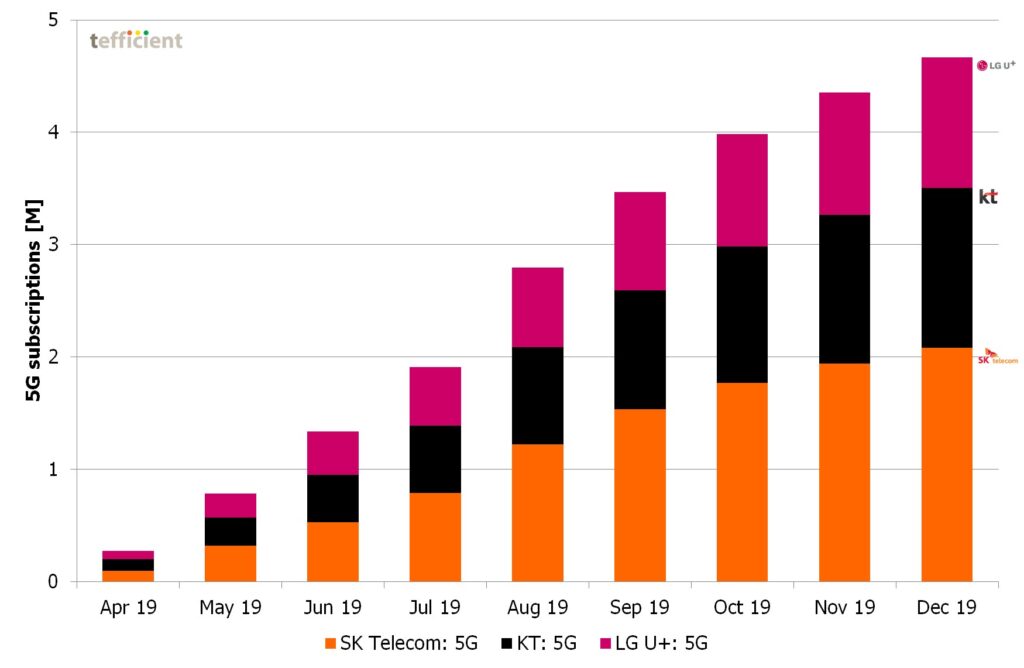

Lobbyists coined the term “the race to 5G”. If there ever was such a race, South Korea won it as unlike other markets there are – read on – many reported numbers to support a leadership claim. With 4.7 million 5G subscriptions by the end of 2019, 7% of Korea’s mobile subscribers used 5G just nine months after launch.

LG U+ site with Huawei 5G gear on the Namsan park above Seoul (photo: Fredrik Jungermann)

The subscriber take-up has been fast, but not linear. In August, September and October, when Samsung launched three new 5G smartphones (Note 10, A90 and Fold) and LG updated its V50 smartphone, 5G sales was exceptionally fast. During November and December no new smartphones were introduced and South Korea missed the expectation of 5 million 5G subscribers by year end 2019.

5G subscriber base per month since launch 5th of April (source data: MSIT)

Without subscription growth it’s difficult for mature market operators to report service revenue growth.

Some operators – anxious to still show growth – have thus begun to regularly highlight their fixed-mobile convergence base in quarterly results presentations. It’s most often a smoke screen. Here are seven examples – of which six aren’t growth stories.

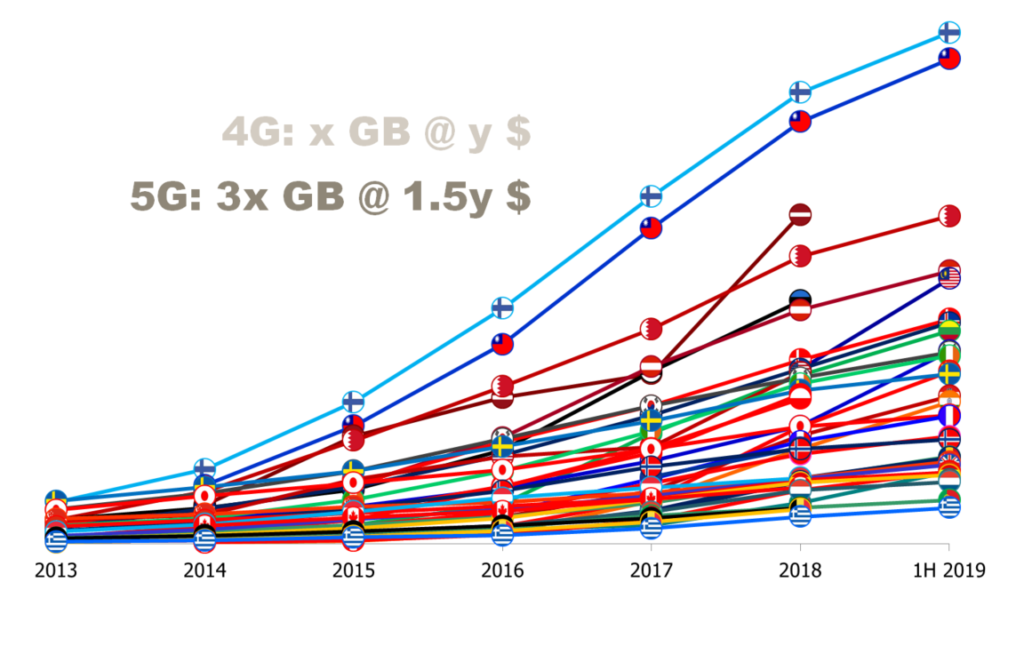

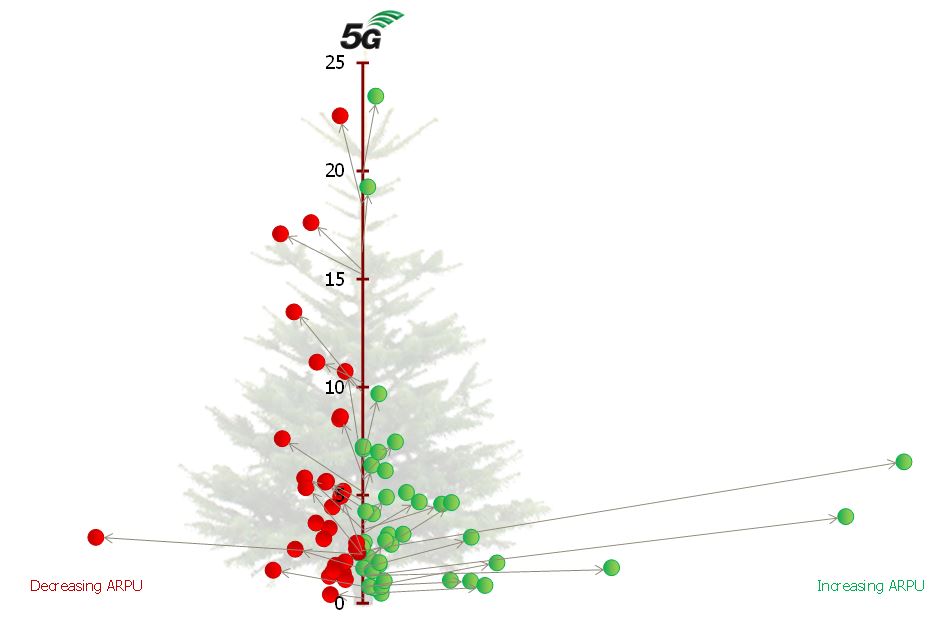

Tefficient’s 24th public analysis on the development and drivers of mobile data ranks 115 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in 1H 2019.

The data usage per SIM grew for all; everybody climbed our Christmas tree. More than half of the operators could turn that data usage growth into ARPU growth– for the first time a majority is in green. Read our analysis to see who delivered on “more for more” – and who didn’t.

Speaking of which, we take a closer look at the development of one of the unlimited powerhouses –Taiwan. Are people getting tired of mobile data?

We also provide insight into South Korea– the world’s leading 5G market. Just how much effect did 5G have on the data usage?

Nowhere else in the world will you find as many 5G users as in South Korea. Nowhere else will you find as many 5G base stations up and running. If there ever was a race to 5G, the Korean government and industry won it.

Seeing is believing: After having dug up, read and compiled all reporting and data on Korea’s mobile business there was no other way forward than to seeing it for ourselves and interview people involved in creating Korea’s ‘5G wonder’.

We spent eight busy days (11-18 July) in Seoul to finish a comprehensive 106-page analysis – full of graphs and photos – with recommendations for European operators.

This is our fourth comparison of the mobile network experiences in the Nordics based on performance data from Opensignal. There are more details and background is the previous (one–two–three) blogs.

This time the data is gathered from March to May 2019. The data has not been published by OpenSignal but has been shared with us through Opensignal’s analyst program.

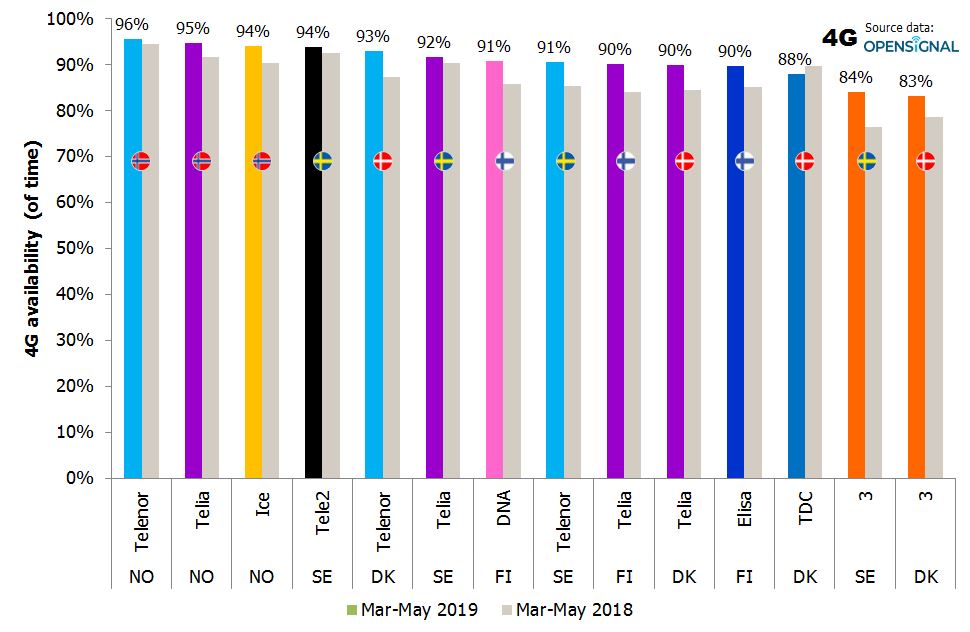

4G availability

The graph below ranks the fourteen operators in Norway, Sweden, Denmark and Finland after how large proportion of time 4G capable devices have been connected to 4G. Opensignal calls this 4G availability.

When you use a mobile network, your traffic has to co-exist with traffic generated by other users currently connected to the same cell. Your speed experience will depend on how much and what type of traffic those other users generate. It will also depend on how your operator has dimensioned that cell, i.e. how many carriers they have put up. Ultimately that depends on the available spectrum your operator has access to.

When operators want to convince us how great their networks are, they typically talk about download speed, i.e. how many Mbit/s users on their network averagely get when downloading something from the internet. It is being supported by a number of independent network performance specialists – Tutela, Opensignal, Ookla, P3, RootMetrics – issuing country reports naming winning networks.

These reports are actually often multi-faceted with several performance metrics, but that is often too complex to use in marketing, operators think. The simplified marketing message becomes: Speed is good – and we won.

Few people think through their New Year resolutions in advance. That’s perhaps the reason to why they typically don’t last longer than the first week of February.

Making industry predictions for an upcoming year is of course something totally different. It’s hard work and no champagne. Fine analysts use twelve months to gather and refine the best ideas and to substantiate these with tons of data points – just to give it all for free to the world. It’s charity at its best.

When we once again dive into OpenSignal‘s crowdsourced stats from the Nordics it is to see if something changed with regards to the network experiences of mobile customers in the region.

This is the third time we address this. The first blog – with data from the autumn of 2017 – contains all the background and reasoning. It was followed up by another blog based on data from the winter of 2017/18.

This time the data is gathered from March to May 2018 and covers about 490 million readings from about 15000 unique devices. The data has not been published by OpenSignal but has been shared with us through OpenSignal’s analyst program.

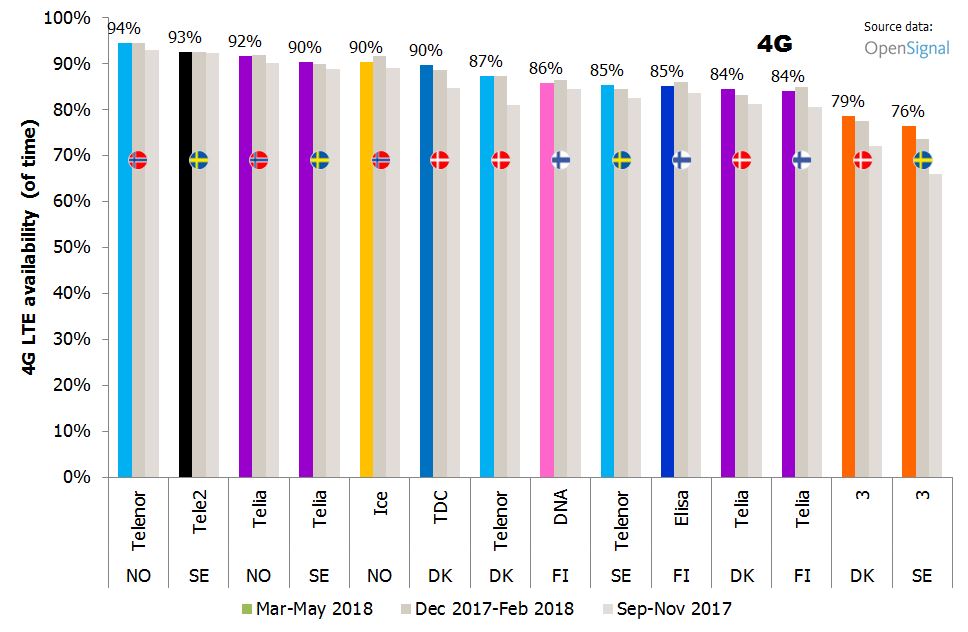

4G availability

The graph below ranks the fourteen operators in Norway, Sweden, Denmark and Finland after how large proportion of time 4G capable devices have been connected to 4G. OpenSignal calls this 4G availability.

2019 will be a year with significant uncertainty for many operators. Will we get that frequency license? Will the merger in our market be approved? Will we be able to launch 5G? Will competing fixed wireless propositions steal our broadband customers and erode prices? Will our competitors begin producing original content?

Good then that there are questions that can be answered here and now. These are the ones we know many of you are busy with: