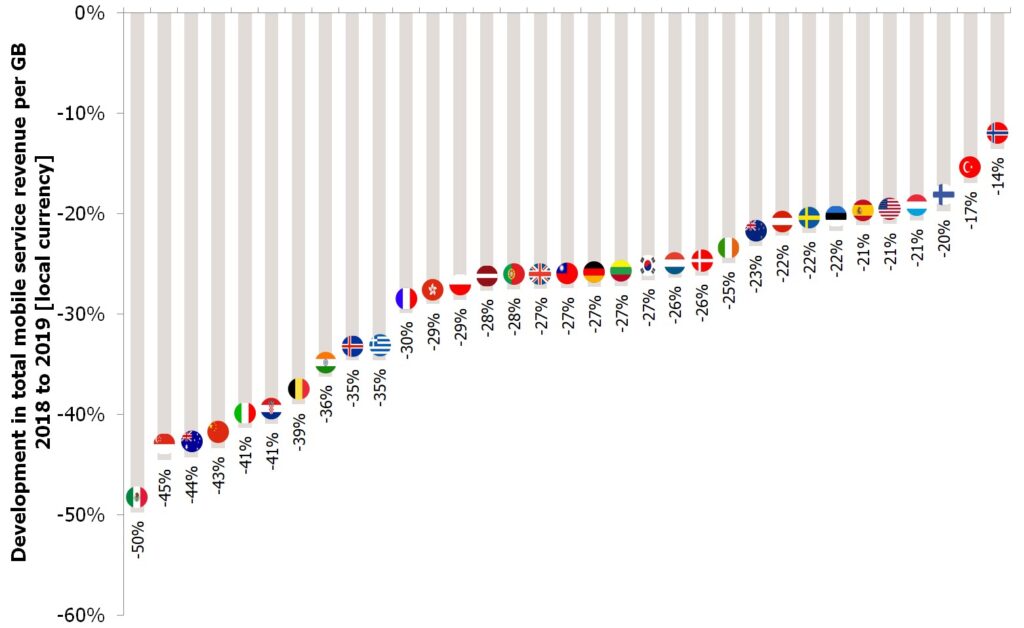

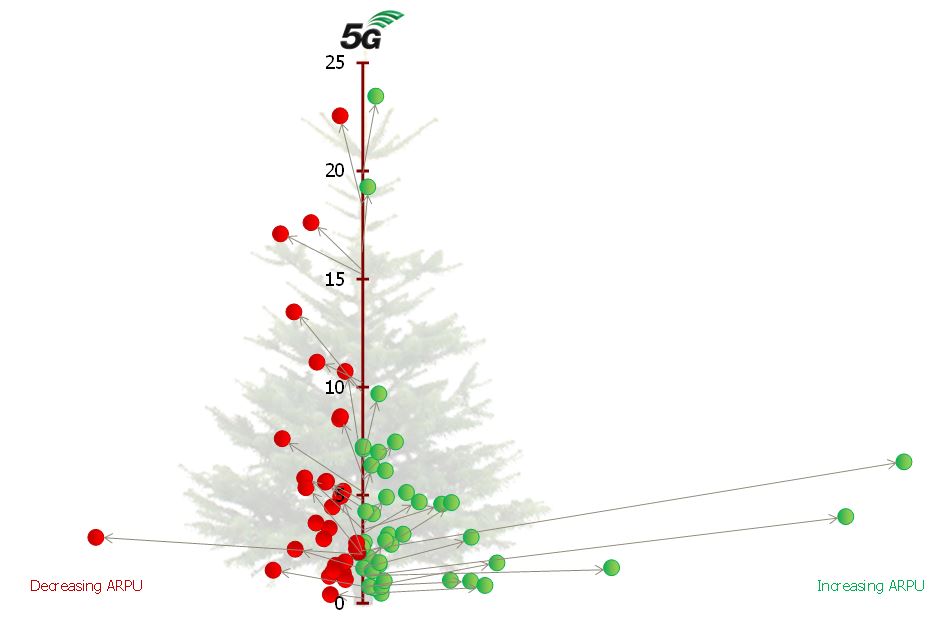

Usage is growing in every single country, but few are able to turn this into ARPU growth. Too few.

Tefficient’s 26th public analysis on the development and drivers of mobile data ranks 105 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in 2019.

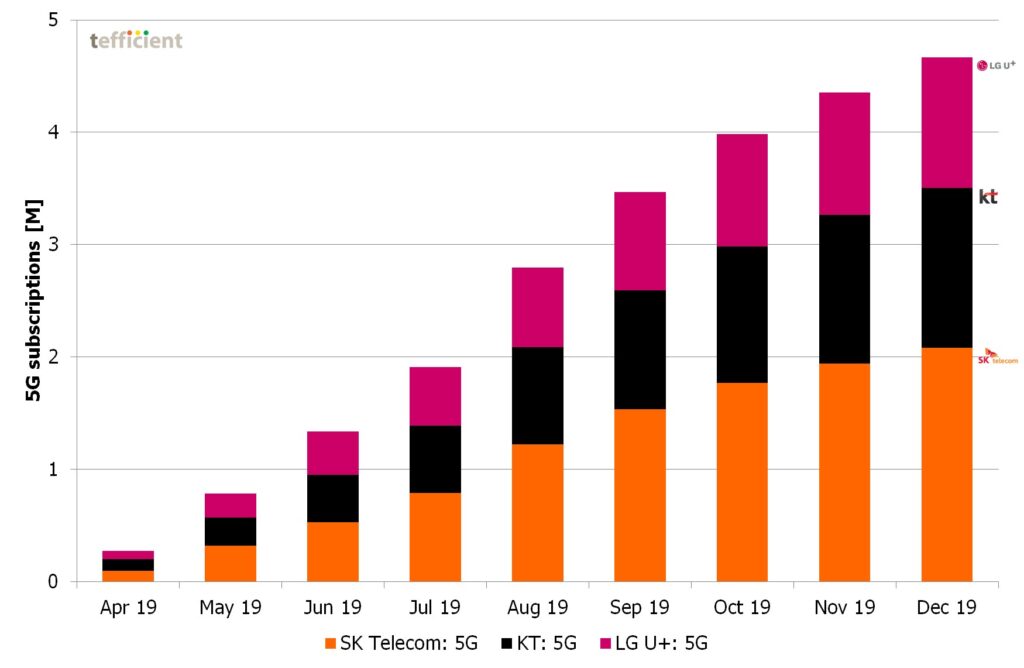

Lobbyists coined the term “the race to 5G”. If there ever was such a race, South Korea won it as unlike other markets there are – read on – many reported numbers to support a leadership claim. With 4.7 million 5G subscriptions by the end of 2019, 7% of Korea’s mobile subscribers used 5G just nine months after launch.

LG U+ site with Huawei 5G gear on the Namsan park above Seoul (photo: Fredrik Jungermann)

The subscriber take-up has been fast, but not linear. In August, September and October, when Samsung launched three new 5G smartphones (Note 10, A90 and Fold) and LG updated its V50 smartphone, 5G sales was exceptionally fast. During November and December no new smartphones were introduced and South Korea missed the expectation of 5 million 5G subscribers by year end 2019.

5G subscriber base per month since launch 5th of April (source data: MSIT)

Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in 1H 2019.

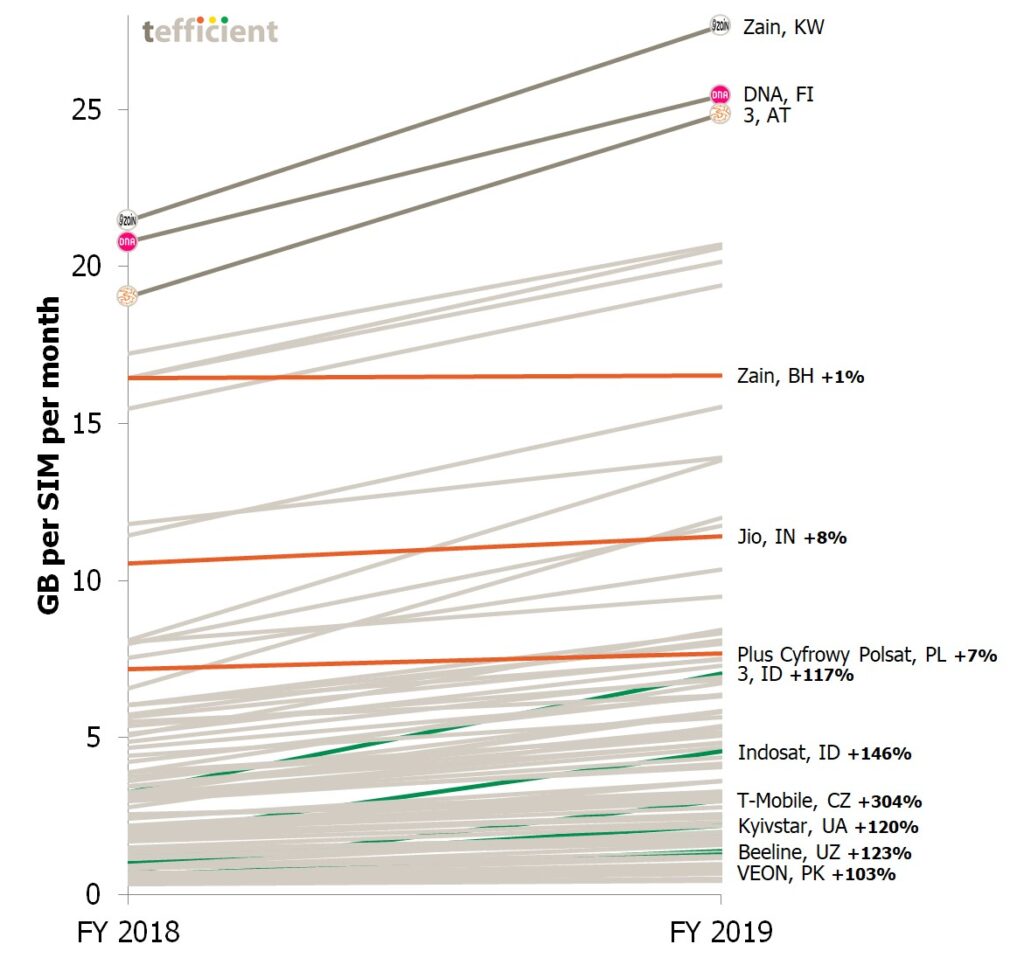

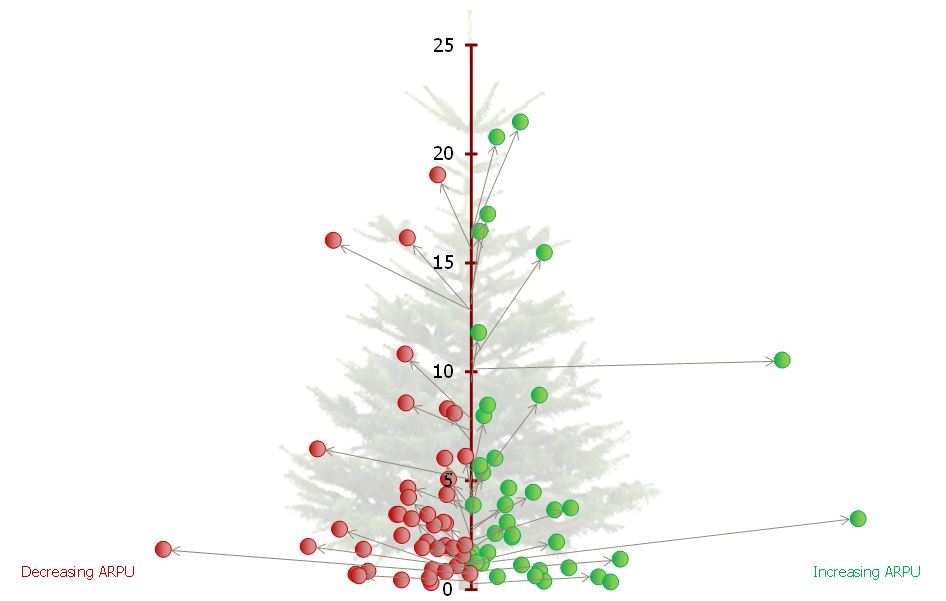

The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth– for the first time a majority is in green. Read our analysis to see who delivered on “more for more” – and who didn’t.

Speaking of which, we take a closer look at the development of one of the unlimited powerhouses –Taiwan. Are people getting tired of mobile data?

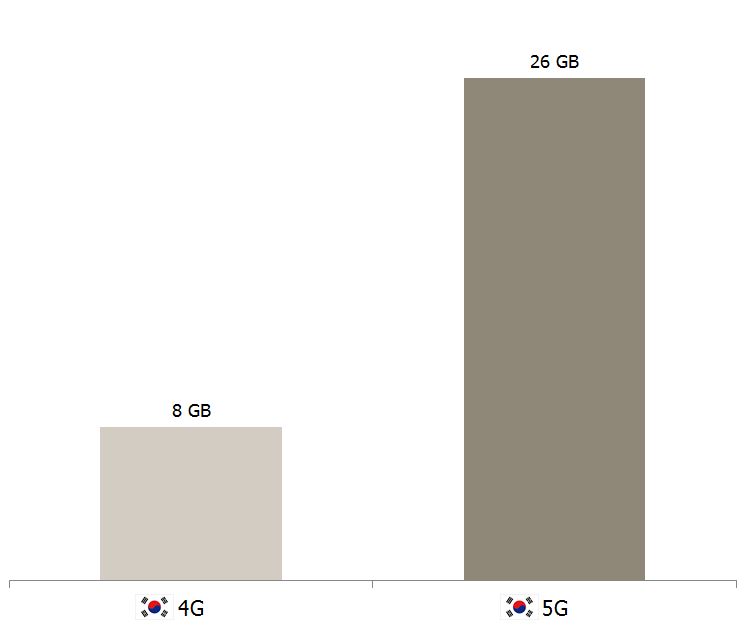

We also provide insight into South Korea– the world’s leading 5G market. Just how much effect did 5G have on the data usage?

Nowhere else in the world will you find as many 5G users as in South Korea. Nowhere else will you find as many 5G base stations up and running. If there ever was a race to 5G, the Korean government and industry won it.

Seeing is believing: After having dug up, read and compiled all reporting and data on Korea’s mobile business there was no other way forward than to seeing it for ourselves and interview people involved in creating Korea’s ‘5G wonder’.

We spent eight busy days (11-18 July) in Seoul to finish a comprehensive 106-page analysis – full of graphs and photos – with recommendations for European operators.

This is tefficient’s 23rd public analysis of the development and drivers of mobile data.

Mobile data usage is still growing in all of the 39 countries covered by this analysis. Two countries stand out – China and India.

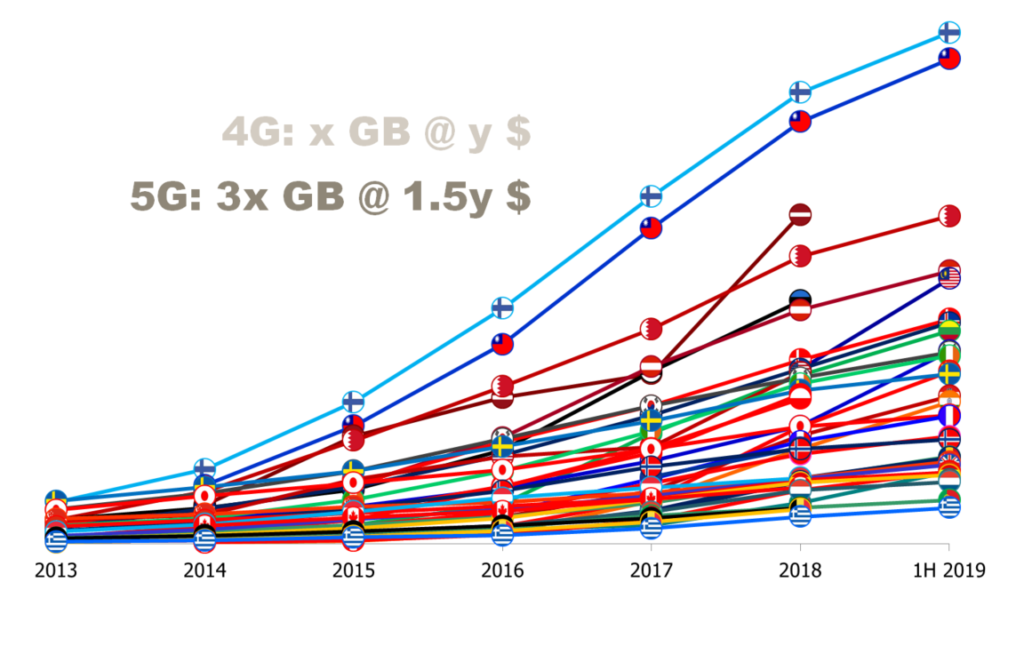

But China and India aren’t yet challenging the usage top – where the two unlimited superpowers, Finland and Taiwan, still reign.

Data-only remains a key driver for overall usage and new figures from Czech Republic, Latvia, Finland and Austria add insight to the extreme usage pattern of fixed wireless access.

Conducting and transcribing 22 interviews with 23 senior executives from telecom operators, handset and chip manufacturers, start-ups, academia and think tanks on the potential of 5G for consumers.

These interviews were, alongside focus groups, used as input to design Ericsson ConsumerLab’s consumer research ultimately covering 22 countries and over 35000 smartphone owners globally.

The interviews form an integral part of the 5G consumer potential report as issued by Ericsson ConsumerLab in May 2019. All interviewees are named in the report. Thank you for your kindness!

When you use a mobile network, your traffic has to co-exist with traffic generated by other users currently connected to the same cell. Your speed experience will depend on how much and what type of traffic those other users generate. It will also depend on how your operator has dimensioned that cell, i.e. how many carriers they have put up. Ultimately that depends on the available spectrum your operator has access to.

When operators want to convince us how great their networks are, they typically talk about download speed, i.e. how many Mbit/s users on their network averagely get when downloading something from the internet. It is being supported by a number of independent network performance specialists – Tutela, Opensignal, Ookla, P3, RootMetrics – issuing country reports naming winning networks.

These reports are actually often multi-faceted with several performance metrics, but that is often too complex to use in marketing, operators think. The simplified marketing message becomes: Speed is good – and we won.

Which operator has the world’s highest data usage?

Which operator carries the most data traffic in the world?

Which operator earns the most – or the least – per GB?

This is tefficient’s 22nd public analysis on the development and drivers of mobile data. We have ranked 90 reporting or reported operators based on average data usage per SIM, total data traffic and revenue per gigabyte in 2018.