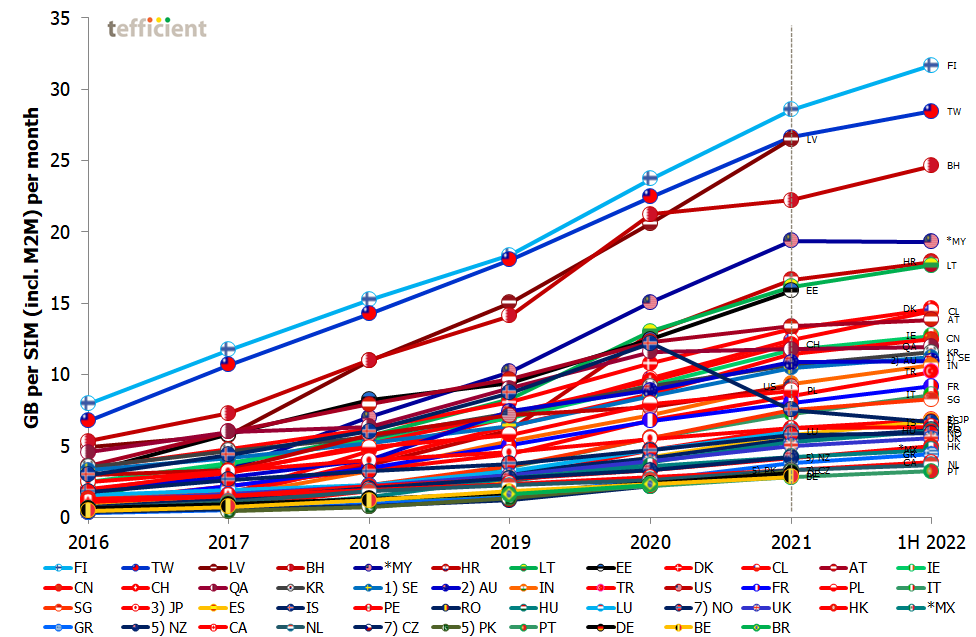

Tefficient’s 35th public analysis of the development and drivers of mobile data compares the trends of 46 countries from around the world. In our previous reports, we observed that the pandemic drove an increase in mobile data usage. However, during the second half of 2021 and into 2022, the demand for more mobile data slowed.

Greece experienced the fastest growth in mobile data usage, with a 45% increase. On the other end of the spectrum, Qatar, Peru, Malaysia, and Austria saw unusually slow growth rates of just 1-3%.

Fiberalliancen is a trade association for companies that own, operate and use fibre networks in Denmark. It is a part of Green Power Denmark.

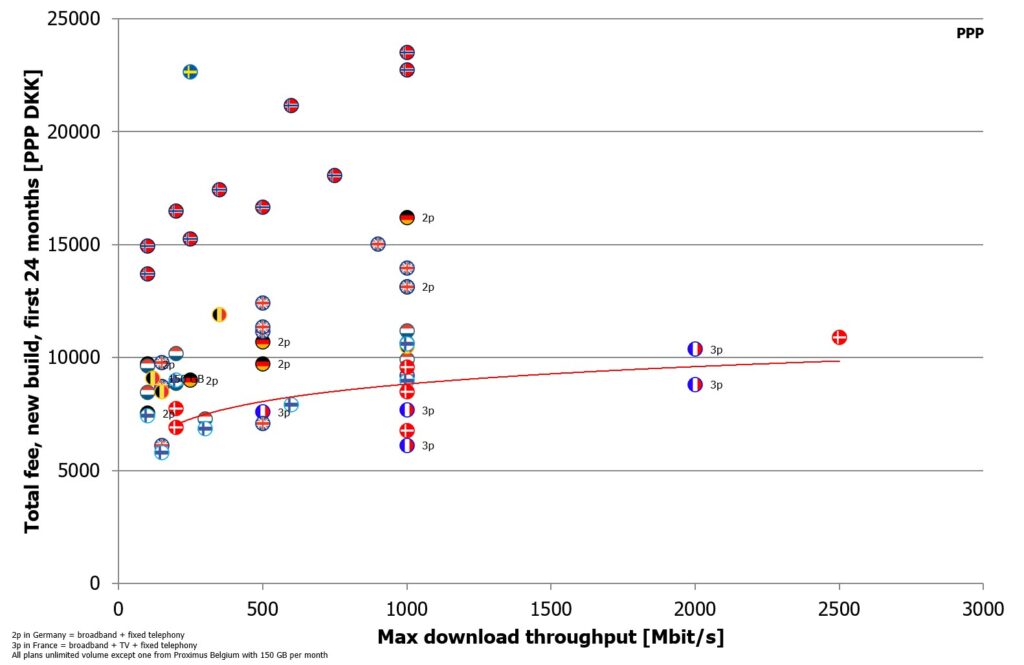

For the second time (the first analysis was done in 2021), Tefficient has performed a comprehensive fibre broadband pricing benchmark covering nine European markets: Denmark, Sweden, Norway, Finland (new since 2021), Germany, the Netherlands, Belgium, the UK and France.

As part of a press release, Fiberalliancen makes Tefficient’s analysis publicly available. Download it from the right ‘Links’ column. It’s in English.

The release concludes that:

Denmark has some of the lowest consumer prices for both new and existing fibre connections. Only French consumers generally get a better deal than Danish consumers.

Danish consumer prices – both for new and existing connections – have overall fallen from 2021 to 2022. This is only seen in Denmark and the UK.

According to Ookla, Denmark has the fastest median broadband download speeds among the countries included in the comparison.

Tefficient’s approach has been thorough and the results are presented in a set of graphs like below.

Tefficient’s 33rd public analysis of the development and drivers of mobile data compares 46 countries from all regions of the world.

In our previous reports for 2020 and 1H 2021 we could see that the pandemic drove mobile data usage – contrary to the belief that all that time we spent at home would offload mobile data traffic to Wi-Fi and fixed broadband.

But the usage backlash is here: During the second half of 2021 the demand for more mobile data slowed. If comparing countries where usage is available for both the first and the second half of the year, most experienced decelerating growth. There were even five countries with a decline in absolute usage: Australia, Iceland, Qatar, Austria and Bahrain.

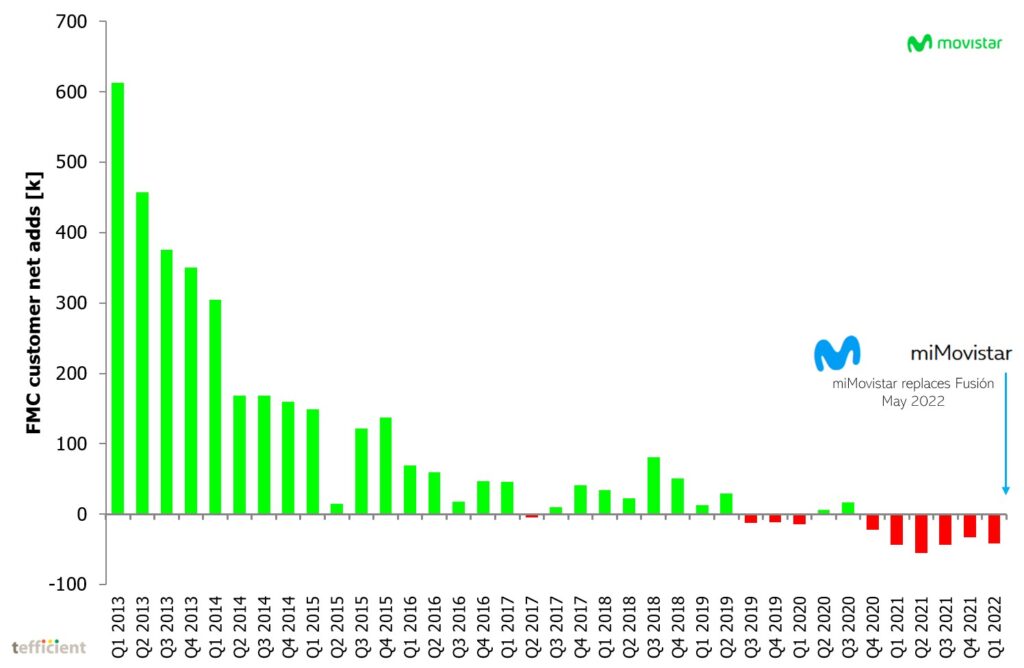

During the last decade, fixed-mobile convergence – FMC for short – has come to dominate how connectivity and entertainment are sold to households in European markets like Spain, France, Portugal, Belgium and the Netherlands.

In Spain, around three quarters of the households currently subscribe to an FMC plan covering at least fixed broadband and one or multiple mobile subscriptions. Often TV or other entertainment services are included too.

Initially FMC was sold with massive discounts and the base grew quickly as it was a no-brainer not to buy everything from the same operator. Churn levels were improved dramatically too when a churn decision no longer just affected one service for one household member, but many different services consumed by many different people. [Some find it easier to negotiate with an operator than with members of the family].

In later years, FMC ARPU increased much, driven by more content (and more expensive content such as football) in the mix. Eventually, the operator thirst for higher and higher ARPU might have been the start of a negative base trend for FMC. In the graph below, we show the FMC net adds for Movistar (Telefónica Spain) since the launch of its Fusión FMC product.

Opensignal’s Global Mobile Network Experience Awards 2022 showed that the mobile networks of Sweden, Finland – and especially Norway and Denmark – provide some of the best experiences in the world.

But there are many companies – some with global, some with local ambitions – that offer their take on who has the best mobile network. To differentiate, providers define different metrics and use different methodologies. Rather than boring you with those, we have compiled a cross-case table naming the winner per each metric across four global network experience specialists: Opensignal, Tutela, Ookla Speedtest and umlaut.

We have included the latest overall or 5G-specific tests made public in 2021 or 2022.

Tefficient’s 32nd public analysis of the development and drivers of mobile data compares 46 countries – now with Brazil added – from all regions of the world.

In our previous, full year 2020, report we could see that the pandemic drove mobile data usage – contrary to the belief that all that time we spent at home would offload mobile data traffic to Wi-Fi and fixed broadband.

Although the pandemic was still very much present in our daily life, the relaxation of restrictions in the first half of 2021 led to a more normal growth in mobile data usage.

Ericsson ConsumerLab published its latest report today.

The 5G Pacesetters report is the public outcome of a very ambitious project to design and analyse an index that measures both the 5G market performance and the consumer perception of 73 operators across 22 markets globally. Each 5G operator was analysed based on 105 criteria across 16 categories – from customer satisfaction to 5G offering, rollout and marketing efforts. It’s the first time a 5G index takes consumer satisfaction and consumers’ 5G leadership expectation into account.

Tefficient’s 31st public analysis of the development and drivers of mobile data compares 45 countries from all regions of the world. The pandemic affected us all but although we to a high extent spent the year in our homes, mobile data usage increased in every single country. Mobile data is apparently not just used by people on the move.

Generally speaking, the growth accelerated in 2020; only a few countries experienced a slower growth rate.

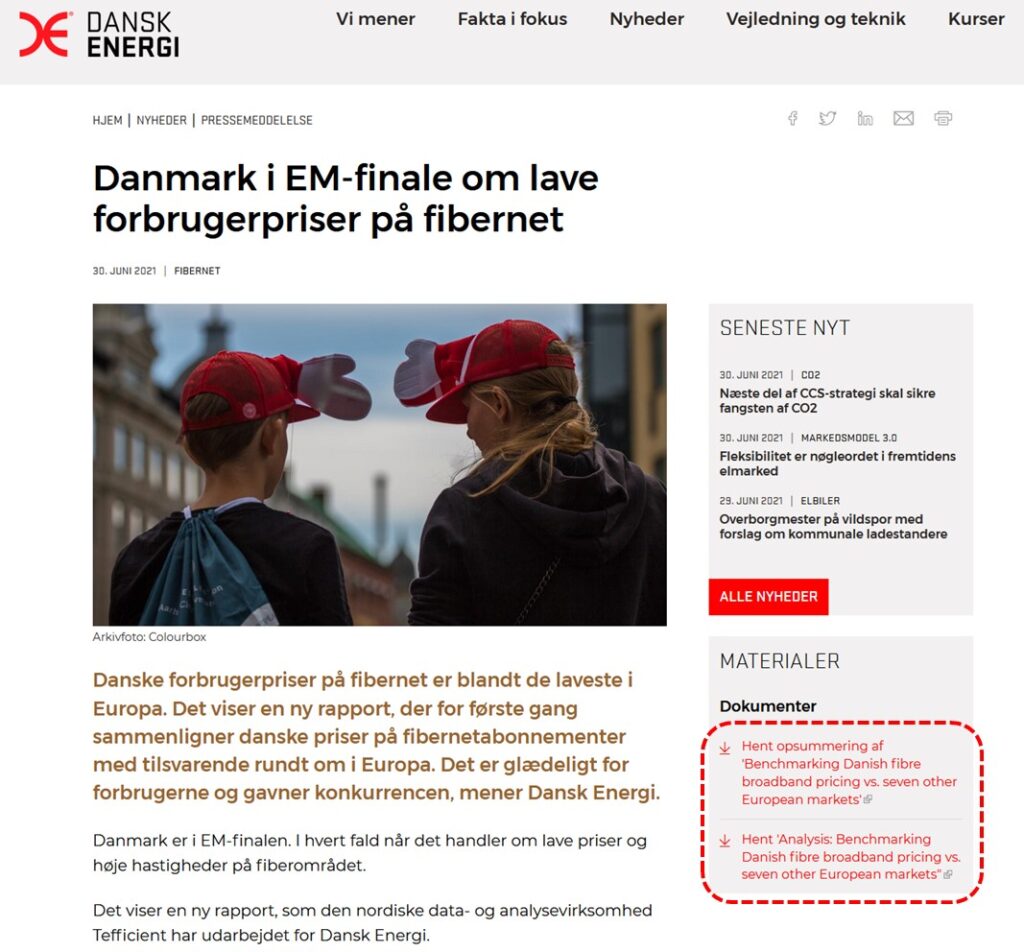

Dansk Energi (Danish Energy) is a business and interest organisation for energy companies in Denmark. These companies spearheaded the rollout of fibre networks in Denmark.

In a press release, Dansk Energi concludes that Denmark has among the lowest prices on fibre broadband in Europe. That conclusion is based on a comprehensive price benchmark performed by Tefficient – a benchmark which Dansk Energi has made public. Open the press release and download the benchmark in the “Dokumenter” area highlighted below.

When COVID-19 hit the world and governments and authorities enforced restrictions on the society, the whole economy trembled. The telco business was affected, but the change in movement and usage patterns didn’t just bring negatives. Although the high margin mobile roaming revenue was lost, mature market telcos have, generally speaking, never reported higher margins than what they did in the just-closed third quarter of 2020.

We’ll show you what the key to this margin increase is.