New! Mobile data usage and revenue for 115 operators

Tefficient’s 20th public analysis on the development and drivers of mobile data follows on our country-focused analysis published in July.

Tefficient’s 20th public analysis on the development and drivers of mobile data follows on our country-focused analysis published in July.

In our latest analysis we have ranked 115 operators based on:

- Average data usage per SIM

- Total data traffic

- Revenue per gigabyte

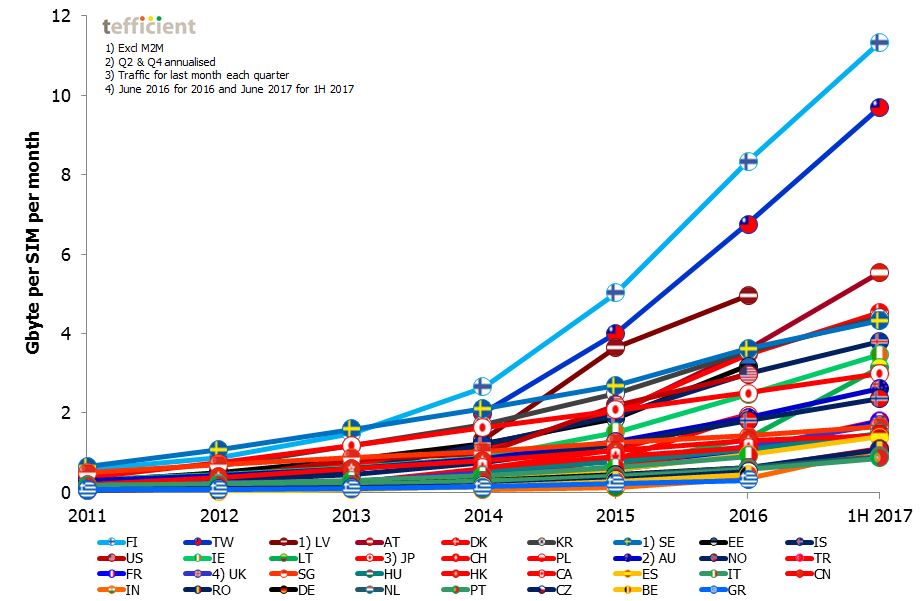

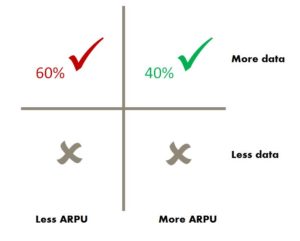

The data usage per SIM grew for all operators. And it grew quickly. But what happened to ARPU? Could operators monetise the data usage growth?

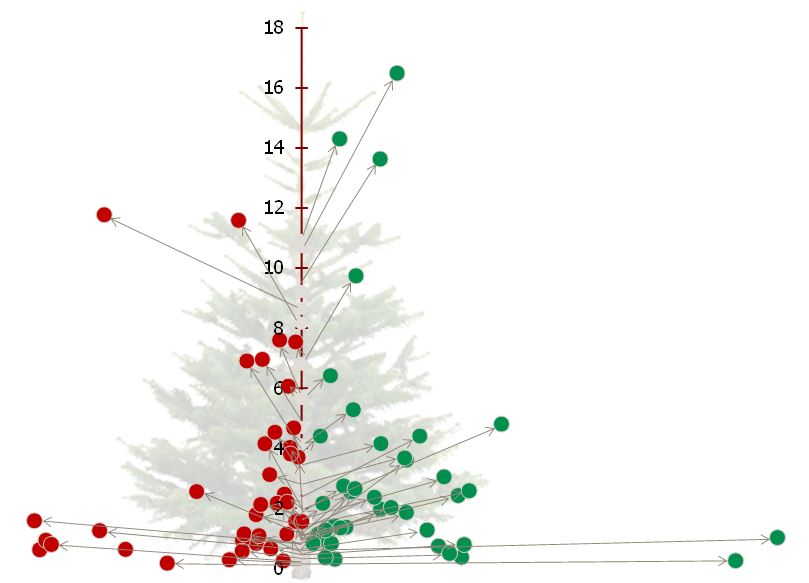

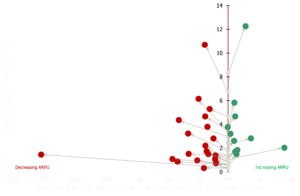

Our Christmas tree graph visualises those that delivered on “more for more” – and those that are just followed the “more for less” stream.

Download analysis: More data? Always. For more? It happens. Continue reading More data? Always. For more? It happens.

In this analysis we again use the Christmas tree visualisation to identify the countries where the more-for-more initiatives of operators buck the general more-for-less trend.

In this analysis we again use the Christmas tree visualisation to identify the countries where the more-for-more initiatives of operators buck the general more-for-less trend.