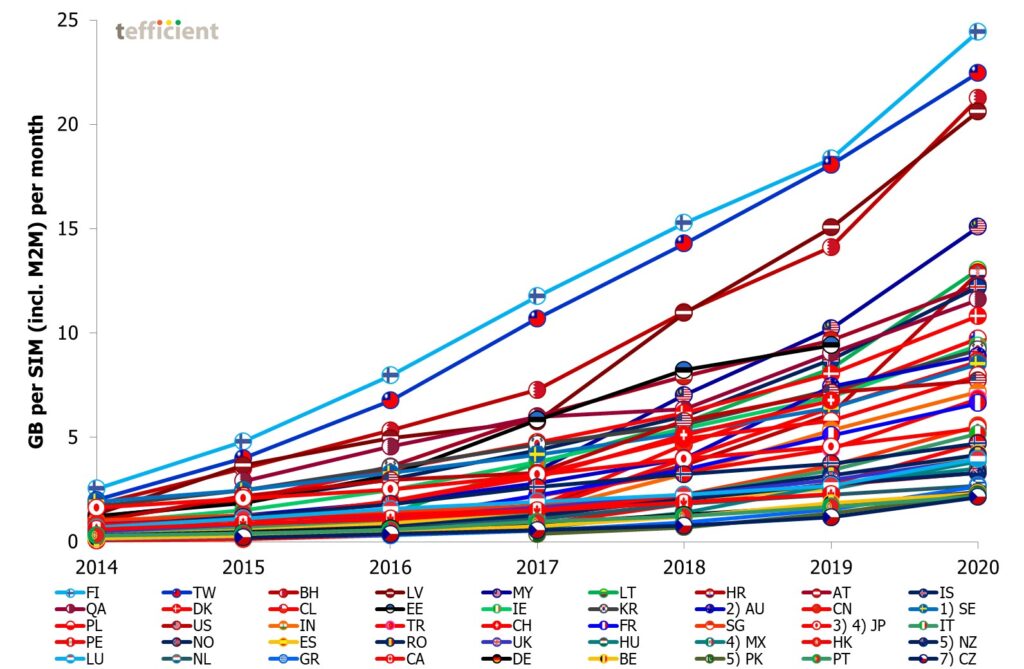

Tefficient’s 32nd public analysis of the development and drivers of mobile data compares 46 countries – now with Brazil added – from all regions of the world.

In our previous, full year 2020, report we could see that the pandemic drove mobile data usage – contrary to the belief that all that time we spent at home would offload mobile data traffic to Wi-Fi and fixed broadband.

Although the pandemic was still very much present in our daily life, the relaxation of restrictions in the first half of 2021 led to a more normal growth in mobile data usage.

Ericsson ConsumerLab published its latest report today.

The 5G Pacesetters report is the public outcome of a very ambitious project to design and analyse an index that measures both the 5G market performance and the consumer perception of 73 operators across 22 markets globally. Each 5G operator was analysed based on 105 criteria across 16 categories – from customer satisfaction to 5G offering, rollout and marketing efforts. It’s the first time a 5G index takes consumer satisfaction and consumers’ 5G leadership expectation into account.

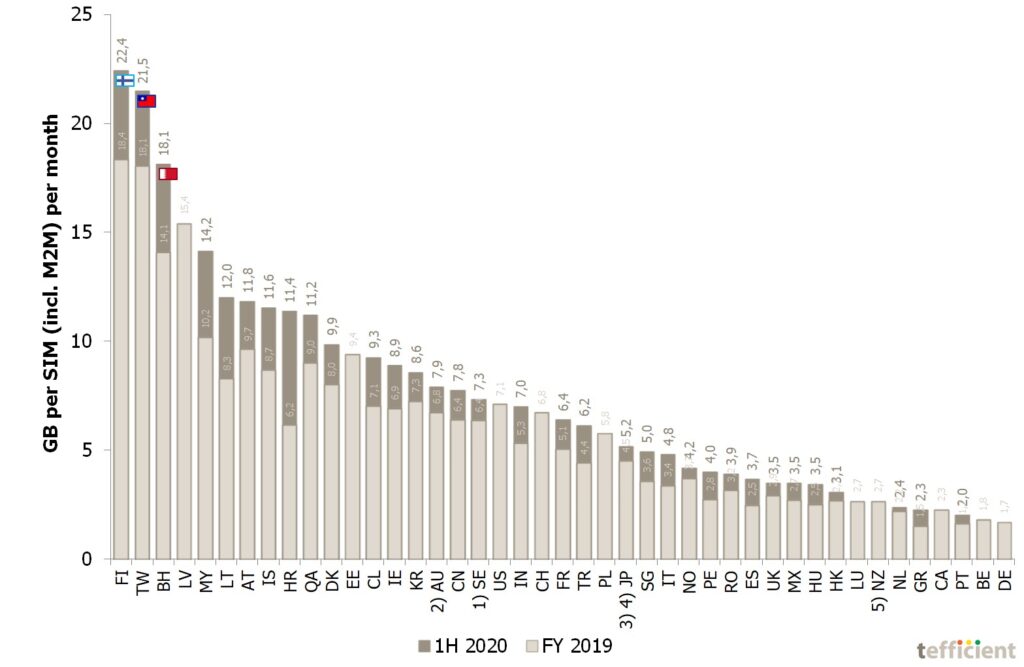

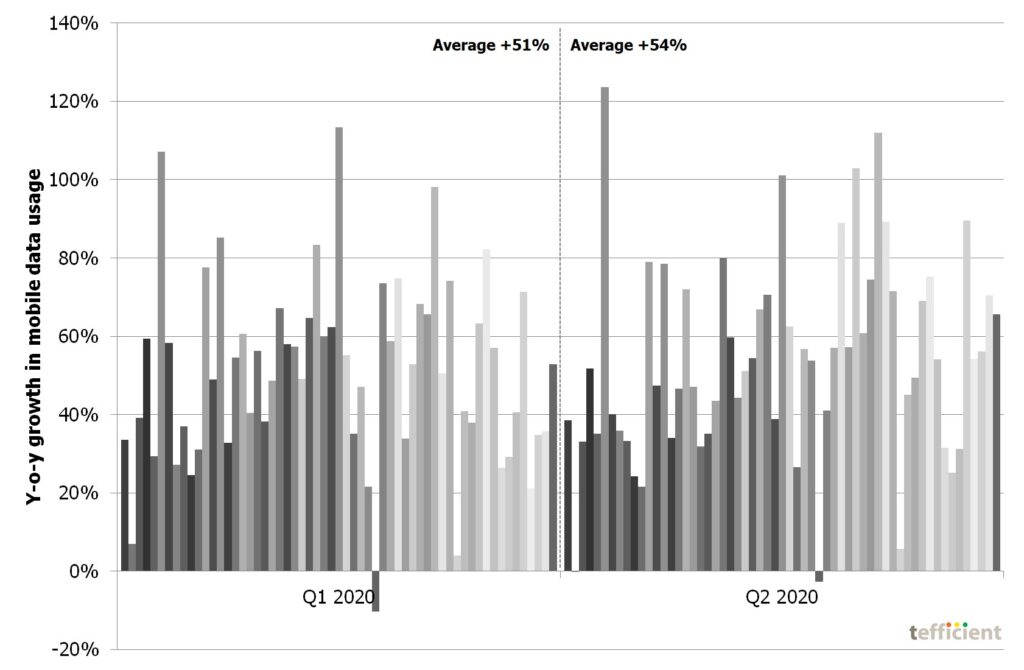

Tefficient’s 31st public analysis of the development and drivers of mobile data compares 45 countries from all regions of the world. The pandemic affected us all but although we to a high extent spent the year in our homes, mobile data usage increased in every single country. Mobile data is apparently not just used by people on the move.

Generally speaking, the growth accelerated in 2020; only a few countries experienced a slower growth rate.

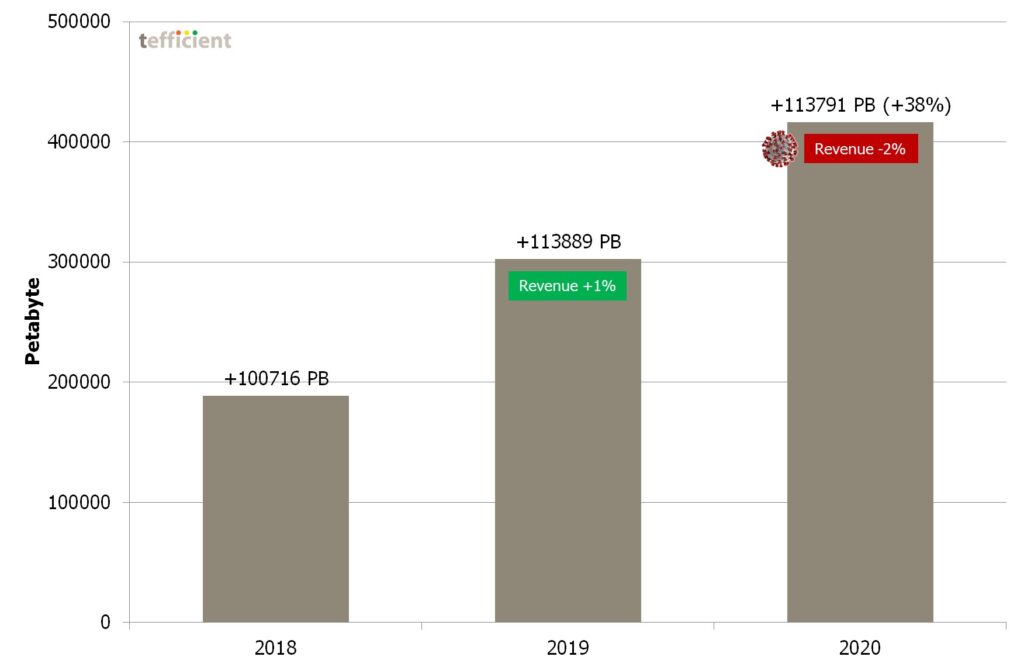

Tefficient’s 30th public analysis on the development and drivers of mobile data ranks 105 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the full year of 2020.

The data usage per SIM grew for basically every operator. 39% could turn that data usage growth into ARPU growth.

Tefficient has written two comprehensive analyses to support chapter 7 in the white paper addressing mobile and fixed broadband networks:

“Assessment of Norwegian mobile revenues in a Nordic context”

“Assessment of Norwegian fixed broadband pricing in a Nordic context”

The first analysis investigates whether Norwegian mobile prices should be considered high or moderate given certain specific Norwegian conditions. A multitude of metrics are used – always compared between the same four markets: Norway, Denmark, Sweden and Finland.

The second analysis investigates Norwegian broadband prices, comparing them against three other Nordic markets: Denmark, Sweden and Finland.

The white paper (in Norwegian) summarises the two analyses in sections 7.2.1.4 and 7.2.2.3 using selected graphs and conclusions. The ministry has integrated the key findings with own and independent research, data and viewpoints to form a basis for future policy.

Which cloud gaming and immersive video propositions are leading operators offering their 5G customers? How have operators gone about it; partnering with global brands, integrating a white label product – or even building it on their own?

KT celebrating 40k GameBox customers one month after launch

What about exclusivity? Can anyone buy or is it just for connectivity customers? Even for 5G customers only? Or have operators made the cloud gaming/immersive video service inclusive? If so, on an all plans or just on the more premium plans?

In this project we summarised and categorised all propositions in leading 5G markets globally and could spot some global trends.

Tefficient’s 29th public analysis of the development and drivers of mobile data compares 44 countries from all regions of the world.

Although a pandemic hit the world in 1H 2020, usage grew in every single country. But the growth was unevenly distributed – some countries grew faster than before while others grew slower than before.

Tefficient’s 28th public analysis on the development and drivers of mobile data ranks 116 operators based on average data usage per SIM, total data traffic and revenue per gigabyte in the first half of 2020.

The data usage per SIM grew for basically every operator. 42% could turn that data usage growth into ARPU growth.

Which are the equipment sales models in mobile and how have they developed over time? Can best practices be spotted when comparing equipment sales and profitability for a large number of mature market operators globally?

Using facts: What outputs are different equipment sales models such as subsidy, instalment, leasing, rental and BYOD generating – and how is an early upgrade promise affecting?

In this project we identified and documented a few operator best practices across different models in different markets.

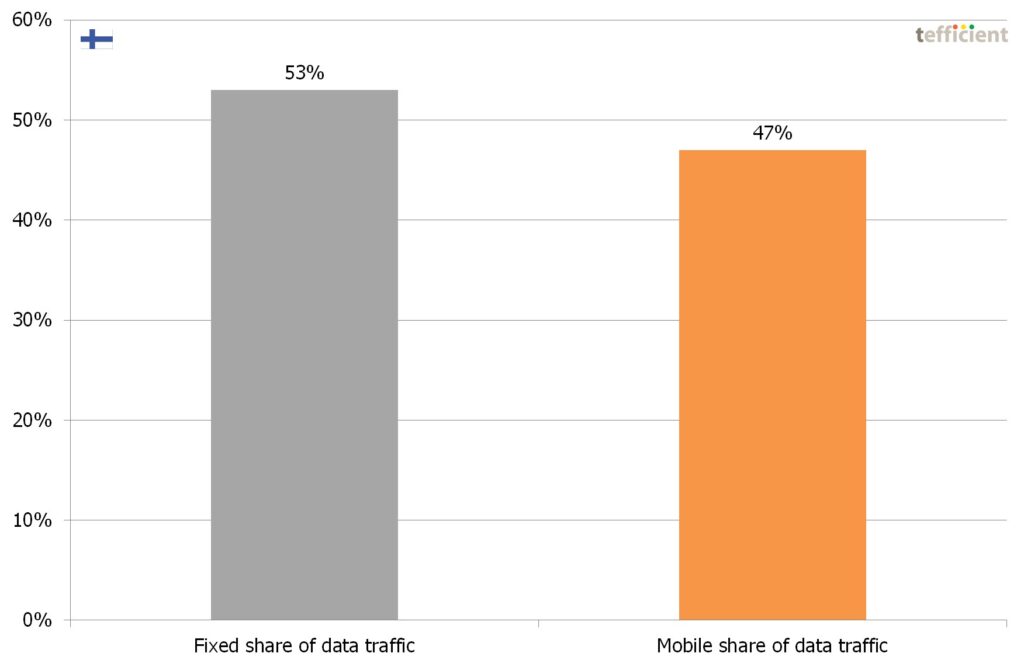

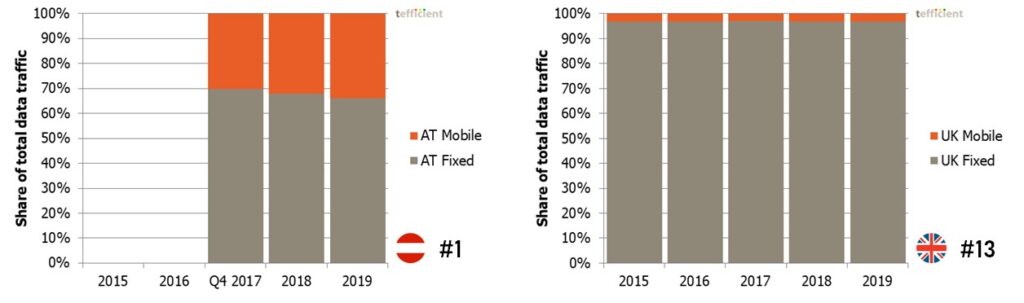

In our latest mobile data usage and revenue analysis, there are 43 countries. Of these, 27 are European. And among these, about half (13) of the regulators are not just reporting the mobile data traffic but also the fixed broadband traffic.

It allows us to compare the two and answer the question “is mobile eating fixed’s lunch?”