Wondered why American carriers spent so much effort and marketing dollars claiming and defending “the best mobile network” position lately?

It started with Verizon‘s balls commercial:

Wondered why American carriers spent so much effort and marketing dollars claiming and defending “the best mobile network” position lately?

It started with Verizon‘s balls commercial:

Even though there are some high-profiled exceptions (Verizon, most of Vodafone Group and Free to mention three), few telcos are today trusting its ability to attract all customer segments – across consumer and business markets – with one single brand.

Having one or several sub-brands has become the norm of a modern telco. In some cases, e.g. with KPN’s Telfort and TDC’s Telmore, sub-brands have been added as a result of acquisitions (often of a successful disruptive brand). In other cases, e.g. Orange’s Sosh or 3 Denmark’s Oister, telecos have themselves created the sub-brand – often with the intention to isolate the main brand from a new price fighter brand. Continue reading When your sub-brand takes over

At KPN’s Capital Market Day, arranged at the Rijksmuseum today, several executives of KPN stated:

At KPN’s Capital Market Day, arranged at the Rijksmuseum today, several executives of KPN stated:

“Households are at the center of our strategy”

And it’s not so difficult to understand why. Continue reading Is KPN dedicating itself to a saturating market?

![]() In Europe, we woke up with the news that Vodafone and Liberty Global had agreed to merge their Dutch operations Vodafone and Ziggo.

In Europe, we woke up with the news that Vodafone and Liberty Global had agreed to merge their Dutch operations Vodafone and Ziggo.

Less than two weeks ago, Telenet, Liberty Global’s affiliate in Belgium, got a green light from the European Commission to buy the mobile operator BASE from KPN. So already before today, Liberty took a major step in the mobile direction.

Read the original commentary on what this means for Europe

Vodafone, on its part, has demonstrated an appetite for cablecos: In 2013, it began acquiring Kabel Deutschland and in 2014 it acquired Ono in Spain. Continue reading Ziggo/Vodafone: Decouple broadband, start to invest – to stop customer outflow

Why should an operator complement their customers’ experience of mobile data with Wi-Fi? To improve customer loyalty?

Wi-Fi is a positively loaded term for many users – which speaks for using it as a retention tool. But are there operators that successfully reduce churn – without using more on customer retention – by having Wi-Fi included in their mobile propositions? Continue reading Wi-Fi – the last piece of the customer retention puzzle?

How much mobile services do you get for 20 EUR?

For 25? 30? 35? 40 EUR?

We have compared the service prices of all mobile operator brands in eleven countries: Germany, the UK, France, the Netherlands, Belgium, Sweden, Austria, Switzerland, Denmark, Finland and Norway.

And Europe is divided. Continue reading What buys you a load of data in Finland, France & Denmark, buys you nothing in Belgium & Switzerland

Decoupled, non-binding, unsubsidised: A game changer?

Our analysis shows that mature market mobile operators on average use 15-20% of service revenue on subscriber acquisition and subscriber retention cost (SAC/SRC). In most cases without growing.

Consequently, we examine the success of the operators who – in order to reduce SAC/SRC and improve margin – are challenging the mature market norm with binding contracts with coupled, subsidised, equipment. Continue reading Increase loyalty. Increase revenue. Reduce SAC/SRC. Is the combo possible?

Once you pop, you can’t stop?

When the rollout of 4G LTE eventually got up to speed in Western, Central and Southern Europe, it wasn’t long until operators started to report that the rollout was more or less completed, using population coverage as the proof point.

Let’s look at the stats from 19 operators who reported 4G population coverage both for December 2013 and 2014: Continue reading Why 100% population coverage on 4G doesn’t imply a great customer experience

Dutch operators KPN and Vodafone were both fined for violations of net neutrality today.

KPN got a fine of 250000 EUR for having blocked access to voice over IP services on public Wi-Fi hotspots. Vodafone was fined 200000 EUR for having zero-rated content from HBO. Continue reading Four years (and a net neutrality law) later, Dutch operators foul again

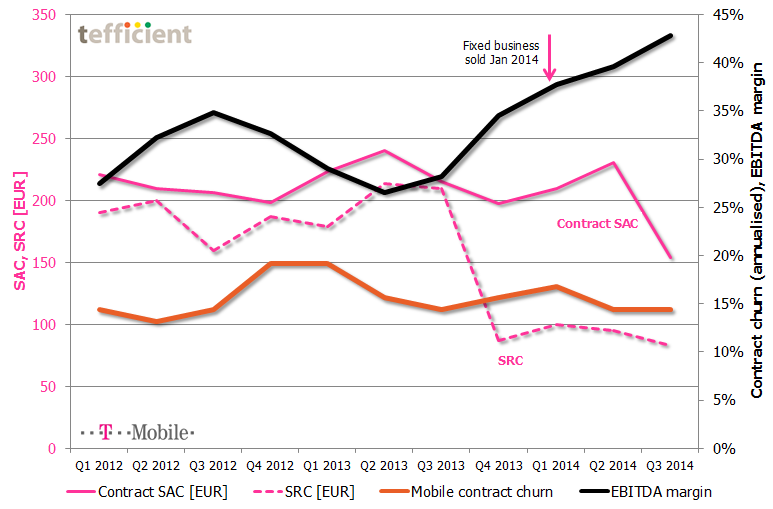

T-Mobile in the Netherlands continues its rally towards higher EBITDA margin: One year ago, it was 28%. Now it’s 43%. T-Mobile’s reported figures shows just how sensitive sales costs are to the mobile business margin.

In Q4 2013, T-Mobile cut its subscriber retention cost (SRC) from a level above 200 EUR to less than half. It has stayed at the new, lower, level since. Even though done during fourth quarter – where margin normally is weak due to seasonal sales – T-Mobile’s EBITDA margin took a leap upwards quarter-to-quarter. Another leap came in Q1 2014 when T-Mobile sold its fixed business (traded under the “Online” brand).

In the just-reported third quarter, T-Mobile’s EBITDA margin took yet a leap: This time due to a significant reduction in contract SAC (subscriber acquisition cost).

The text book says that such dramatic reductions in SAC/SRC would immediately penalise T-Mobile who would experience a shrinking base and market share since existing customers would churn out and new customers would’t join. The interesting thing is that existing customers haven’t left: The orange curve shows a stabilising contract churn of about 15%. T-Mobile has, however, still experienced a decline in their total base, but this has mainly been within prepaid. [The reported reduction in Q3 was almost exclusively to the disposal of the Simpel brand].

According to T-Mobile, the answer to how this has been possible comes in two parts:

In a market where T-Mobile’s two current MNO competitors KPN and Vodafone both go in the converged multi-play direction, it will be interesting to follow if T-Mobile can stay on this route – especially as Tele2 is about to enter the Dutch market as MNO within short.