Providing a global solutions provider with a country-per-country OPEX and CAPEX breakdown comparison between all major operators in seven large countries – based on combining operator reported figures, regulatory data, market data and operators’ communicated plans & targets with tefficient‘s understanding of what is industry typical given market position and strategy.

Not many operators in Europe report the number of 4G subscribers, but in this graph we have collected those who have. We recalculated end of March 2015 figures into penetration figures of the total SIM base. Continue reading 4G penetration top 21 of Europe→

The graph below shows the difference (in percentage points) between operator reported population coverage for the end of 2014 and the actual time 4G customers could indeed be on 4G – according to OpenSignal’s crowdsourced data for Q1 2015 (gathered November 2014-January 2015). Continue reading 4G population coverage: Marketing vs. reality→

Consumers often think of carriers being somewhat stuffy and dusty, being slow to give customers flexibility and big at small print. But there are great exceptions to the rule with T-Mobile in the US, Free in France and Tele2 in Sweden, and we believe the next two years will see some further fun, entertaining and disruptive carrier offerings on the market. Continue reading Freedom to stay – The power of 40000 Tweets→

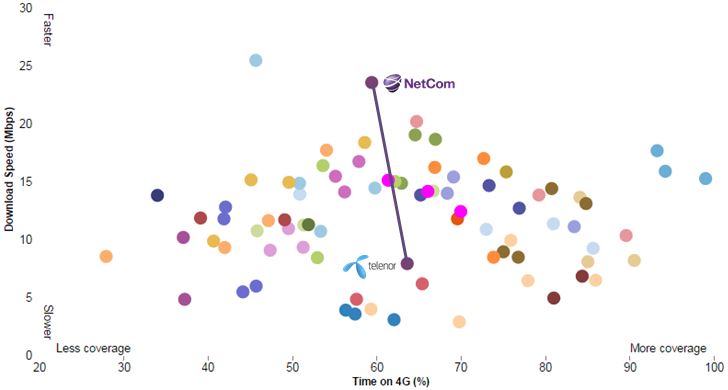

We’ve been awaiting Telenor’s official comments to OpenSignal’s new crowdsourced 4G coverage and speed test, but since Telenor hasn’t yet commented it we try to interpret the Norwegian results ourselves.

In our public industry analysis “Peak data” in sight? we use regulator data to identify Finland as the number 1 country in the world when it comes to mobile data usage, beating all the countries which typically are followed closely – USA, South Korea, Japan.

It’s with great pleasure we note that Finland’s third operator, DNA, has followed in its larger competitor Elisa’s footsteps and reported total mobile data traffic. And it is a blast. Too. Continue reading Finland: The land of three thousand megabytes→

Measure, compare and improve competitiveness in telecoms