Norway’s Ministry of Digitalisation and Public Governance today published two analyses commissioned from Tefficient.

The conclusion is summarised (in Norwegian) in a press release from the Ministry.

Both analyses are very comprehensive and compare Norway to the three fellow Nordic countries Denmark, Sweden, and Finland. It means that they are highly interesting not just for the industry and policy makers in Norway, but in all four countries.

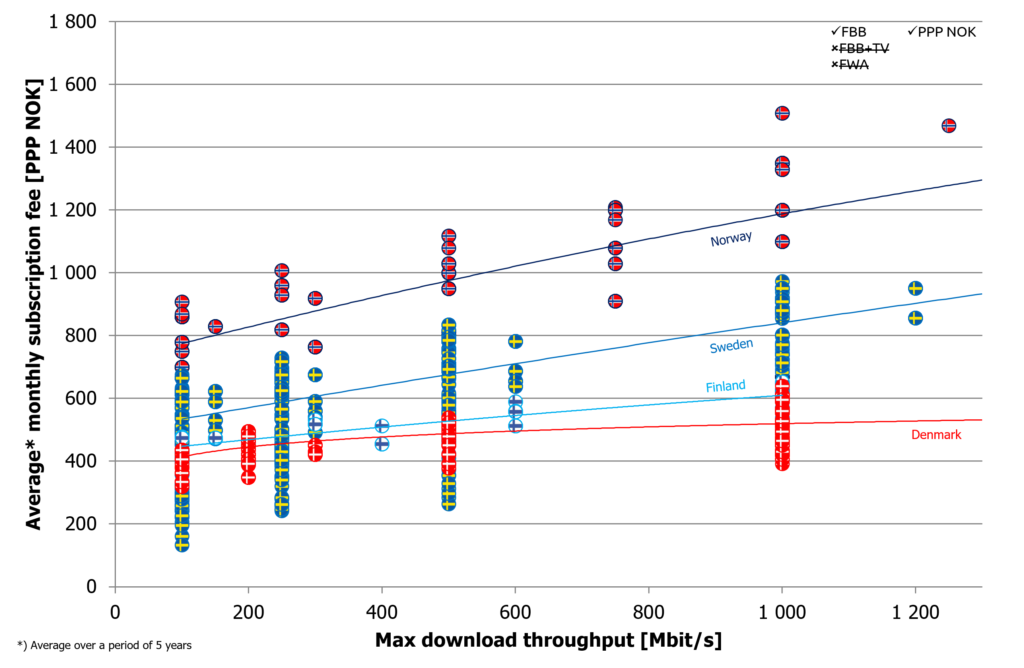

An example graph from the fixed analysis shows how the average monthly subscription fee compares between different plans with different maximum download throughput:

The average monthly subscription fee during the first 5 years of a fixed broadband contract, measured in purchasing power parity adjusted Norwegian kroner. Each dot represents an actual consumer offer. In total 6500 offers across 385 addresses were documented.

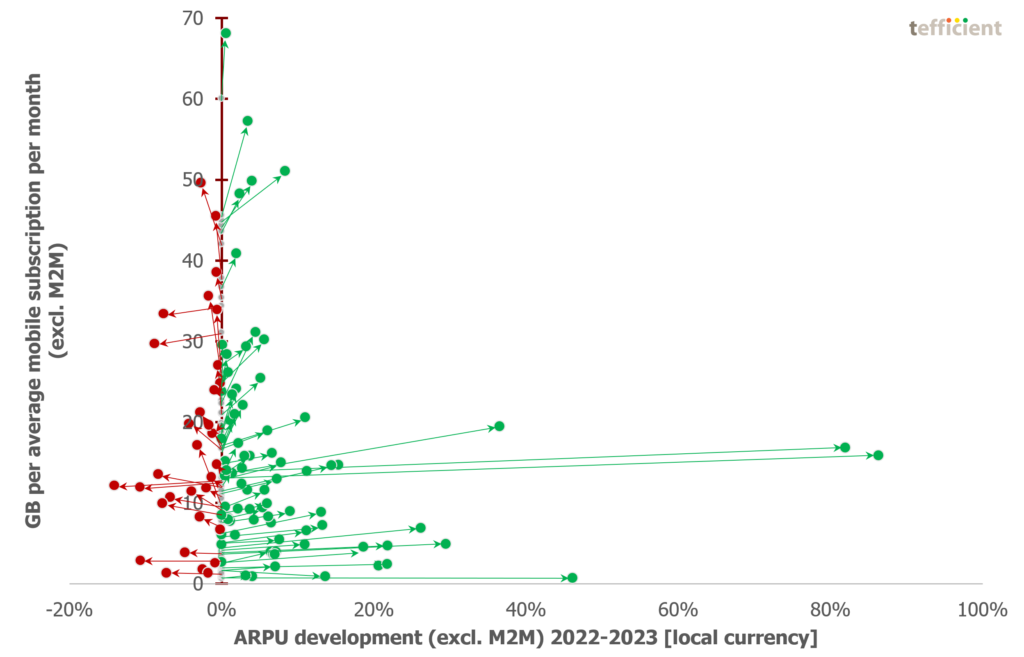

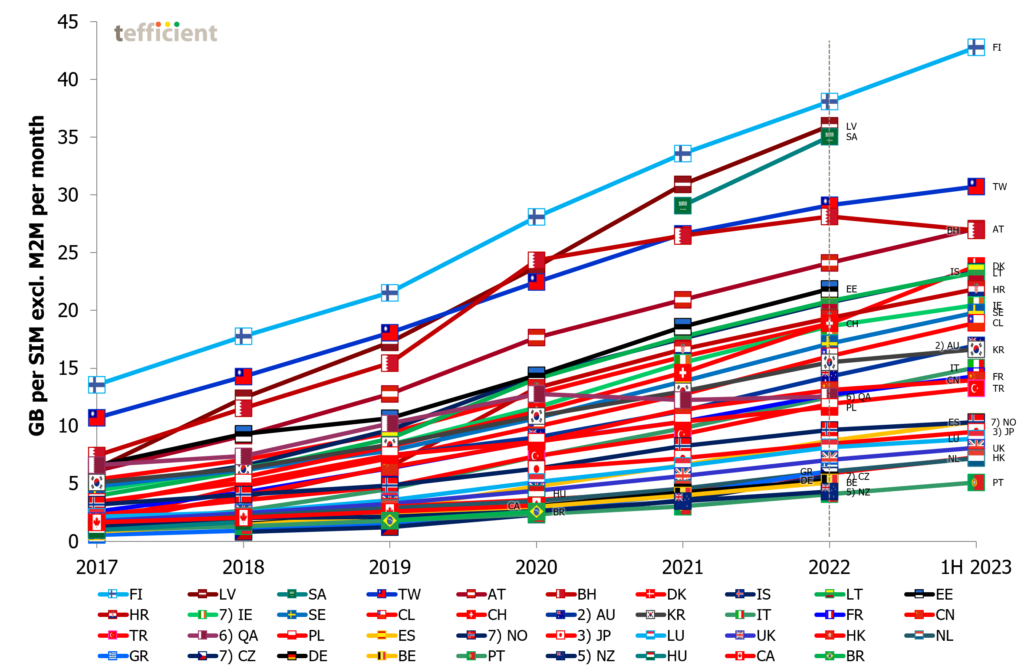

In Tefficient’s 42nd public analysis of mobile data trends, 123 operators are ranked based on metrics like average data usage per subscription, total data traffic, and revenue per gigabyte.

In 2023, 93% of operators experienced growth in data usage per subscription, with 71% of them successfully converting this into higher ARPU.

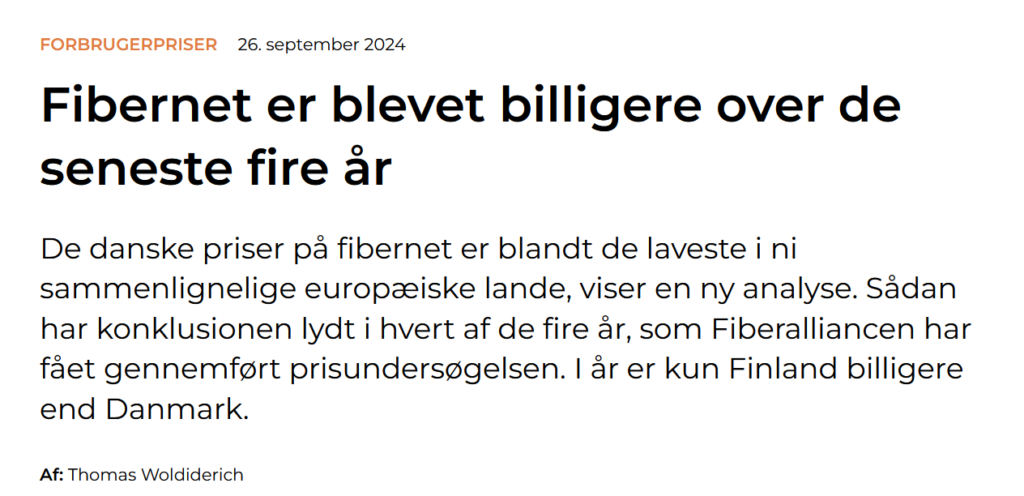

Fiberalliancen is a trade association representing companies that own, operate, and use fibre networks in Denmark. It is part of Green Power Denmark.

For the fourth time, following previous reports in 2021, 2022, and 2023, Tefficient has conducted an extensive fibre broadband pricing benchmark across nine European markets: Denmark, Sweden, Norway, Finland, Germany, the Netherlands, Belgium, the UK, and France.

“Germany and the Netherlands have also experienced falling fiber prices, but Denmark has seen the biggest overall price drop over the four years.”

In a press release, Fiberalliancen introduces Tefficient’s latest analysis and makes it publicly available for download at the bottom of the page under ‘Læs hele analysen fra Tefficient‘. If you do not read Danish, don’t worry; the report is in English.

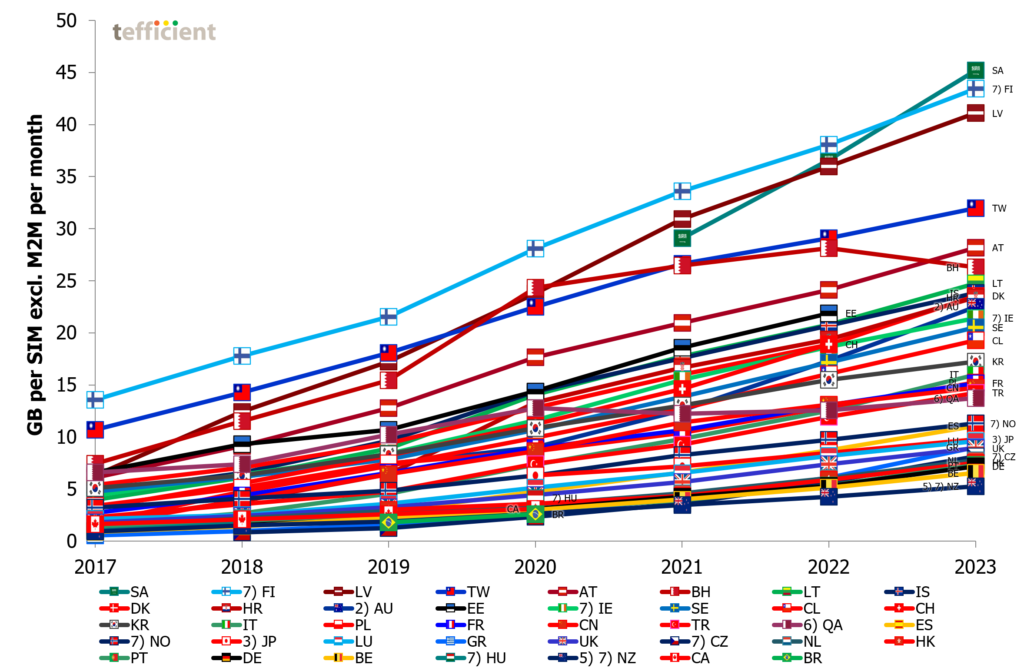

Tefficient’s 41st public analysis of mobile data development and drivers compares 39 countries worldwide, where M2M/IoT can be excluded from the total bases. Mobile data usage grew in 38 of these, with Bahrain as the only exception.

Finland no longer leads in usage

For the first time since 2013, Finland doesn’t lead in usage. Saudi Arabia is the new world leader with more than 45 GB per average subscription in 2023.

The Hellenic Telecommunications & Post Commission, EETT, functions as Greece’s national regulatory authority for telecommunications.

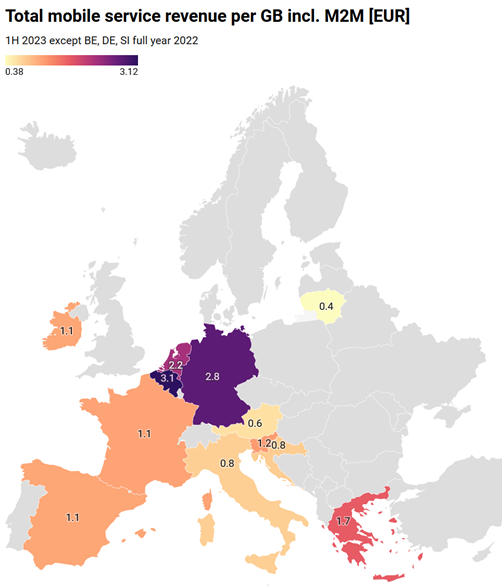

In response to EETT’s request, Tefficient has conducted an extensive benchmark analysis, focusing on value for money, spanning twelve EU and Euro countries: Austria, Belgium, Croatia, France, Germany, Greece, Ireland, Italy, Lithuania, the Netherlands, Slovenia, and Spain.

While the primary focus of the benchmark is on Greece, its insights provide valuable perspectives for the telecommunications industry in the remaining eleven countries.

Key conclusions for Greece include:

Mobile Average Revenue Per User (ARPU) is approximately on par but with a notable increase

Mobile data usage is low but exhibits the most significant growth

Voice usage is the highest among the peer group but continues to see robust growth

The total mobile revenue per gigabyte of mobile data is high but demonstrates a marked decrease

Voice revenue per mobile voice minute aligns with the median and experiences median erosion

In terms of value for money, Greece ranks weaker in data offerings compared to most of its peers but stronger than most in voice services

Several selected example graphs are presented below.

During the early days of 5G, the mobile industry was sometimes caught saying that mobile – with the help of 5G – would kill Wi-Fi. That hasn’t happened, obviously. Usage of public Wi-Fi hotspots would likely decline if more users had mobile data plans that are unlimited in volume. T-Mobile suggested it in this blog post from December 2021.

Blog from T-Mobile US mentioning that 13% fewer Magenta MAX users are connecting to Wi-Fi.

But even if so, few users would stop using their Wi-Fi at home. Home is where Wi-Fi connects automatically and where a majority of usage takes place.

Ironically, the greatest use case for 5G so far is to substitute fixed broadband. 5G has encouraged many MNOs globally to, for the first time, seriously push fixed wireless access, or FWA, services using their mobile networks. Why is it ironic? The mobile industry has for more than a decade specified and built 5G, the most advanced and best mobile technology so far, but its primary use case to date is fixed. Sitting still.

Airtel India’s Xstream AirFiber.

While FWA could substitute a fixed broadband connection, especially DSL and cable, it does not substitute Wi-Fi, though. The FWA router converts 5G into Wi-Fi. Wi-Fi, not 5G, remains the interface to the connected devices in the home.

So while we, already, are tired of our own headline and the whole notion of “Wi-Fi vs. 5G”, we need to check the facts. After all, we are Tefficient and believers in data.

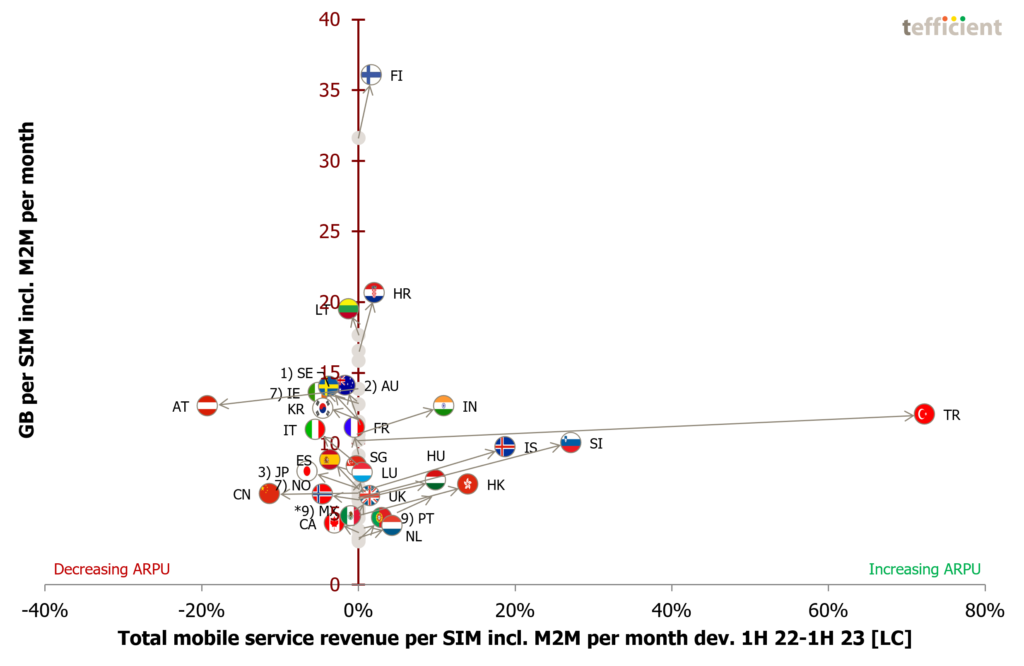

Tefficient’s 40th public analysis of mobile data development and drivers compares 47 countries worldwide, including M2M/IoT in the total bases. Mobile data usage grew in 44 of them, with Austria, Bahrain and China being exceptions.

If you’d rather see the analysis excluding M2M, go here.

When usage grows, the growth rates are slowing. Cyprus, however, had an astonishing growth rate of 123%, in stark contrast to much slower growth rates, or even declines, elsewhere.

Tefficient’s 39th public analysis of mobile data development and drivers compares 39 countries worldwide, where M2M/IoT can be excluded from the total bases. Mobile data usage grew in 38 of them – with Bahrain as the only exception.

If you’d rather see the analysis including M2M, go here.

When usage grows, the growth rates are slowing. Portugal leads with a growth rate of 47%, contrasting with Taiwan‘s modest 8% growth. Bahrain experienced a decline of 6% in data usage.

Data-only subscriptions continue to dominate average mobile data usage, although their market share remains limited. Latvia‘s average data-only subscription consumed 138 GB per month in 2022 while Austria recorded 115 GB in the first half of 2023. In the FWA-only category, Australia had a remarkable 334 GB per month in 1H 2023.

While data-only drives traffic, the same can’t be said for 5G

Reporting is imperfect, but there are only three countries with disproportionately high 5G traffic in relation to their 5G bases: South Korea, Austria and Saudi Arabia. We explain what these countries do and what other countries are missing.

The Q3 results just reported by Telia Company, Telenor, Tele2, 3 Scandinavia and Elisa show that it’s quite difficult not to be successful as a Nordic telco today.

Revenue and ARPU is growing. OPEX grows too, but slower than the revenue, so the EBITDA margins are increasing. Churn is decreasing. CAPEX is in decline. More cash is being generated.

We have identified seven signs that competition in cooling down in Nordic telco.

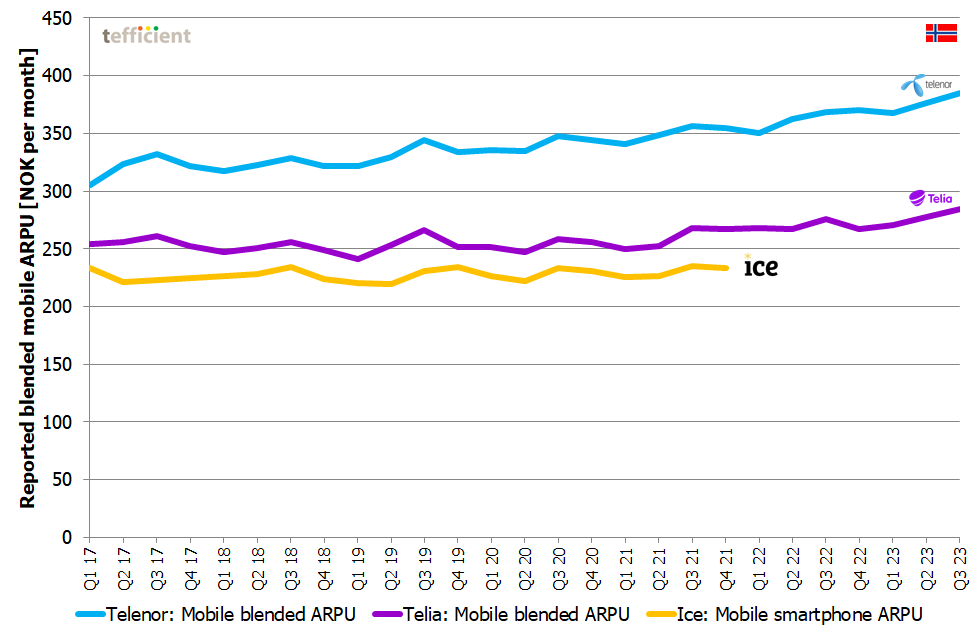

Sign 1. Mobile ARPU grows

Let’s start with Norway. The reported blended mobile ARPU has quite steadily increased for the two MNOs that still report it. For Telenor it grew 4% year-on-year to Q3 2023. For Telia it grew 3%.

Figure 1. Mobile ARPU, Norway (source data: operator reports)

In Sweden, the ARPU development has been a bit more dramatic than in Norway. Three players, first 3, then Telenor and the B2B side of Tele2, witnessed their ARPUs going down from 2018 to the first half of 2021. A corona effect, you might say. Not really; it started before corona started (Q1 2020) and compare with Telia who could keep their ARPU steady or even increase it when 3, Telenor and Tele2 B2B seemingly fought a battle on price.

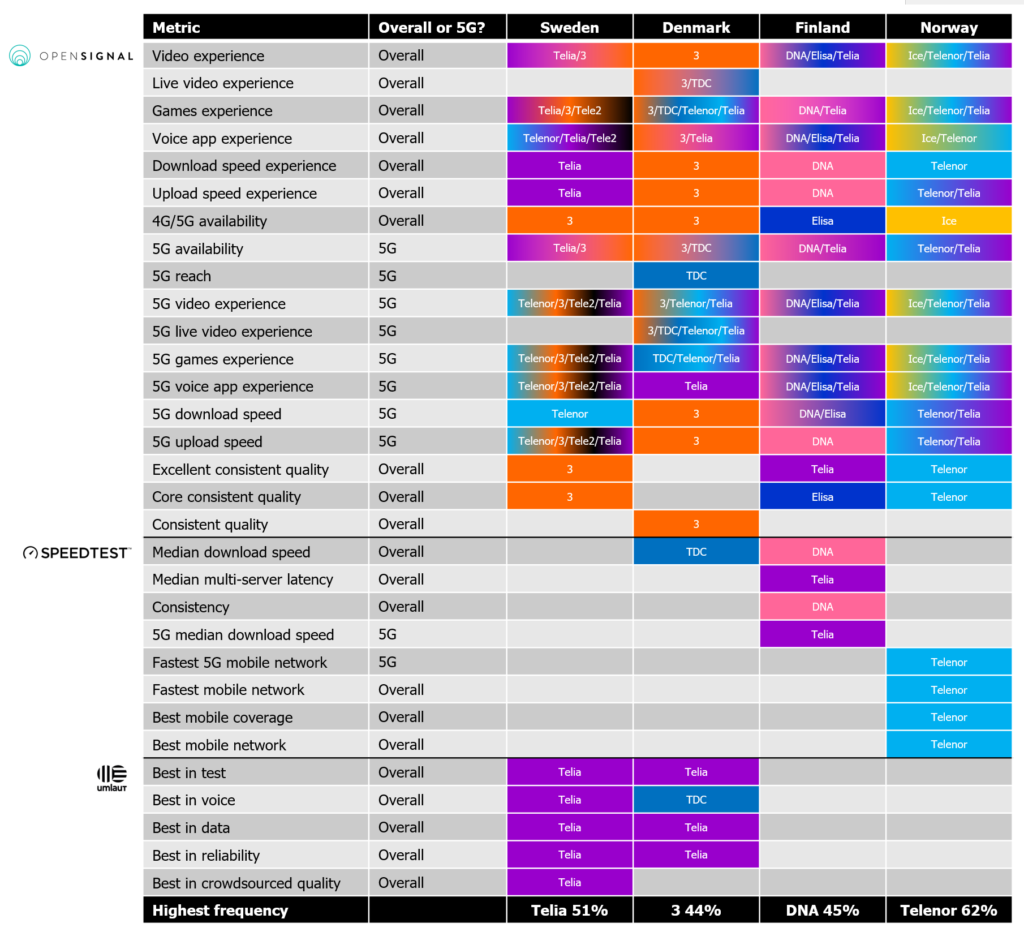

But there are several companies – some with global, some with local ambitions – that offer their take on who has the best mobile network. To differentiate, providers define different metrics and use different methodologies. Rather than boring you with those, we have compiled a cross-case table naming the winner per each metric across three global network experience specialists: Opensignal (now having merged with Tutela), Ookla Speedtest and umlaut.

We have included the latest overall or 5G-specific tests made public in Q4 2022 or 2023.