![]() The mobile network performance crowdsourcer OpenSignal published its latest State of LTE report today. This time it’s based on data samples from 357924 mobile users who have OpenSignal’s app on their Android devices. The network performance data isn’t just gathered when users actively do a measurement; it’s collected all the time and the number of samples are therefore hundreds of millions. The stats thus better represent the normal behavioural patterns of users when it comes to time and location. The data is collected during the fourth quarter of 2015. Continue reading Crowdsourced 4G experience: Benchmarking Nordic operators

The mobile network performance crowdsourcer OpenSignal published its latest State of LTE report today. This time it’s based on data samples from 357924 mobile users who have OpenSignal’s app on their Android devices. The network performance data isn’t just gathered when users actively do a measurement; it’s collected all the time and the number of samples are therefore hundreds of millions. The stats thus better represent the normal behavioural patterns of users when it comes to time and location. The data is collected during the fourth quarter of 2015. Continue reading Crowdsourced 4G experience: Benchmarking Nordic operators

Category Archives: Blog

Denmark – 5 months after the non-merger

On 11 September 2015, Telia and Telenor announced that they had been unsuccessful in reaching an agreement with the EU Commission for Competition concerning a merger of the two operators in Denmark, which was announced 9 months earlier on 3 December 2014.

On 11 September 2015, Telia and Telenor announced that they had been unsuccessful in reaching an agreement with the EU Commission for Competition concerning a merger of the two operators in Denmark, which was announced 9 months earlier on 3 December 2014.

The concerns from EU presumably centered around a weakened competitive market in Denmark if Telia and Telenor were allowed to merge. As a background, the two companies had already merged their networks into a common JV called TT-Netværket.

So what has happened since – it has now been 5 months or so since the news about the failed merger? So you know what to expect in e.g. the UK and in Italy if the mobile mergers won’t be approved there. Continue reading Denmark – 5 months after the non-merger

34 petabytes of zero-rated video streamed since launch of Binge On

Mid November last year, T-Mobile USA launched its 10th uncarrier initiative, Binge On. It has been the most controversial uncarrier launch so far.

Why? Binge On zero-rates commercial video services – so that T-Mobile customers can watch as much as they like without emptying their data bucket. The trade-off? Video streams are slowed down to about 1.5 Mbit/s which means that image quality suffers – which is visible, but perhaps not on smaller screens like smartphones and tablets. Continue reading 34 petabytes of zero-rated video streamed since launch of Binge On

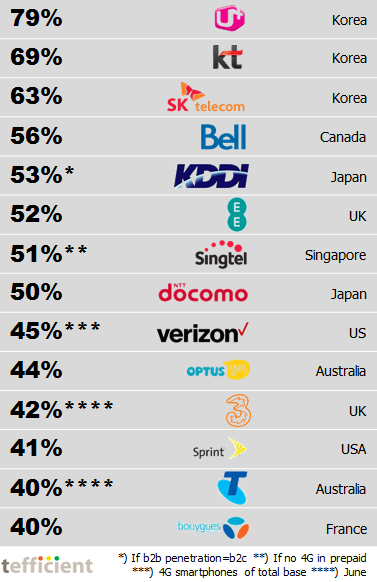

4G penetration: Global top list

4G is rapidly becoming a mature market normality.

4G is rapidly becoming a mature market normality.

Our top list to the right shows the reporting operators of the world with more than 40% 4G adoption in their retail bases as of September 2015.

The three Korean operators LG Uplus, KT and SK Telecom lead. No news; this has been the case since the first days of 4G. Continue reading 4G penetration: Global top list

Chart: Why Netflix’ expansion is good news for mobile carriers

Some of you might feel that tefficient tends to overstate the importance of Netflix for telecoms.

Some of you might feel that tefficient tends to overstate the importance of Netflix for telecoms.

In most European markets where Netflix operates, it has as many subscribers as all other paid video streaming services together. In some of these countries Netflix has more households subscribing to its service than there are IPTV households in the country. Continue reading Chart: Why Netflix’ expansion is good news for mobile carriers

Nine predictions for 2016 – which can be measured

Prediction 1 – mobile data usage of 10 GB per month

At least one mobile operator will reach an average mobile data consumption of 10 GB per any SIM and month in 2016

![]() We think this operator is Finnish and that Elisa and DNA both have a chance to snatch this world first. Finland is already having the highest mobile data usage in the world and the current usage level will not even have to double as in 2015 to reach 10 GB in 2016. Continue reading Nine predictions for 2016 – which can be measured

We think this operator is Finnish and that Elisa and DNA both have a chance to snatch this world first. Finland is already having the highest mobile data usage in the world and the current usage level will not even have to double as in 2015 to reach 10 GB in 2016. Continue reading Nine predictions for 2016 – which can be measured

Plan B: Avoid the merger-to-no-merger journey

The shock waves reverberate in the European telecoms industry ever since Telenor and TeliaSonera in September deemed it pointless to continue negotiations with the European Commission to win support for a mobile merger between Telenor and Telia in Denmark. Continue reading Plan B: Avoid the merger-to-no-merger journey

The shock waves reverberate in the European telecoms industry ever since Telenor and TeliaSonera in September deemed it pointless to continue negotiations with the European Commission to win support for a mobile merger between Telenor and Telia in Denmark. Continue reading Plan B: Avoid the merger-to-no-merger journey

Too much equipment and too little service revenue? Or vice versa? Check here.

We all know that a significant share of mobile operator revenue is equipment, not service, related. Even though equipment subsidisation and lock-in contracts rapidly become less popular, the reality is that if it wasn’t for subsidisation, reported equipment revenues would be even higher.

Our comparison of 80 reporting operators globally – all in mature markets – shows that the equipment revenue to total mobile revenue ratio can be as low as 5% and as high as 77% (click graph to enlarge): Continue reading Too much equipment and too little service revenue? Or vice versa? Check here.

How carriers are using Wi-Fi across the world

One year elapsed since the previous Wi-Fi conference in Europe and carriers’ deployment of Wi-Fi has never been faster.

The graph is fetched from our presentation in the Wi-Fi NOW conference in Amsterdam yesterday and shows the number of hotspots in green and homespots in amber for 45 reporting carriers globally (click to enlarge): Continue reading How carriers are using Wi-Fi across the world

Save, borrow, be rewarded with, give away Gbytes. The new currency?

Back from two mind-blowing days in Helsinki, we sense that nobody – organisers, speakers, participants – on beforehand actually had a notion of just how great the Nexterday North “anti-seminar” would turn out to be. Continue reading Save, borrow, be rewarded with, give away Gbytes. The new currency?