Since T-Mobile’s plans for Data Stash were made public in December last year, we have looked forward to T-Mobile’s reporting of Q1 results – since we hoped to see the first indications of if rollover data actually helps customer retention. Continue reading T-Mobile’s churn lowest ever – following introduction of Data Stash

All posts by Fredrik Jungermann

Liberty Global buys a mobile operator. What does it mean for Europe?

![]() Liberty Global has through a number of major acquisitions – Virgin Media in the UK and Ziggo in the Netherlands being the latest – expanded its European cable footprint. Continue reading Liberty Global buys a mobile operator. What does it mean for Europe?

Liberty Global has through a number of major acquisitions – Virgin Media in the UK and Ziggo in the Netherlands being the latest – expanded its European cable footprint. Continue reading Liberty Global buys a mobile operator. What does it mean for Europe?

4G population coverage: Marketing vs. reality

We have previously addressed the challenge to translate high population coverage into customer experience in 4G LTE.

The graph below shows the difference (in percentage points) between operator reported population coverage for the end of 2014 and the actual time 4G customers could indeed be on 4G – according to OpenSignal’s crowdsourced data for Q1 2015 (gathered November 2014-January 2015). Continue reading 4G population coverage: Marketing vs. reality

BT Mobile: Surprisingly disruptive

After 14 years, BT is back into consumer mobile. The long-rumoured launch of BT Mobile happened today. Continue reading BT Mobile: Surprisingly disruptive

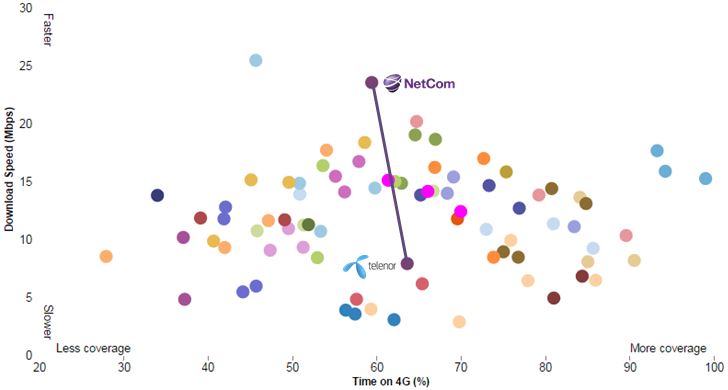

If you sell Mbytes, why slow your customers down?

We’ve been awaiting Telenor’s official comments to OpenSignal’s new crowdsourced 4G coverage and speed test, but since Telenor hasn’t yet commented it we try to interpret the Norwegian results ourselves.

Continue reading If you sell Mbytes, why slow your customers down?

Tele2: From industry’s black sheep to customer’s best friend?

Late November last year, Tele2 launched a major transformation campaign in Sweden under the Tele2.0 banner.

Late November last year, Tele2 launched a major transformation campaign in Sweden under the Tele2.0 banner.

The message? Tele2 had questioned all industry practices and concluded that many of them were outright stupid. And consequently stopped or changed them. Continue reading Tele2: From industry’s black sheep to customer’s best friend?

Finland: The land of three thousand megabytes

In our public industry analysis “Peak data” in sight? we use regulator data to identify Finland as the number 1 country in the world when it comes to mobile data usage, beating all the countries which typically are followed closely – USA, South Korea, Japan.

It’s with great pleasure we note that Finland’s third operator, DNA, has followed in its larger competitor Elisa’s footsteps and reported total mobile data traffic. And it is a blast. Too. Continue reading Finland: The land of three thousand megabytes

Contributing to Comptel’s book “Operation Nexterday”

Analysis & Go-to-market 2015

![]() In cooperation with key Comptel experts, writing and editing key parts of Comptel’s book “Operation Nexterday” which was launched at Mobile World Congress 2015.

In cooperation with key Comptel experts, writing and editing key parts of Comptel’s book “Operation Nexterday” which was launched at Mobile World Congress 2015.

Why 100% population coverage on 4G doesn’t imply a great customer experience

Once you pop, you can’t stop?

When the rollout of 4G LTE eventually got up to speed in Western, Central and Southern Europe, it wasn’t long until operators started to report that the rollout was more or less completed, using population coverage as the proof point.

Let’s look at the stats from 19 operators who reported 4G population coverage both for December 2013 and 2014: Continue reading Why 100% population coverage on 4G doesn’t imply a great customer experience

Niel buys Orange Switzerland: So will Swiss headcount follow French?

Orange Switzerland (which since 2012 isn’t owned by Orange Group) is just about to be sold to Xavier Niel’s private holding company. What makes it interesting is that Niel is the person behind Iliad, the company who operates under the Free brand in France. Continue reading Niel buys Orange Switzerland: So will Swiss headcount follow French?