In our public industry analysis “Peak data” in sight? we use regulator data to identify Finland as the number 1 country in the world when it comes to mobile data usage, beating all the countries which typically are followed closely – USA, South Korea, Japan.

It’s with great pleasure we note that Finland’s third operator, DNA, has followed in its larger competitor Elisa’s footsteps and reported total mobile data traffic. And it is a blast. Too. Continue reading Finland: The land of three thousand megabytes→

In cooperation with key Comptel experts, writing and editing key parts of Comptel’s book “Operation Nexterday” which was launched at Mobile World Congress 2015.

When the rollout of 4G LTE eventually got up to speed in Western, Central and Southern Europe, it wasn’t long until operators started to report that the rollout was more or less completed, using population coverage as the proof point.

Previous years’ benchmarks showed that network sharing JVs – through focus and new operation models – have established cost and productivity levels which few mobile operators can match within their own network departments. JVs’ network quality is also higher – in spite of higher network load. Continue reading Network sharing JV benchmark 2015→

Bucket plans – with volume caps on the number of minutes, messages and Mbytes – have been offered by mobile operators for years. Even though the composition has varied over time (e.g. through elements made unlimited), the concept is well known to customers.

Monthly caps have become the standard of our industry. Another standard is to reset those caps at the start of a new month. This means that any balance left – minutes, messages, Mbytes – is voided. Or confiscated – to use the word of John Legere, CEO of T-Mobile USA. Continue reading Rollover: The next big thing for customer retention→

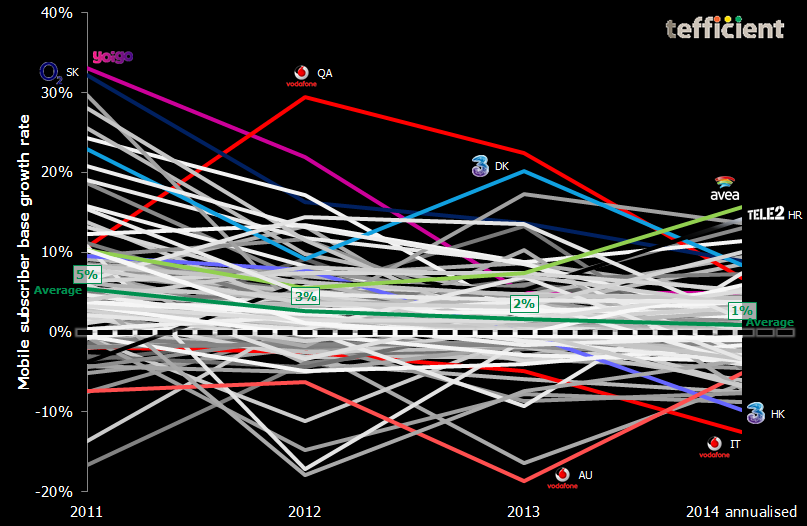

In 2013, tefficient introduced the Nordic operator benchmark to telcos in Sweden, Finland and Norway. The feedback has been strong, leading to repetitions in 2014 and 2015. Denmark was added in 2015.

Unlike other benchmarks, it has a local view sincethe peer group only contains operators from the covered countries – which have been selected based on high comparability. Unlike other benchmarks, it is therefore 100% fact based since no numbers need to be “adjusted” in an attempt to mask that they weren’t comparable in the first place. Continue reading The Alps operator benchmark→

Late November last year, Tele2 launched a major transformation campaign in Sweden under the Tele2.0 banner.

Late November last year, Tele2 launched a major transformation campaign in Sweden under the Tele2.0 banner.

Previous years’ benchmarks

Previous years’ benchmarks Bucket plans – with volume caps on the number of minutes, messages and Mbytes – have been offered by mobile operators for years. Even though the composition has varied over time (e.g. through elements made unlimited), the concept is well known to customers.

Bucket plans – with volume caps on the number of minutes, messages and Mbytes – have been offered by mobile operators for years. Even though the composition has varied over time (e.g. through elements made unlimited), the concept is well known to customers.