Tefficient’s 34th public analysis on the development and drivers of mobile data ranks 104 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the full year of 2021 and in the first half of 2022.

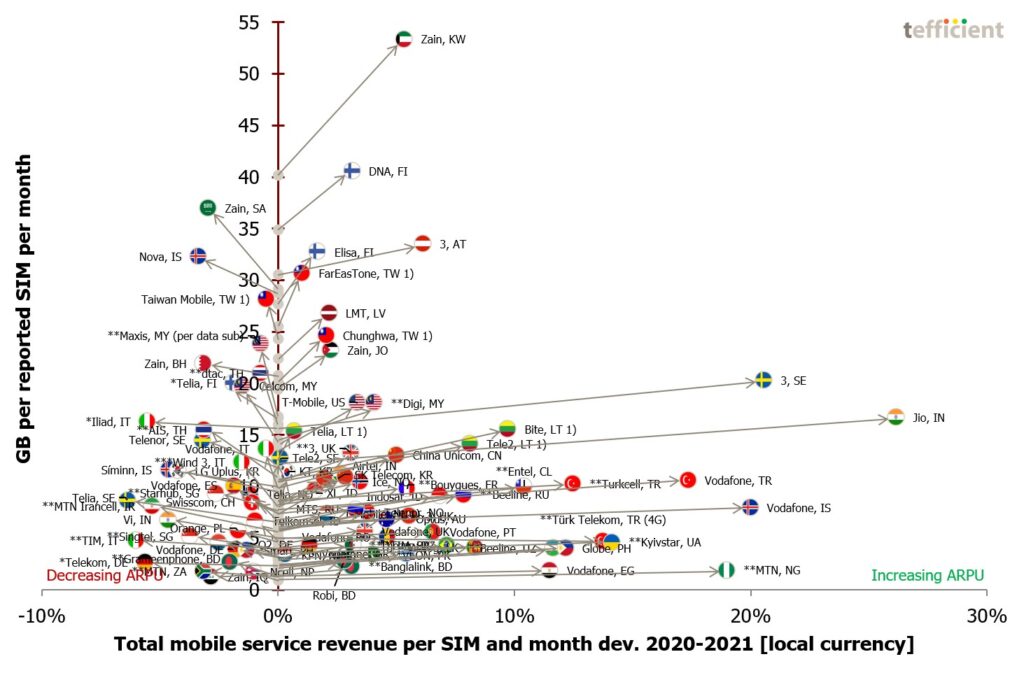

In 2021 – a year marked by COVID – the data usage per SIM grew for 97% of operators. The average traffic growth was 32%. A majority of operators, 62%, could turn data usage growth into ARPU growth.

62% of operators could turn data usage growth into ARPU growth

Tefficient’s 33rd public analysis of the development and drivers of mobile data compares 46 countries from all regions of the world.

In our previous reports for 2020 and 1H 2021 we could see that the pandemic drove mobile data usage – contrary to the belief that all that time we spent at home would offload mobile data traffic to Wi-Fi and fixed broadband.

But the usage backlash is here: During the second half of 2021 the demand for more mobile data slowed. If comparing countries where usage is available for both the first and the second half of the year, most experienced decelerating growth. There were even five countries with a decline in absolute usage: Australia, Iceland, Qatar, Austria and Bahrain.

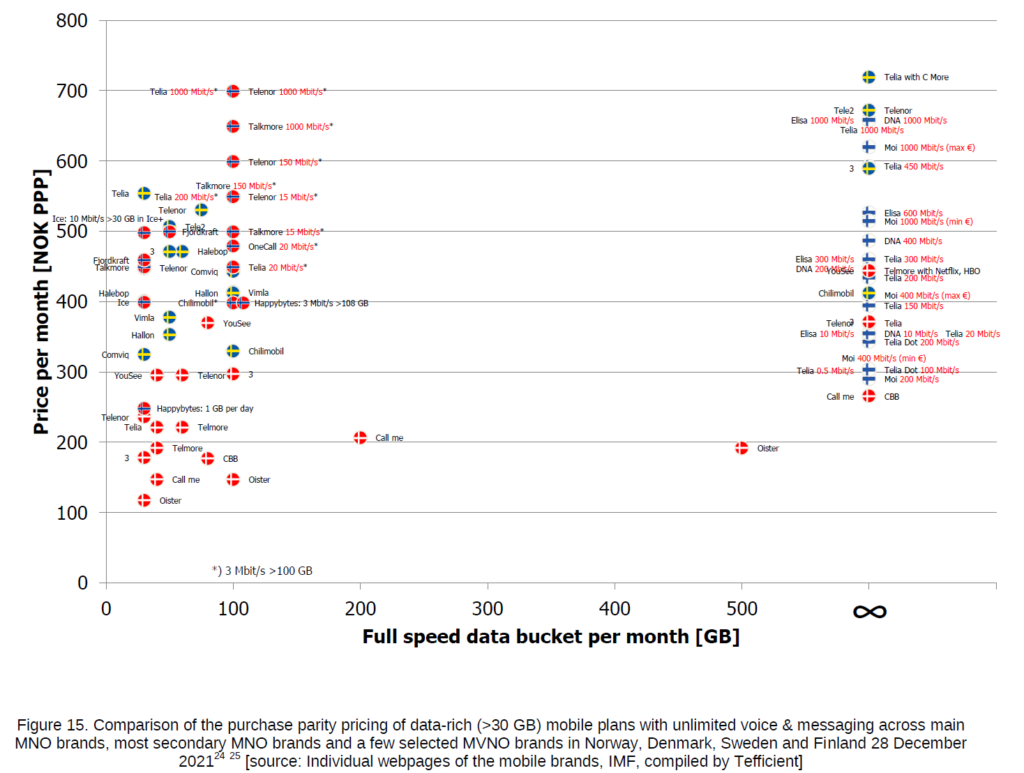

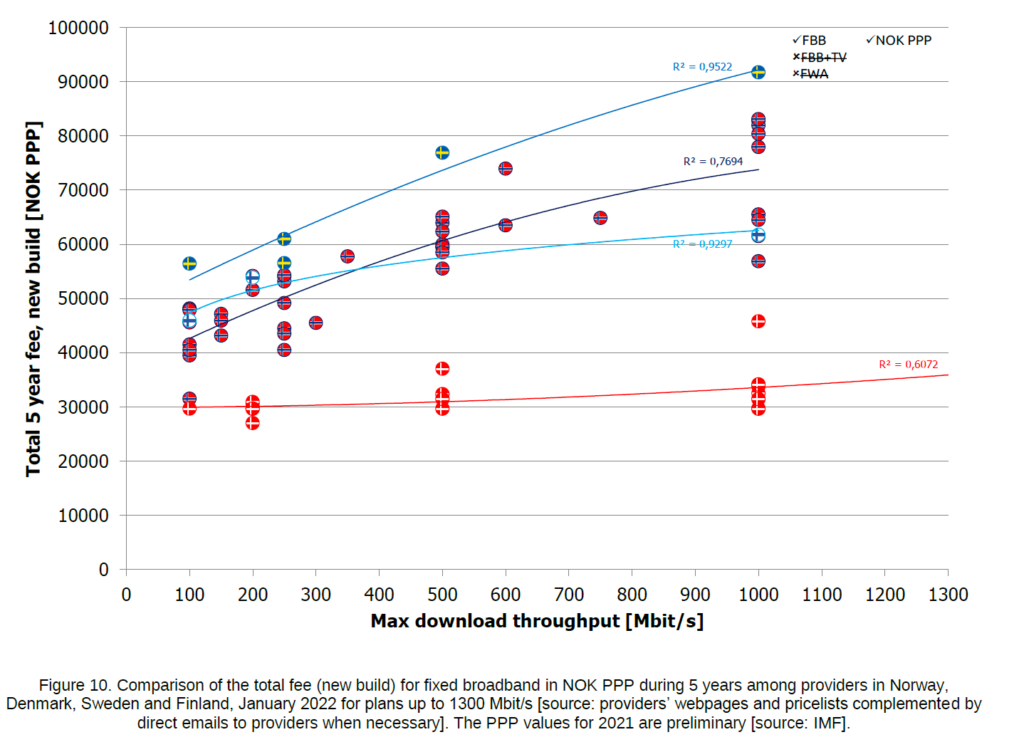

Both analyses are quite comprehensive and compare Norway to the three fellow Nordic countries Denmark, Sweden and Finland. It means that they are highly interesting not just for the industry and policy makers in Norway, but in all four countries.

Sample graph from the mobile reportSample graph from the fixed broadband report

Since the Ministry has made both analyses available for public download, you can access them directly and for free from here:

Gaming is a multi-billion dollar business – but operators have not really aimed to monetise it. Until now. Cloud gaming relies on a network’s ability to deliver a stable throughput and a low and stable latency. Gaming devices no longer need to have muscles; the rendering happens in powerful cloud servers. With cloud gaming, operators have the possibility to be relevant for gamers; operators can use network features to control and improve the gaming experience. Perhaps operators can even sell cloud gaming with differentiated experience tiers?

Opensignal’s Global Mobile Network Experience Awards 2022 showed that the mobile networks of Sweden, Finland – and especially Norway and Denmark – provide some of the best experiences in the world.

But there are many companies – some with global, some with local ambitions – that offer their take on who has the best mobile network. To differentiate, providers define different metrics and use different methodologies. Rather than boring you with those, we have compiled a cross-case table naming the winner per each metric across four global network experience specialists: Opensignal, Tutela, Ookla Speedtest and umlaut.

We have included the latest overall or 5G-specific tests made public in 2021 or 2022.

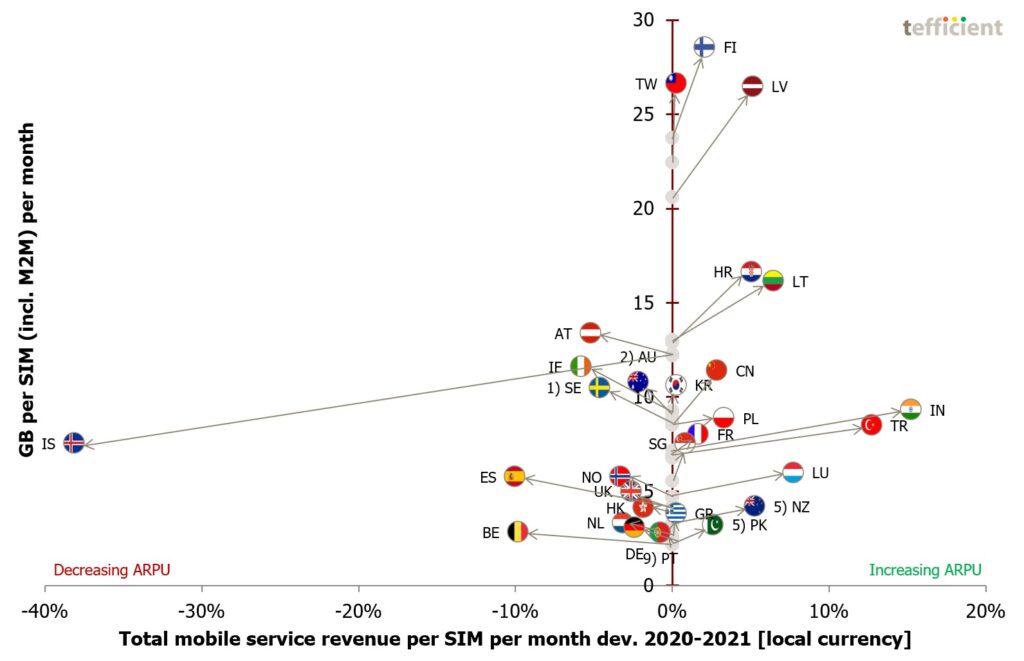

Tefficient’s 32nd public analysis of the development and drivers of mobile data compares 46 countries – now with Brazil added – from all regions of the world.

In our previous, full year 2020, report we could see that the pandemic drove mobile data usage – contrary to the belief that all that time we spent at home would offload mobile data traffic to Wi-Fi and fixed broadband.

Although the pandemic was still very much present in our daily life, the relaxation of restrictions in the first half of 2021 led to a more normal growth in mobile data usage.

Ericsson ConsumerLab published its latest report today.

The 5G Pacesetters report is the public outcome of a very ambitious project to design and analyse an index that measures both the 5G market performance and the consumer perception of 73 operators across 22 markets globally. Each 5G operator was analysed based on 105 criteria across 16 categories – from customer satisfaction to 5G offering, rollout and marketing efforts. It’s the first time a 5G index takes consumer satisfaction and consumers’ 5G leadership expectation into account.

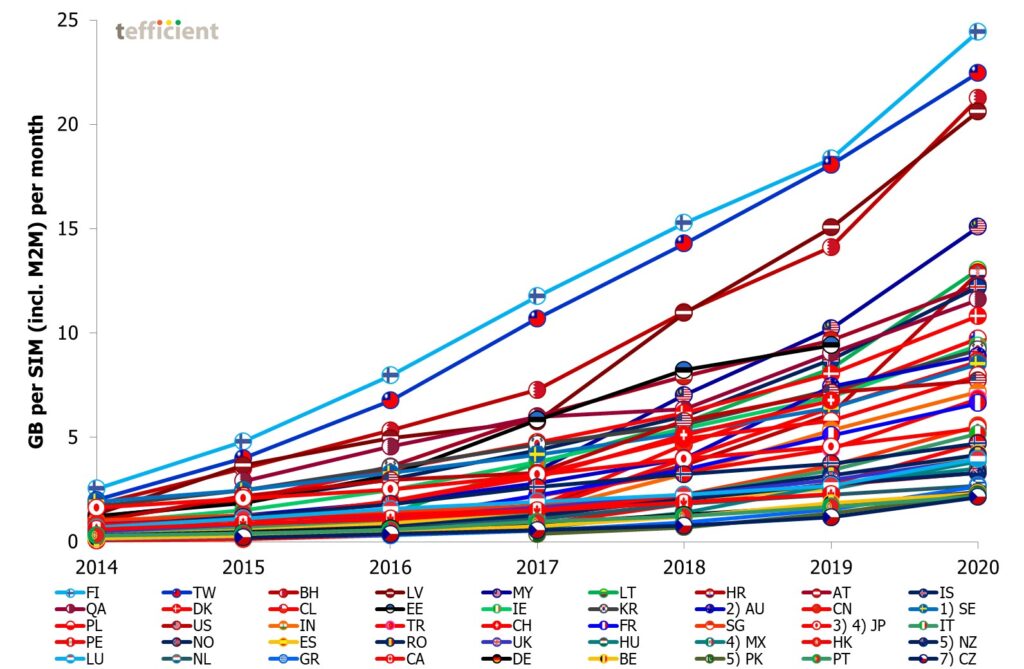

Tefficient’s 31st public analysis of the development and drivers of mobile data compares 45 countries from all regions of the world. The pandemic affected us all but although we to a high extent spent the year in our homes, mobile data usage increased in every single country. Mobile data is apparently not just used by people on the move.

Generally speaking, the growth accelerated in 2020; only a few countries experienced a slower growth rate.

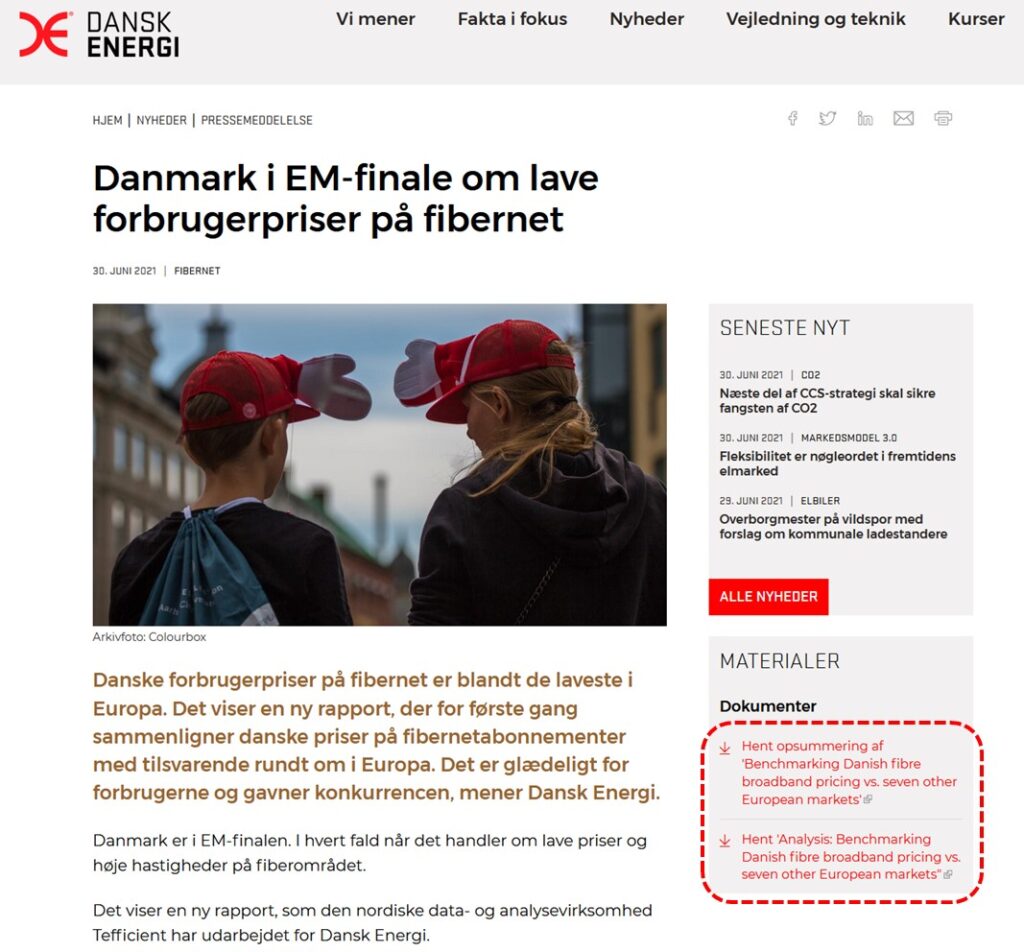

Dansk Energi (Danish Energy) is a business and interest organisation for energy companies in Denmark. These companies spearheaded the rollout of fibre networks in Denmark.

In a press release, Dansk Energi concludes that Denmark has among the lowest prices on fibre broadband in Europe. That conclusion is based on a comprehensive price benchmark performed by Tefficient – a benchmark which Dansk Energi has made public. Open the press release and download the benchmark in the “Dokumenter” area highlighted below.

Tefficient’s 30th public analysis on the development and drivers of mobile data ranks 105 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the full year of 2020.

The data usage per SIM grew for basically every operator. 39% could turn that data usage growth into ARPU growth.