Quantitative and qualitative exploration and analysis project starting with a Nonstop Retention® benchmark for a specific country market.

Analysing a wide area of propositions and tactics from several different markets:

Multi-user and multi-device plans

Fixed-mobile convergent plans

Premium value plans and options

Flexible plans and sub-brands

Early upgrade plans for handsets

Loyalty programmes

Identifying best practice with regards to impact on revenue, take-up and customer loyalty. Applying it to the local market competitive context, resulting in a recommendation presented during interactive workshops.

2019 will be a year with significant uncertainty for many operators. Will we get that frequency license? Will the merger in our market be approved? Will we be able to launch 5G? Will competing fixed wireless propositions steal our broadband customers and erode prices? Will our competitors begin producing original content?

Good then that there are questions that can be answered here and now. These are the ones we know many of you are busy with:

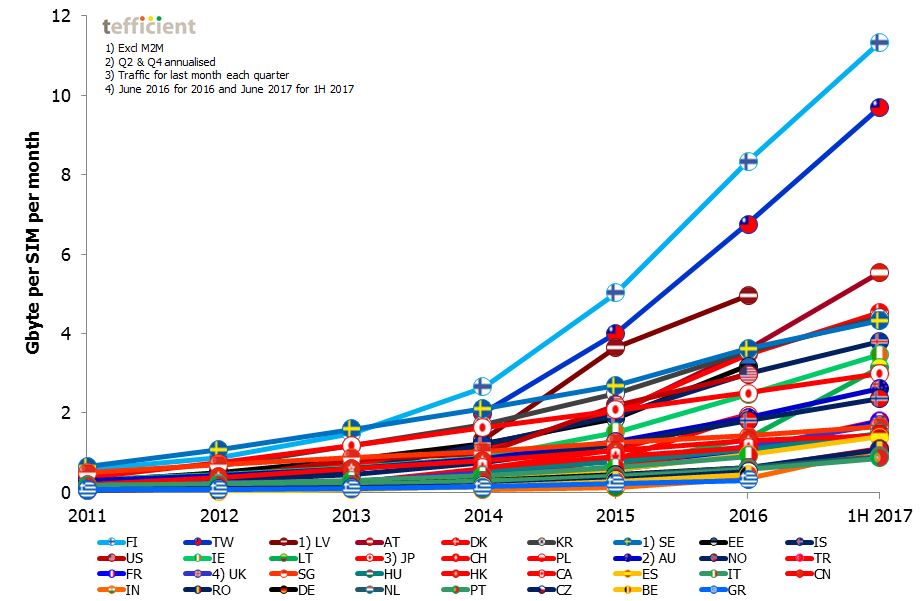

The Finnish-Estonian operator Elisa just published its 4Q 2017 results. And it was a new record in revenue and profitability.

How is that even possible? Readers of our public analysis of mobile data usage know that Finland is the mobile data usage powerhouse of the world – and that Elisa is no exception.

But Elisa doesn’t charge per gigabyte – so where is the revenue growth coming from? How can the company make more profit when it needs to handle all that traffic? This blog reveals their secret. Continue reading The secret behind Elisa’s financials→

Building and interactively presenting a comprehensive before/after analysis of international mobile propositions and their effects on customer intake, customer loyalty, revenue growth and data usage.

Emphasis on how to maximise the effect of e.g. unlimited data, zero-rated services, group & family plans and time-based offers in post- and prepaid propositions. Mapping the propositions to customers segments with a reward-for-wanted-behaviour logic balancing between general availability and segment exclusivity. Continue reading Analysis and recommendations on mobile proposition refresh→

Nonstop Retention® benchmark: Calculating and comparing the Nonstop Retention Index for mobile brands (MNOs, sub-brands and main MVNOs) in one specific major European market. Identifying best practice and showing current trends. Recommending propositions and actions to improve customer loyalty per brand.

There has been a lot of talk – and increasing irritation – about pigeonholing, especially the younger (18 to 24 year olds), consumers to a tightly defined segment. Generalisations can be dangerous, especially for those companies that still primarily make the effort of engaging with their customers when they are buying something and spend most of their marketing dollars in digital and other forms of advertising.

But loyalty comes from understanding what makes your customers tick – and this knowledge can only be derived from active conversations with the community, regardless if they are Millennials or those labelled Generation X. Nevertheless, it is useful to understand broadly how the different consumer segments are behaving and what motivates them. But we’ll come back to this in a bit. Continue reading Instant messaging and ad blocking – the new normal?→

Wi-Fi Calling is relatively new – and then, not really. In 2014, Apple’s launch of iOS 8 with embedded Wi-Fi Calling marked a milestone for voice calling with mobile devices, despite several years of Voice over Wi-Fi services in various guises preceding iOS 8.

Aptilo Networks – a leading provider of carrier-class systems to manage data services with advanced functions for authentication, policy control and charging – has released a White Paper titled “Seamless Next Generation Wi-Fi Calling”, which is written by Allan Greve of tefficient.