Which cloud gaming and immersive video propositions are leading operators offering their 5G customers? How have operators gone about it; partnering with global brands, integrating a white label product – or even building it on their own?

KT celebrating 40k GameBox customers one month after launch

What about exclusivity? Can anyone buy or is it just for connectivity customers? Even for 5G customers only? Or have operators made the cloud gaming/immersive video service inclusive? If so, on an all plans or just on the more premium plans?

In this project we summarised and categorised all propositions in leading 5G markets globally and could spot some global trends.

Tefficient’s 29th public analysis of the development and drivers of mobile data compares 44 countries from all regions of the world.

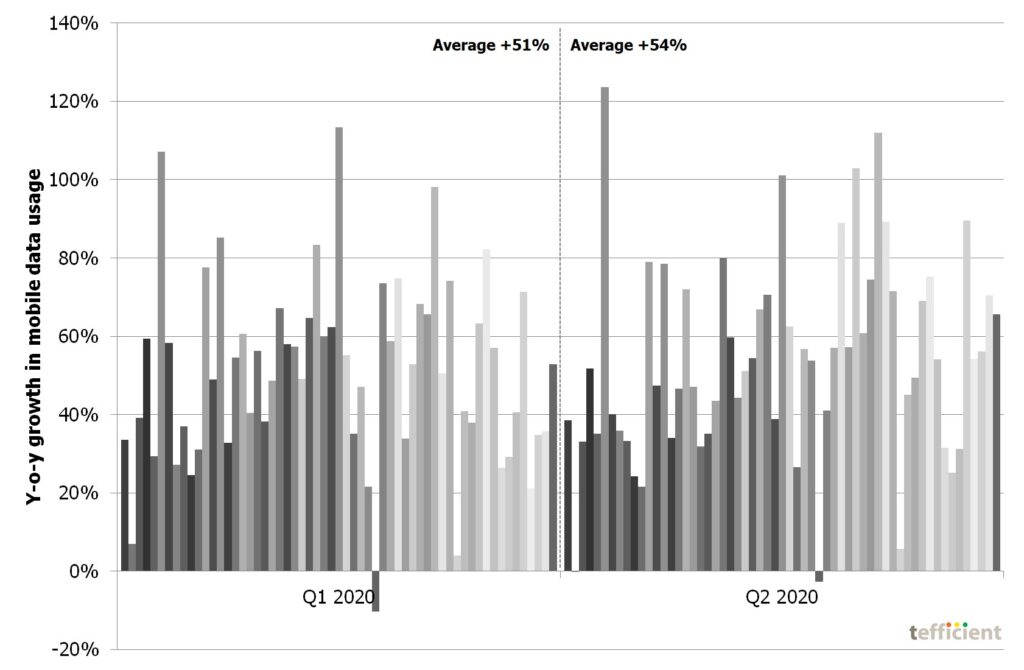

Although a pandemic hit the world in 1H 2020, usage grew in every single country. But the growth was unevenly distributed – some countries grew faster than before while others grew slower than before.

When COVID-19 hit the world and governments and authorities enforced restrictions on the society, the whole economy trembled. The telco business was affected, but the change in movement and usage patterns didn’t just bring negatives. Although the high margin mobile roaming revenue was lost, mature market telcos have, generally speaking, never reported higher margins than what they did in the just-closed third quarter of 2020.

We’ll show you what the key to this margin increase is.

Don’t get us wrong, cost management is important. Our point is that you should not base your improvement targets on your present actuals.

With targets such as “All functions cut 10% off the costs”, you risk cutting down on the activities that are key to your success. Too. Because you don’t know for sure that they are actually key to your success. Since you haven’t measured it against relevant peers. This year. It risks your business: The negative impact of 10% cost reduction in an activity that is key to your success could easily outweigh the positive impact of a equally large cost reduction in an activity which actually needed to be trimmed.

COVID-19 has raised the bar. In the midst of a global health crisis, telcos are delivering. For many operators, Q3 2020 represents their best EBITDA margin quarter ever. But we need to be honest about why. Many cost reductions have – so far – come almost automatically:

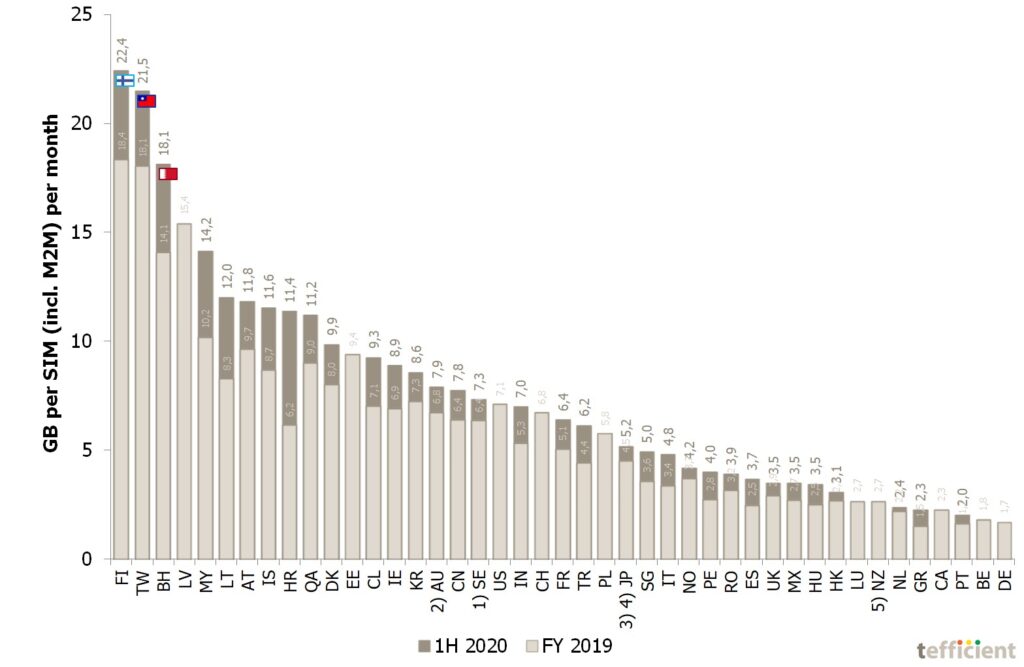

Tefficient’s 28th public analysis on the development and drivers of mobile data ranks 116 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2020.

The data usage per SIM grew for basically every operator. 42% could turn that data usage growth into ARPU growth.

Which are the equipment sales models in mobile and how have they developed over time? Can best practices be spotted when comparing equipment sales and profitability for a large number of mature market operators globally?

Using facts: What outputs are different equipment sales models such as subsidy, instalment, leasing, rental and BYOD generating – and how is an early upgrade promise affecting?

In this project we identified and documented a few operator best practices across different models in different markets.

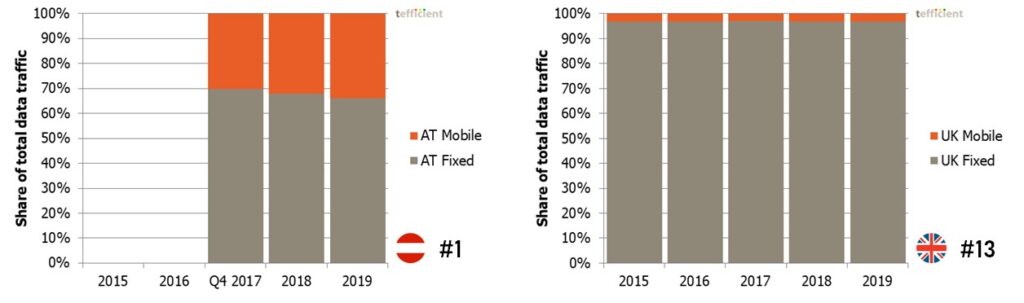

In our latest mobile data usage and revenue analysis, there are 43 countries. Of these, 27 are European. And among these, about half (13) of the regulators are not just reporting the mobile data traffic but also the fixed broadband traffic.

It allows us to compare the two and answer the question “is mobile eating fixed’s lunch?”

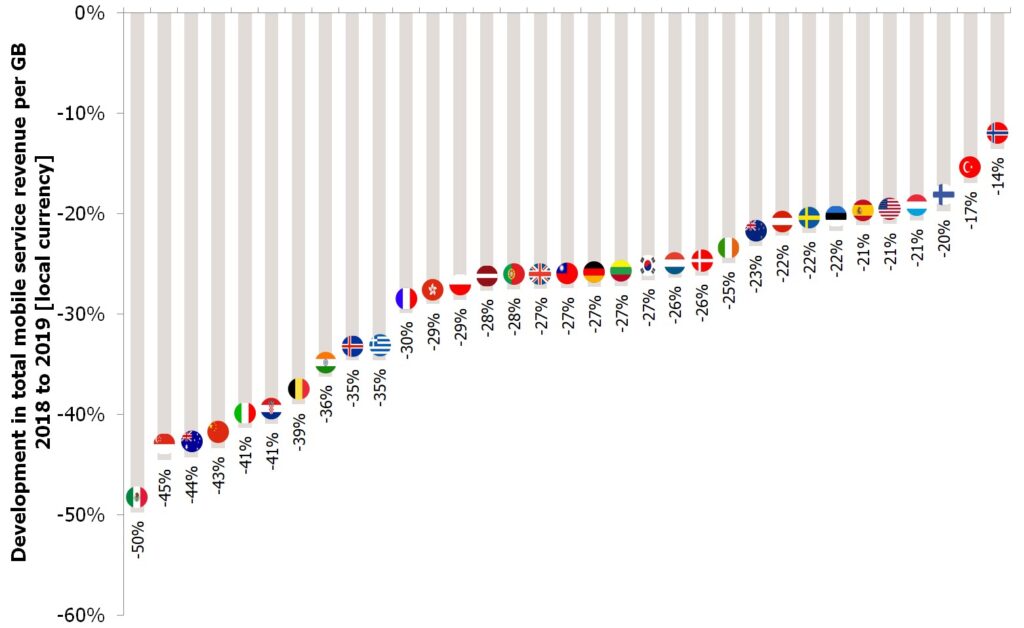

Tefficient’s 27th public analysis of the development and drivers of mobile data compares 44 countries from all regions of the world. We say hello to the new additions Chile, New Zealand and Qatar.

Usage is growing in every single country, but few are able to turn this into ARPU growth. Too few.

How have operators introduced fixed-mobile convergent plans in Europe’s most advanced markets France, Spain, Portugal, Belgium, Switzerland, the Netherlands – and in emerging FMC markets like the UK and Sweden? How – and how quickly – did competition react?

Using facts: What is the take-up of these FMC plans? How have the FMC introductions affected mobile and fixed market share, customer churn, acquisition & retention cost, demand for fibre and TV – and revenue and margin?

How do you avoid making FMC a discount-centric thing? How have the best FMC propositions been put together and how have they been marketed? Is there a way to leverage content and exclusivity?

For the eighth consecutive year: Comprehensive business benchmark with 890 KPIs covering revenue, OPEX, CAPEX, headcount productivity, subscriptions & channels, performance, load, quality and innovation & growth – for 54 functions of mobile, fixed/cable and integrated operators.

Peer group data exclusively from Swedish, Finnish, Norwegian and Danish operators. Due to pre-agreed confidentiality requirements, participating operators are anonymous (and of course their data).