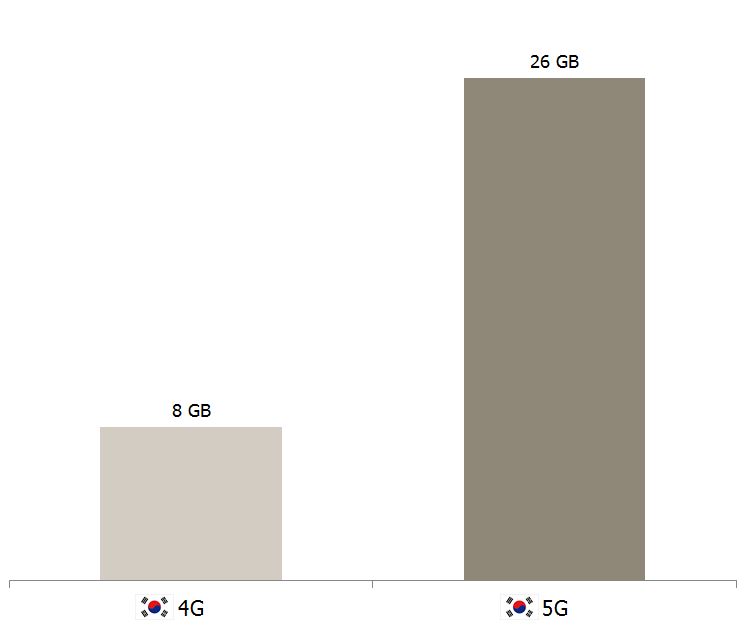

Nowhere else in the world will you find as many 5G users as in South Korea. Nowhere else will you find as many 5G base stations up and running. If there ever was a race to 5G, the Korean government and industry won it.

Seeing is believing: After having dug up, read and compiled all reporting and data on Korea’s mobile business there was no other way forward than to seeing it for ourselves and interview people involved in creating Korea’s ‘5G wonder’.

We spent eight busy days (11-18 July) in Seoul to finish a comprehensive 106-page analysis – full of graphs and photos – with recommendations for European operators.

This is tefficient’s 23rd public analysis of the development and drivers of mobile data.

Mobile data usage is still growing in all of the 39 countries covered by this analysis. Two countries stand out – China and India.

But China and India aren’t yet challenging the usage top – where the two unlimited superpowers, Finland and Taiwan, still reign.

Data-only remains a key driver for overall usage and new figures from Czech Republic, Latvia, Finland and Austria add insight to the extreme usage pattern of fixed wireless access.

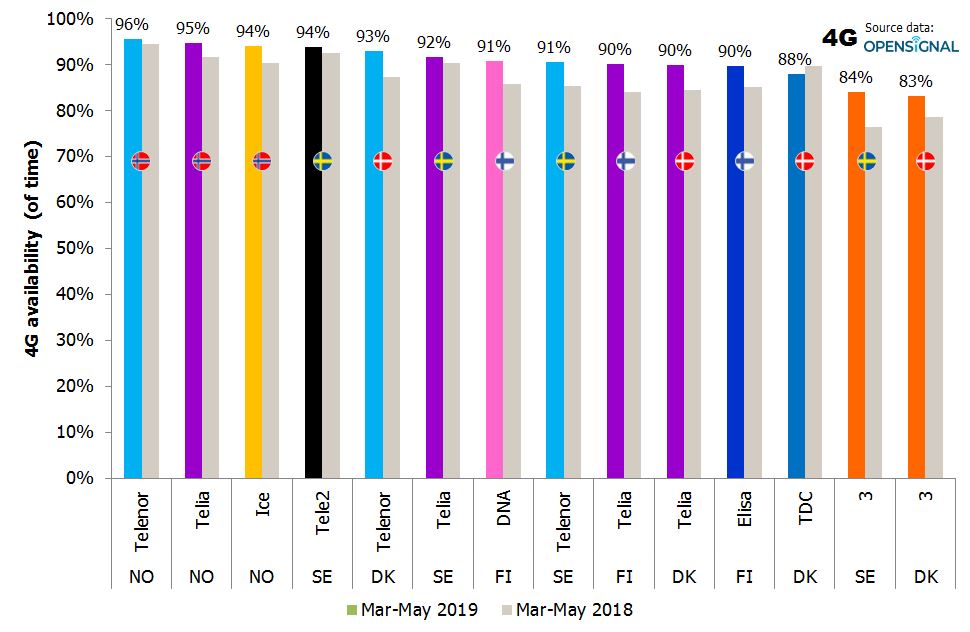

This is our fourth comparison of the mobile network experiences in the Nordics based on performance data from Opensignal. There are more details and background is the previous (one–two–three) blogs.

This time the data is gathered from March to May 2019. The data has not been published by OpenSignal but has been shared with us through Opensignal’s analyst program.

4G availability

The graph below ranks the fourteen operators in Norway, Sweden, Denmark and Finland after how large proportion of time 4G capable devices have been connected to 4G. Opensignal calls this 4G availability.

Conducting and transcribing 22 interviews with 23 senior executives from telecom operators, handset and chip manufacturers, start-ups, academia and think tanks on the potential of 5G for consumers.

These interviews were, alongside focus groups, used as input to design Ericsson ConsumerLab’s consumer research ultimately covering 22 countries and over 35000 smartphone owners globally.

The interviews form an integral part of the 5G consumer potential report as issued by Ericsson ConsumerLab in May 2019. All interviewees are named in the report. Thank you for your kindness!

When you use a mobile network, your traffic has to co-exist with traffic generated by other users currently connected to the same cell. Your speed experience will depend on how much and what type of traffic those other users generate. It will also depend on how your operator has dimensioned that cell, i.e. how many carriers they have put up. Ultimately that depends on the available spectrum your operator has access to.

When operators want to convince us how great their networks are, they typically talk about download speed, i.e. how many Mbit/s users on their network averagely get when downloading something from the internet. It is being supported by a number of independent network performance specialists – Tutela, Opensignal, Ookla, P3, RootMetrics – issuing country reports naming winning networks.

These reports are actually often multi-faceted with several performance metrics, but that is often too complex to use in marketing, operators think. The simplified marketing message becomes: Speed is good – and we won.

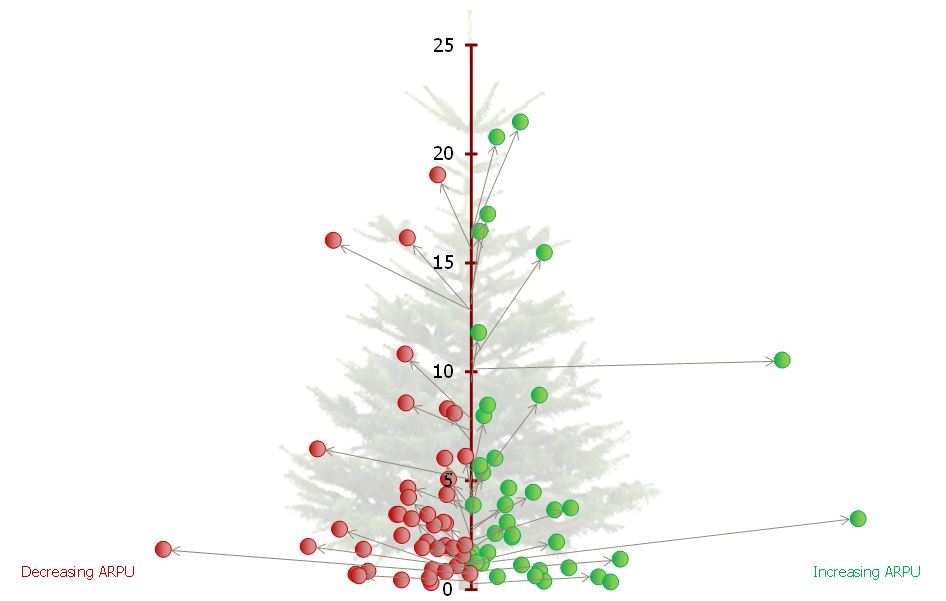

Which operator has the world’s highest data usage?

Which operator carries the most data traffic in the world?

Which operator earns the most – or the least – per GB?

This is tefficient’s 22nd public analysis on the development and drivers of mobile data. We have ranked 90 reporting or reported operators based on average data usage per SIM, total data traffic and revenue per gigabyte in 2018.

Final! Mobile data usage and revenue for 39 countries

This is tefficient’s 21st public analysis of the development and drivers of mobile data.

Mobile data usage is still growing in all of the 39 countries covered by this analysis. But there are two countries that stand out – China and India. In the first half of 2018, these two ‘developing’ nations have overtaken several mature markets when it comes to average data consumption per subscription. The growth is incredibly fast and driven by 4G.

Two years ago, telcos were still proudly reporting their progress in utilisation of their own public Wi-Fi hotspots for cost efficient offloading of mobile data. Public Wi-Fi was also positioned as an investment in a better customer experience – especially in public indoor environments. Telcos that were late with 4G – such as in Taiwan and Belgium – could utilise their public Wi-Fi to bridge the transition from 3G to 4G.

Those of you that read our series of international mobile data analyses know that Finland is the country with the highest average mobile data consumption in the world.

Truly unlimited mobile data is a key explanation to this: 66% of Finland’s mobile subscriptions (excl. M2M) had unlimited mobile data in June. As a direct consequence of this Finns have developed a readiness to try out new apps and services at any location and at any time – as they never have to consider the data consumption or the associated cost. The habit of ‘Wi-Fi hunting’ is not spread in Finland.

American carriers and uncarriers are embracing fixed wireless as one of the first use cases that 5G will solve. Verizon finally lifted the curtain on its fixed wireless offering yesterday: Verizon 5G Home. October 1 it will be available for 50 USD per month to existing Verizon customers in certain areas in Houston, Indianapolis, Los Angeles and Sacramento.

T-Mobile’s 5G will – to use their own words – have more ‘breadth and depth‘ than Verizon’s. With 5G, T-Mobile will position itself within fixed wireless for the first time:

“51% of Americans have only one high-speed broadband option – no choice at all! The combined company will create a viable alternative for millions by enabling mobile connections that rival broadband, driving prices lower and improving service.”

The only caveat when it comes to T-Mobile’s ambition is that it is conditional. This will happen if T-Mobile and Sprint are allowed to merge – a decision not yet made.

This is tefficient’s 21st public analysis of the development and drivers of mobile data.

This is tefficient’s 21st public analysis of the development and drivers of mobile data. Two years ago, telcos were still proudly reporting their progress in utilisation of their own public Wi-Fi hotspots for cost efficient offloading of mobile data. Public Wi-Fi was also positioned as an investment in a better customer experience – especially in public indoor environments. Telcos that were late with 4G – such as in Taiwan and Belgium – could utilise their public Wi-Fi to bridge the transition from 3G to 4G.

Two years ago, telcos were still proudly reporting their progress in utilisation of their own public Wi-Fi hotspots for cost efficient offloading of mobile data. Public Wi-Fi was also positioned as an investment in a better customer experience – especially in public indoor environments. Telcos that were late with 4G – such as in Taiwan and Belgium – could utilise their public Wi-Fi to bridge the transition from 3G to 4G.

T-Mobile’s 5G will – to use their own words – have more ‘

T-Mobile’s 5G will – to use their own words – have more ‘