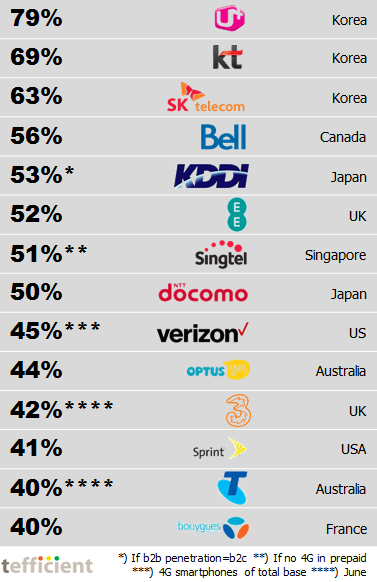

Why should an operator complement their customers’ experience of mobile data with Wi-Fi? To improve customer loyalty?

Wi-Fi is a positively loaded term for many users – which speaks for using it as a retention tool. But are there operators that successfully reduce churn – without using more on customer retention – by having Wi-Fi included in their mobile propositions? Continue reading Wi-Fi – the last piece of the customer retention puzzle?→

Some of you might feel that tefficient tends to overstate the importance of Netflix for telecoms.

In most European markets where Netflix operates, it has as many subscribers as all other paid video streaming services together. In some of these countries Netflix has more households subscribing to its service than there are IPTV households in the country. Continue reading Chart: Why Netflix’ expansion is good news for mobile carriers→

Prediction 1 – mobile data usage of 10 GB per month

At least one mobile operator will reach an average mobile data consumption of 10 GB per any SIM and month in 2016

We think this operator is Finnish and that Elisa and DNA both have a chance to snatch this world first. Finland is already having the highest mobile data usage in the world and the current usage level will not even have to double as in 2015 to reach 10 GB in 2016. Continue reading Nine predictions for 2016 – which can be measured→

We all know that a significant share of mobile operator revenue is equipment, not service, related. Even though equipment subsidisation and lock-in contracts rapidly become less popular, the reality is that if it wasn’t for subsidisation, reported equipment revenues would be even higher.

A loyal long-term customer is considered a key asset by companies in most industries. It’s conventional wisdom that it costs more to recruit a new customer than to keep an existing one. Consequently, existing customers should be treated better than new customers. Continue reading The anti-guide: Six ways to make sure your customer churns→

Measure, compare and improve competitiveness in telecoms